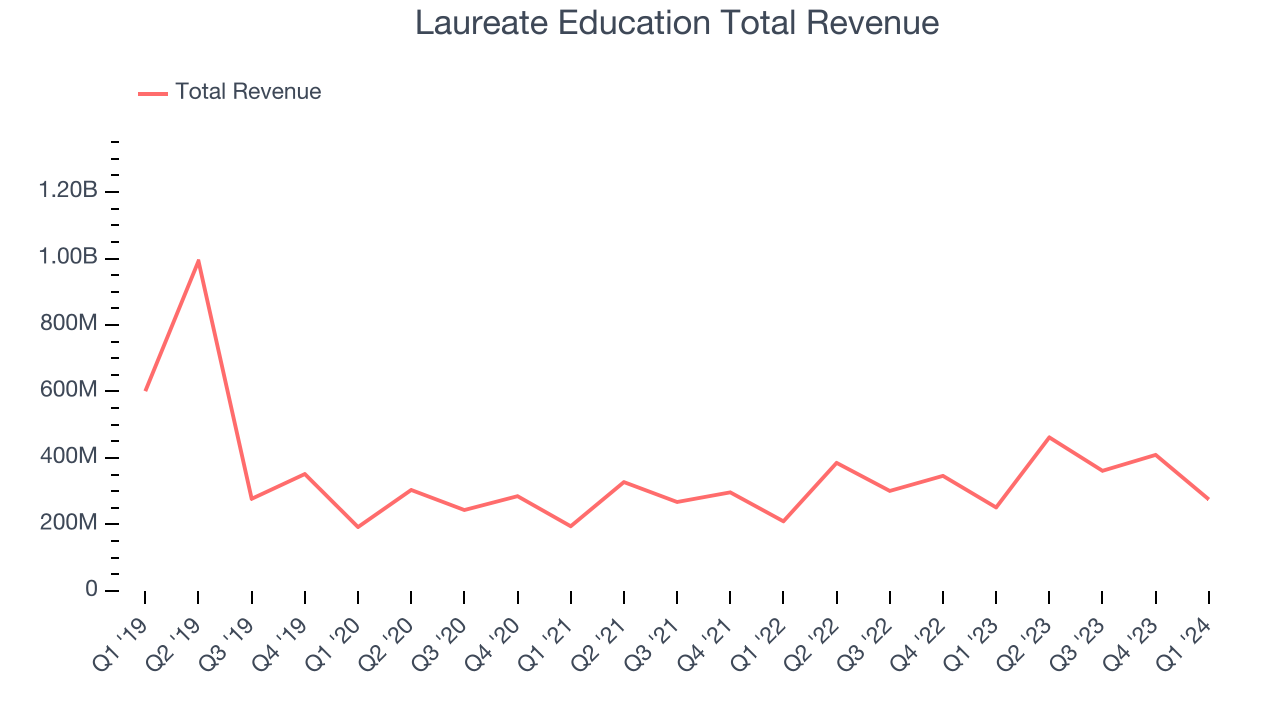

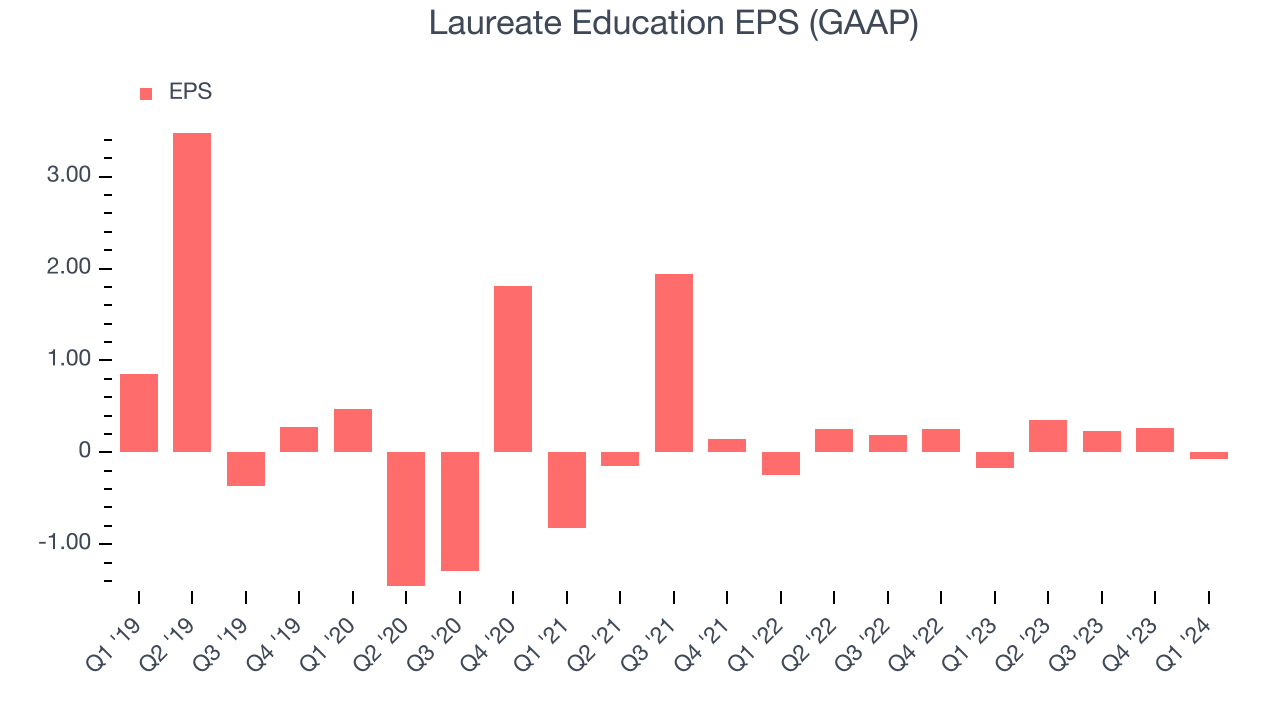

Higher education company Laureate Education (NASDAQ:LAUR) announced better-than-expected results in Q1 CY2024, with revenue up 9.6% year on year to $275.4 million. The company expects the full year's revenue to be around $1.57 billion, in line with analysts' estimates. It made a GAAP loss of $0.07 per share, improving from its loss of $0.17 per share in the same quarter last year.

Laureate Education (LAUR) Q1 CY2024 Highlights:

- Revenue: $275.4 million vs analyst estimates of $269.3 million (2.3% beat)

- Adjusted EBITDA: $30.6 million vs analyst estimates of $25.0 million (22.4% beat)

- EPS: -$0.07 vs analyst estimates of -$0.03 (-$0.04 miss)

