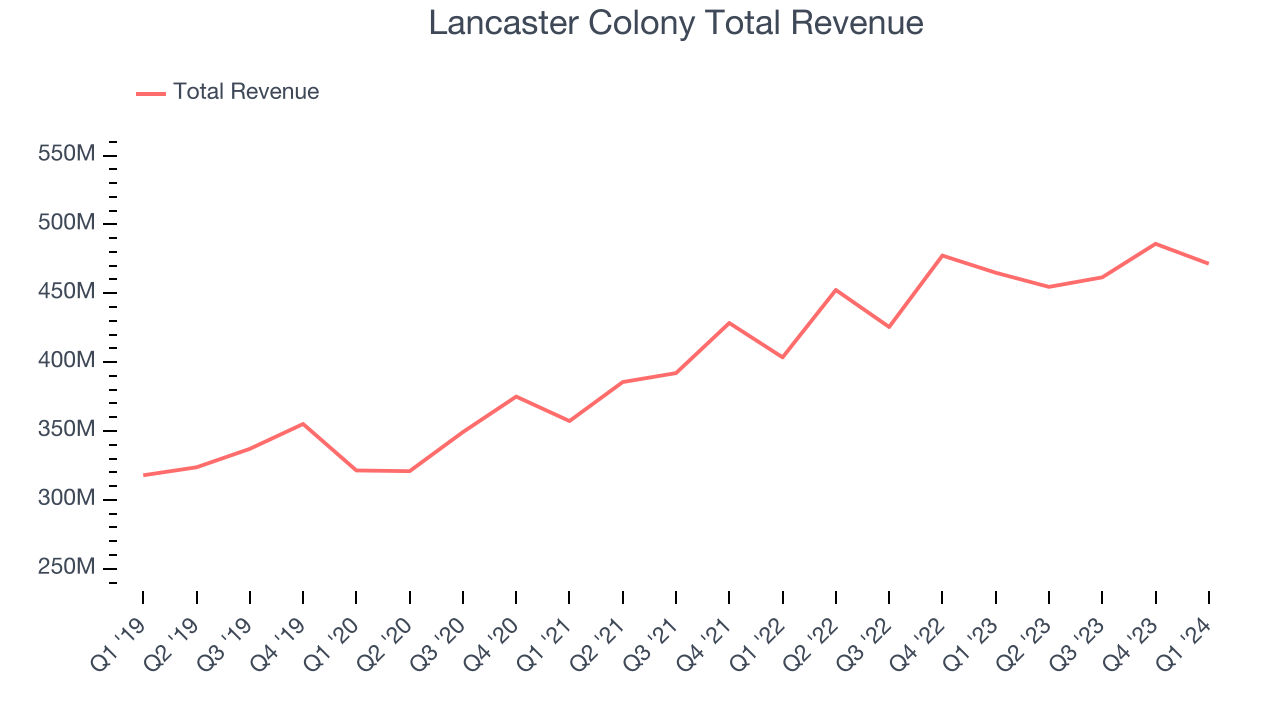

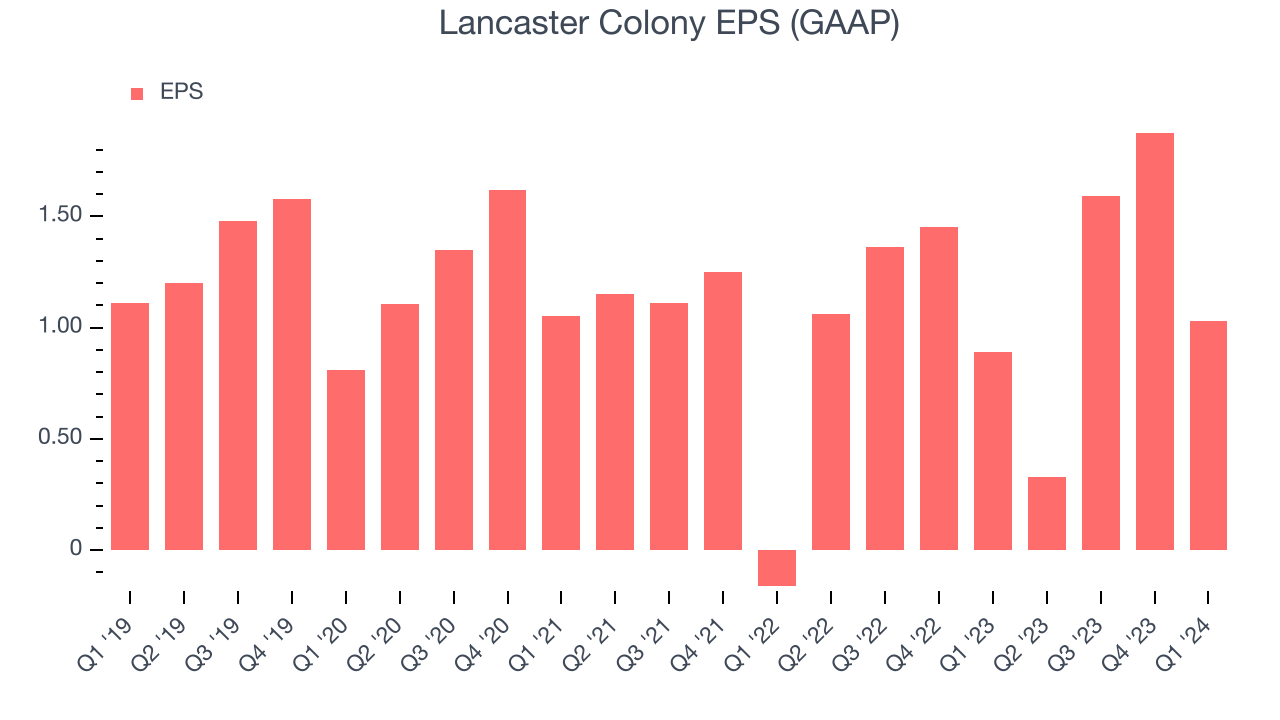

Specialty food company Lancaster Colony (NASDAQ:LANC) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 1.4% year on year to $471.4 million. It made a GAAP profit of $1.03 per share, improving from its profit of $0.89 per share in the same quarter last year.

Lancaster Colony (LANC) Q1 CY2024 Highlights:

- Revenue: $471.4 million vs analyst estimates of $468.2 million (small beat)

- Operating profit: $47.3 million vs analyst estimates of $48.6 million (2.7% miss)

- EPS: $1.03 vs analyst expectations of $1.40 (26.3% miss)

- No guidance given but management anticipates "Retail sales will continue to benefit from our licensing program, including incremental growth from the recent additions of Subway and Texas Roadhouse sauces. In the Foodservice segment, we expect continued volume growth from select quick-service restaurant customers and our branded Foodservice products, while deflationary pricing is projected to remain a headwind to Foodservice segment net sales"