- Full year guidance for revenue and adjusted EBITDA both exceeded expectations

- Gross Margin (GAAP): 7.8%, down from 10.3% in the same quarter last year

- Free Cash Flow of $17.3 million, down 48.6% from the previous quarter

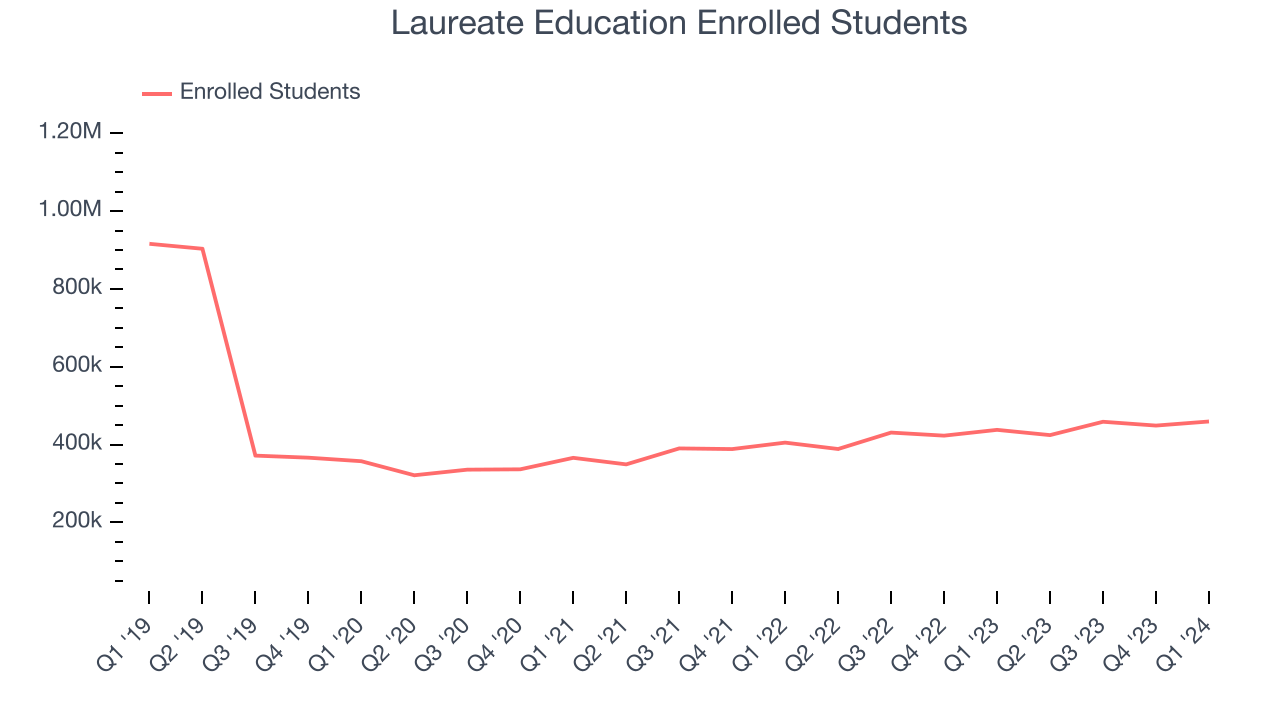

- Enrolled Students: 459,400

- Market Capitalization: $2.30 billion

Founded in 1998 by Douglas L. Becker and based in Miami, Laureate Education (NASDAQ:LAUR) is a global network of higher education institutions.

Laureate Education has both traditional campus-based learning and online offerings. The company's institutions offer undergraduate, master's, and doctoral degree programs in disciplines such as business, healthcare, engineering, and education.

A focus of Laureate Education is the internationalization of its curriculum and student body. Many of its institutions hold a diverse mix of local and international students, fostering a multicultural learning environment.

Laureate Education also offers opportunities for student exchanges and global learning experiences across its network, which includes universities in Mexico and Peru.

We note the company's historical financials are distorted because it conducted several divestitures between 2018 and 2019. Divested assets include Kendall College, University of St. Augustine for Health Sciences, Universidad Europea de Madrid, and many others.

Education Services

A whole industry has emerged to address the problem of rising education costs, offering consumers alternatives to traditional education paths such as four-year colleges. These alternative paths, which may include online courses or flexible schedules, make education more accessible to those with work or child-rearing obligations. However, some have run into issues around the value of the degrees and certifications they provide and whether customers are getting a good deal. Those who don’t prove their value could struggle to retain students, or even worse, invite the heavy hand of regulation.

Laureate Education's primary competitors include Strategic Education (NASDAQ:STRA), Adtalem Global Education (NYSE:ATGE), and Grand Canyon Education (NASDAQ:LOPE).Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Laureate Education's revenue declined over the last five years, dropping 14.4% annually.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Laureate Education's annualized revenue growth of 17% over the last two years is a reversal from its five-year trend, suggesting some bright spots.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Laureate Education's annualized revenue growth of 17% over the last two years is a reversal from its five-year trend, suggesting some bright spots.