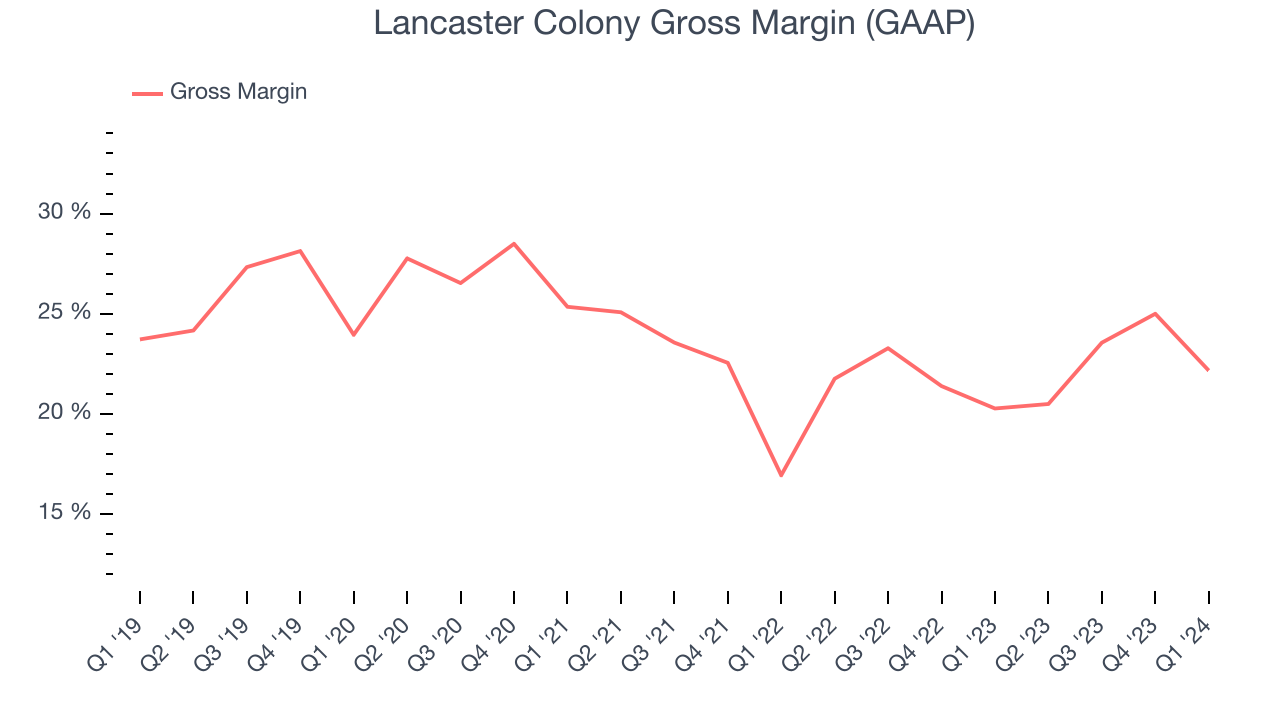

- Gross Margin (GAAP): 22.2%, up from 20.3% in the same quarter last year

- Sales Volumes were up 1.5% year on year

- Market Capitalization: $5.27 billion

Known for its frozen garlic bread and Parkerhouse rolls, Lancaster Colony (NASDAQ:LANC) sells bread, dressing, and dips to the retail and food service channels.

The company was founded in 1961 as a glass and automotive products company. However, it quickly shifted focus towards specialty foods. Since its inception, Lancaster Colony has grown both organically and through a series of acquisitions, with its purchase of salad dressings giant Marzetti in 1969 as one of the most significant.

In addition to Marzetti dressings, Lancaster Colony goes to market with the Sister Schubert brand of rolls and the New York Brand Bakery brand of garlic breads, croutons, and toasts. The company sells to the retail channel, where its dressings and dips products can be found in grocery produce departments and where other products can be found in the shelf-stable sections. Lancaster Colony also sells private-label products to restaurants.

At retail, the core Lancaster Colony customer is likely someone who does the grocery shopping for his or her household. This customer values convenience, as he or she has little time between work, kids, and other commitments to make food from scratch. Those who buy the company’s dressings are likely also health conscious and use the products to add some pizzazz to their salads.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors in specialty foods include Treehouse Foods (NYSE:THS), Flowers Foods (NYSE:FLO), and Clorox (NYSE;CLX), which owns the Hidden Valley dressing brand.Sales Growth

Lancaster Colony carries some recognizable brands and products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Lancaster Colony can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's annualized revenue growth rate of 10.1% over the last three years was decent for a consumer staples business.

This quarter, Lancaster Colony grew its revenue by 1.4% year on year, and its $471.4 million in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 3% over the next 12 months, an acceleration from this quarter.

Gross Margin & Pricing Power

All else equal, we prefer higher gross margins. They make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Lancaster Colony's gross profit margin came in at 22.2% this quarter, up 1.9 percentage points year on year. That means for every $1 in revenue, a chunky $0.78 went towards paying for raw materials, production of goods, and distribution expenses.

Lancaster Colony has poor unit economics for a consumer staples company, leaving it with little room for error if things go awry. As you can see above, it's averaged a paltry 22.2% gross margin over the last two years. Its margin, however, has been trending up over the last 12 months, averaging 5.4% year-on-year increases each quarter. If this trend continues, it could suggest a less competitive environment.

Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

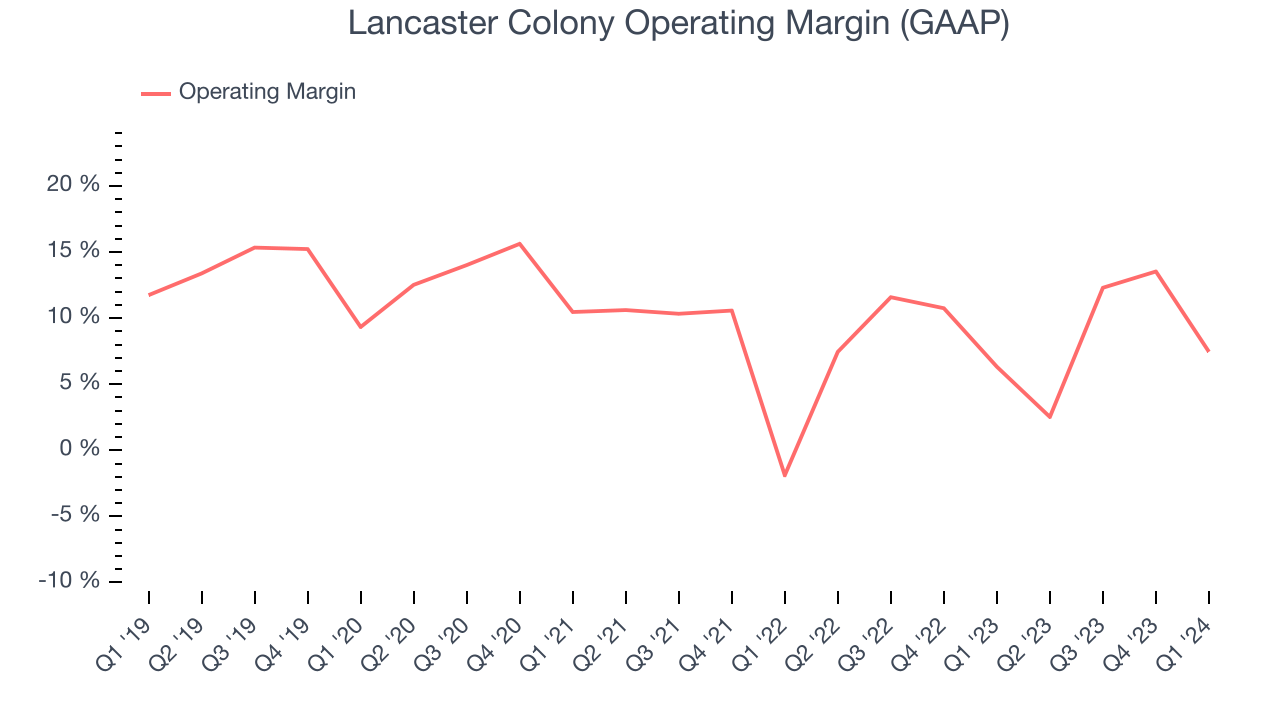

This quarter, Lancaster Colony generated an operating profit margin of 7.5%, up 1.1 percentage points year on year. This increase was encouraging, and we can infer Lancaster Colony had stronger pricing power and lower raw materials/transportation costs because its gross margin expanded more than its operating margin.

Zooming out, Lancaster Colony has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 9%, higher than the broader consumer staples sector. On top of that, its margin has remained more or less the same, highlighting the consistency of its business. The company's operating profitability was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes tectonic shifts to move meaningfully. Companies have more control over their operating margins, and it signals strength if they're high when gross margins are low (like for Lancaster Colony).

Zooming out, Lancaster Colony has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 9%, higher than the broader consumer staples sector. On top of that, its margin has remained more or less the same, highlighting the consistency of its business. The company's operating profitability was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes tectonic shifts to move meaningfully. Companies have more control over their operating margins, and it signals strength if they're high when gross margins are low (like for Lancaster Colony).EPS

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q1, Lancaster Colony reported EPS at $1.03, up from $0.89 in the same quarter a year ago. This print unfortunately missed Wall Street's estimates, but we care more about long-term EPS growth rather than short-term movements.

Between FY2021 and FY2024, Lancaster Colony's EPS dropped 5.8%, translating into 2% annualized declines. We tend to steer our readers away from companies with falling EPS, especially in the consumer staples sector, where shrinking earnings could imply changing secular trends or consumer preferences. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

On the bright side, Wall Street expects the company's earnings to grow over the next 12 months, with analysts projecting an average 42.6% year-on-year increase in EPS.