We can better understand the company's revenue dynamics by analyzing its number of enrolled students, which reached 459,400 in the latest quarter. Over the last two years, Laureate Education's enrolled students averaged 8.2% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company's monetization of its consumers has risen.

This quarter, Laureate Education reported solid year-on-year revenue growth of 9.6%, and its $275.4 million of revenue outperformed Wall Street's estimates by 2.3%. Looking ahead, Wall Street expects sales to grow 4.6% over the next 12 months, a deceleration from this quarter.

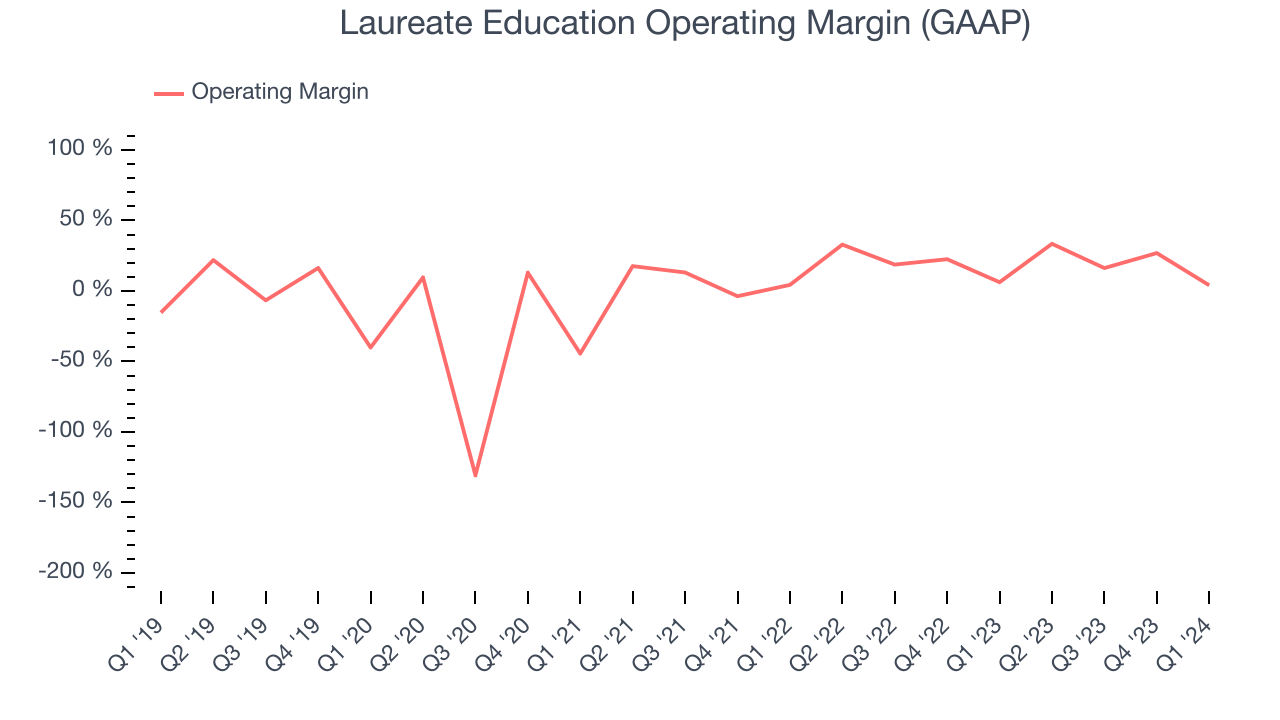

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Laureate Education has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 21.9%.

This quarter, Laureate Education generated an operating profit margin of 4%, down 2.2 percentage points year on year.

Over the next 12 months, Wall Street expects Laureate Education to maintain its LTM operating margin of 22.2%.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, Laureate Education's EPS dropped 102%, translating into 15% annualized declines. Thankfully, Laureate Education has bucked its trend as of late, growing its EPS over the last three years. We'll see if the company's growth is sustainable.

In Q1, Laureate Education reported EPS at negative $0.07, up from negative $0.17 in the same quarter last year. Despite growing year on year, this print unfortunately missed analysts' estimates. Over the next 12 months, Wall Street expects Laureate Education to grow its earnings. Analysts are projecting its LTM EPS of $0.77 to climb by 84.4% to $1.42.

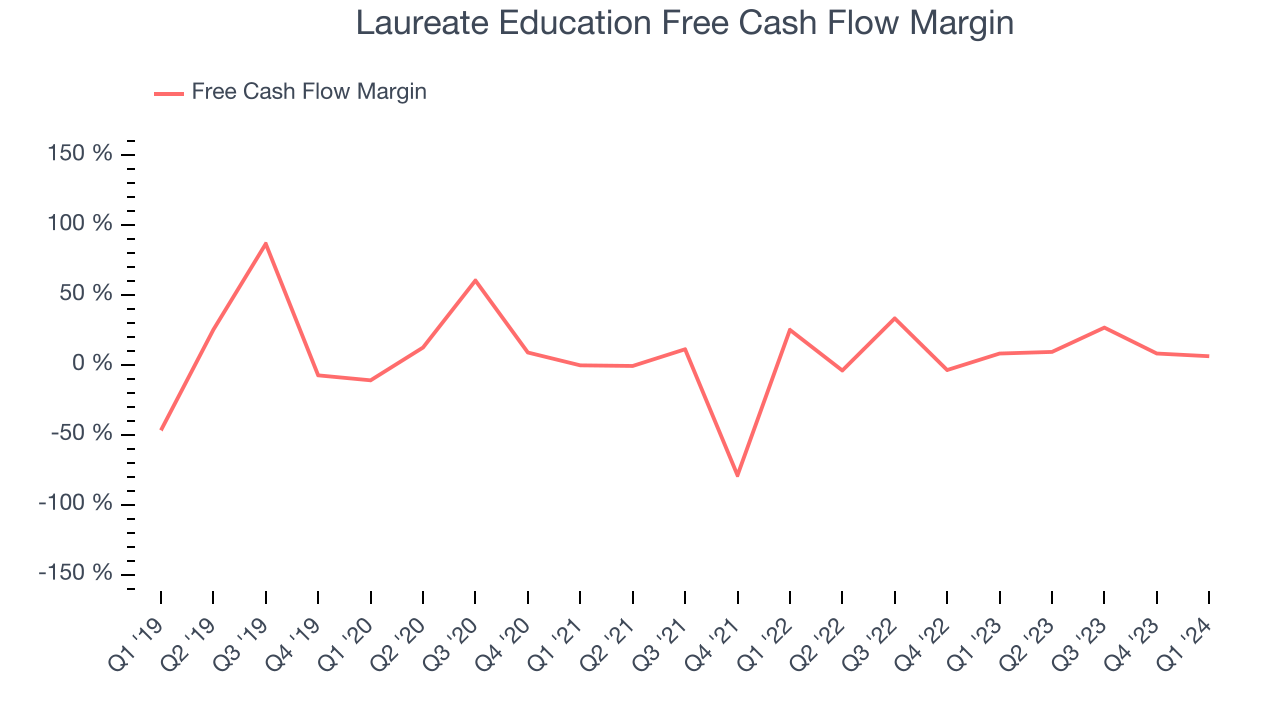

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Laureate Education has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 10.2%, slightly better than the broader consumer discretionary sector.

Laureate Education's free cash flow came in at $17.3 million in Q1, equivalent to a 6.3% margin and down 16.2% year on year. Over the next year, analysts' consensus estimates show they're expecting Laureate Education's LTM free cash flow margin of 12.7% to remain the same.