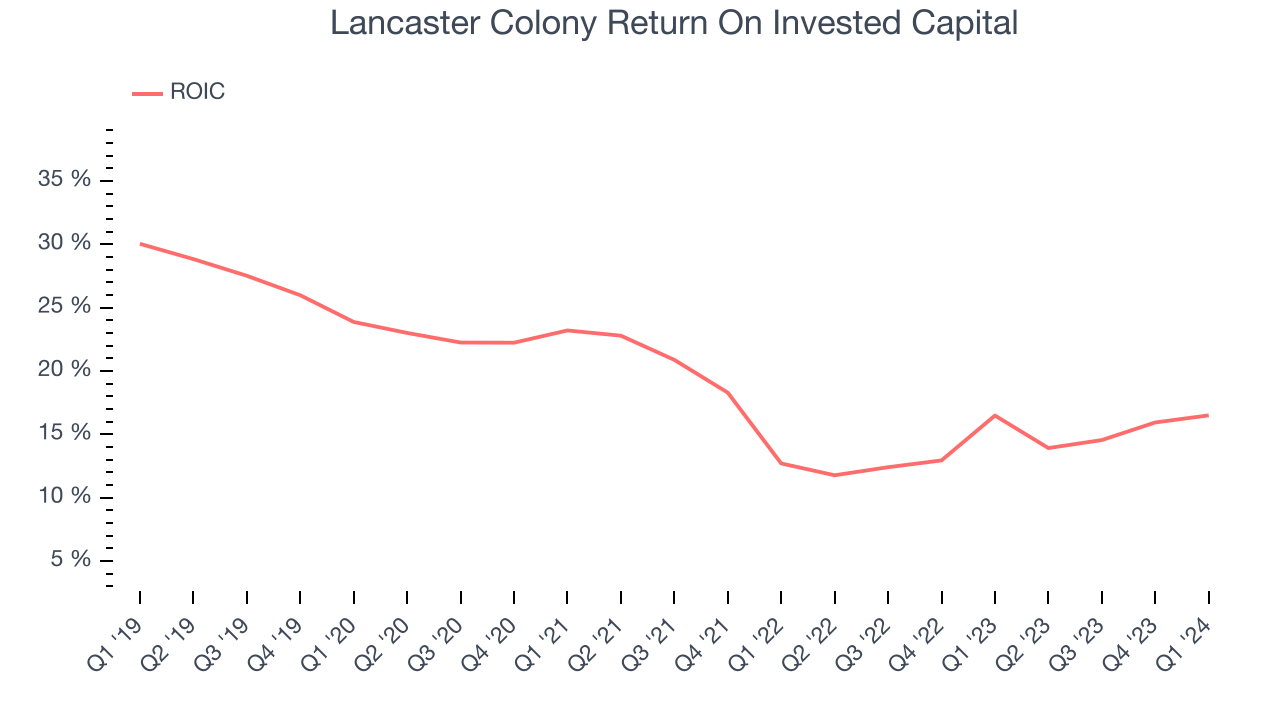

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Lancaster Colony's five-year average ROIC was 18.6%, higher than most consumer staples companies. Just as you’d like your investment dollars to generate returns, Lancaster Colony's invested capital has produced solid profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Lancaster Colony's ROIC averaged 7 percentage point decreases over the last few years. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Lancaster Colony is a well-capitalized company with $164.8 million of cash and no debt. This position gives Lancaster Colony the freedom to borrow money, return capital to shareholders, or invest in growth initiatives.

Key Takeaways from Lancaster Colony's Q1 Results

It was encouraging to see Lancaster Colony narrowly top analysts' revenue expectations this quarter. On the other hand, its operating profit and operating margin missed analysts' expectations, leading to lower-than-expected EPS. Overall, the results could have been better. The stock is flat after reporting and currently trades at $191.43 per share.

Is Now The Time?

Lancaster Colony may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We have other favorites, but we understand the arguments that Lancaster Colony isn't a bad business. First off, its revenue growth has been solid over the last three years. And while its gross margins make it more challenging to reach positive operating profits compared to other consumer staples businesses, its projected EPS for the next year implies the company's fundamentals will improve.

Lancaster Colony's price-to-earnings ratio based on the next 12 months is 27.8x. There are things to like about Lancaster Colony and there's no doubt it's a bit of a market darling, at least for some investors. But it seems there's a lot of optimism already priced in and we wonder if there are better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $212.15 per share right before these results (compared to the current share price of $191.43).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.