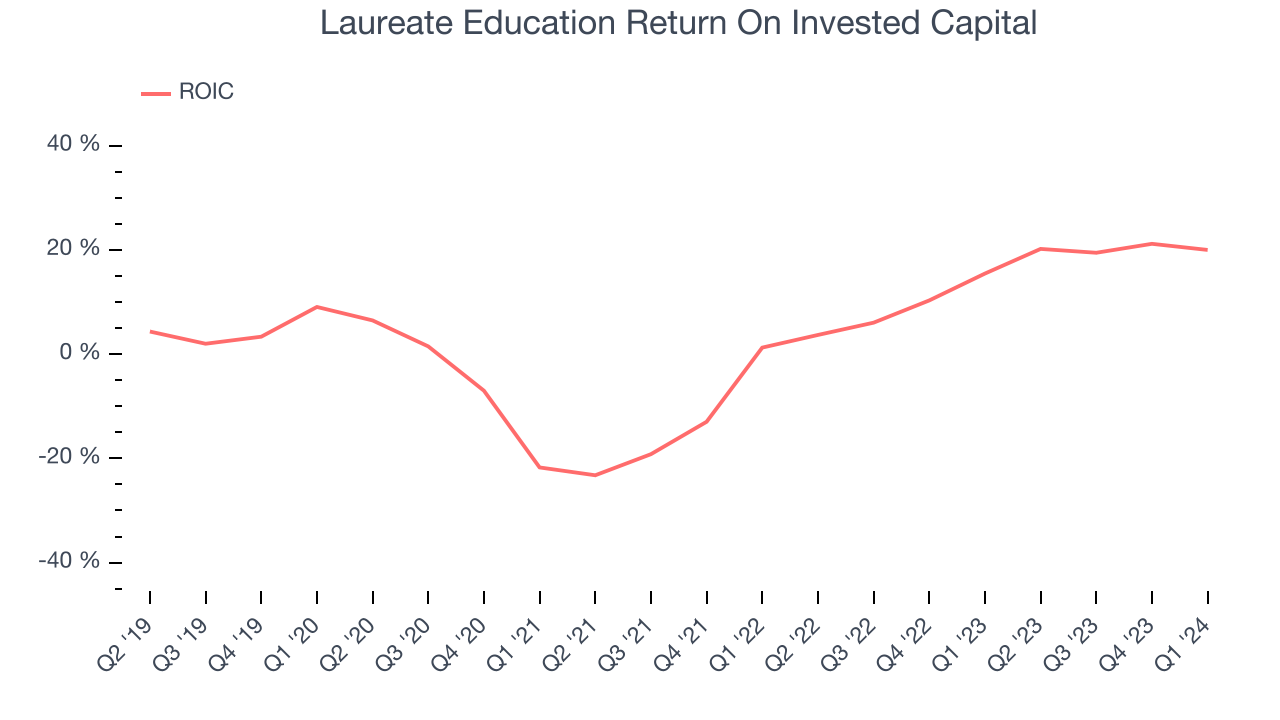

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Laureate Education's five-year average return on invested capital was 4.8%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Laureate Education's ROIC has significantly increased. This is a good sign, and we hope the company can continue improving.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Laureate Education reported $126.2 million of cash and $628.1 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $415.7 million of EBITDA over the last 12 months, we view Laureate Education's 1.2x net-debt-to-EBITDA ratio as safe. We also see its $10.91 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Laureate Education's Q1 Results

We were impressed by how significantly Laureate Education blew past analysts' adjusted EBITDA expectations this quarter, showing strong profitability. We were also glad its revenue outperformed Wall Street's estimates. Full year guidance for both revenue and adjusted EBITDA came in ahead of expectations. On the other hand, its number of enrolled students fell short of Wall Street's estimates. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 4.5% after reporting and currently trades at $15.24 per share.

Is Now The Time?

Laureate Education may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Laureate Education, we'll be cheering from the sidelines. Its revenue has declined over the last five years, but at least growth is expected to increase in the short term. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its declining EPS over the last five years makes it hard to trust. On top of that, its relatively low ROIC suggests it has historically struggled to find compelling business opportunities.

Laureate Education's price-to-earnings ratio based on the next 12 months is 10.3x. While there are some things to like about Laureate Education and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $17.67 per share right before these results (compared to the current share price of $15.24).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.