Wrapping up Q1 earnings, we look at the numbers and key takeaways for the semiconductor manufacturing stocks, including Lam Research (NASDAQ:LRCX) and its peers.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers and data storage. The growth of data and technologies like artificial intelligence, 5G networks and smart cars are also creating a next wave of growth for the industry. To keep up with ever changing customer needs requires new tools that can design, fabricate and test at ever smaller sizes and more complex architectures, and that is driving the demand for semiconductor capital manufacturing equipment.

The 4 semiconductor manufacturing stocks we track reported a weak Q1; on average, revenues missed analyst consensus estimates by 0.16%, while on average next quarter revenue guidance was 1.75% under consensus. Tech stocks have had a rocky start in 2022 and while some of the semiconductor manufacturing stocks have fared somewhat better, they have not been spared, with share price declining 12% since earnings, on average.

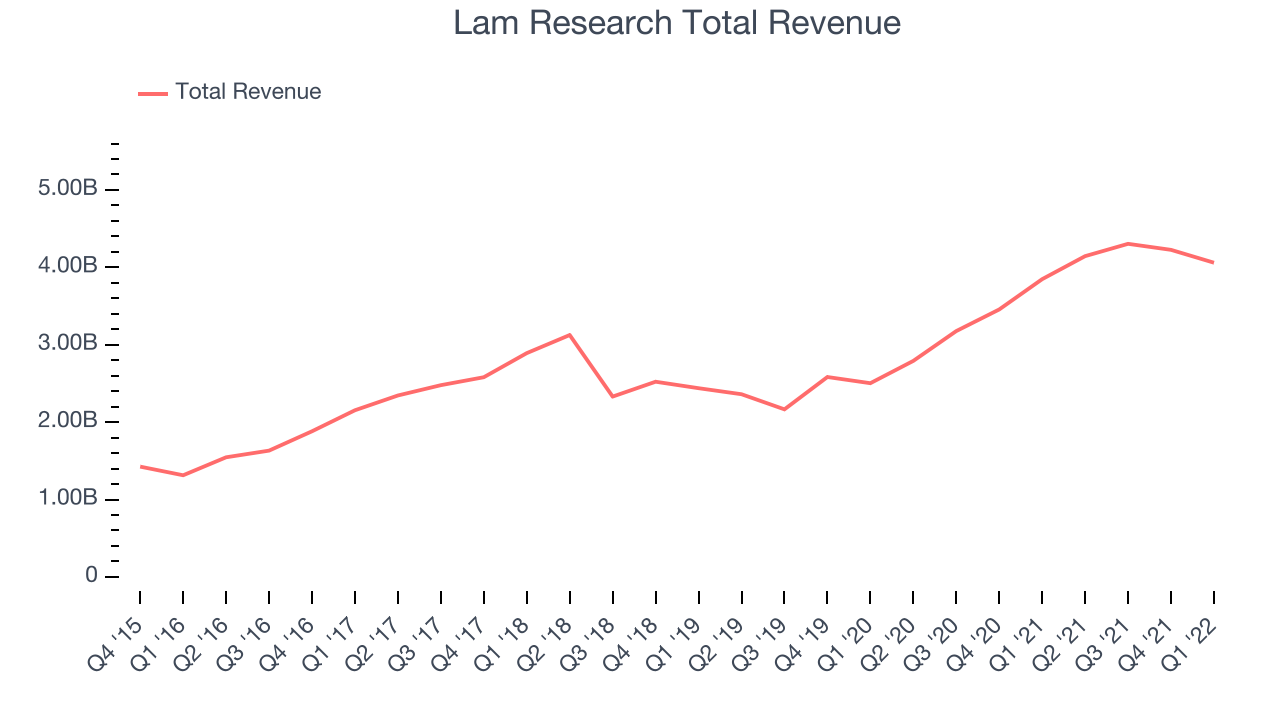

Weakest Q1: Lam Research (NASDAQ:LRCX)

Founded in 1980 by David Lam, who pioneered semiconductor etching technology, Lam Research (NASDAQ:LCRX) is one of the leading providers of the wafer fabrication equipment used to make semiconductors.

Lam Research reported revenues of $4.06 billion, up 5.52% year on year, missing analyst expectations by 4.33%. It was a weak quarter for the company, with an underwhelming revenue guidance for the next quarter and a miss of the top line analyst estimates.

“In an extraordinarily difficult supply environment, Lam reported March quarter results within guided ranges,” said Tim Archer, Lam Research’s President and Chief Executive Officer.

Lam Research delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. The stock is down 11.4% since the results and currently trades at $427.49.

Is now the time to buy Lam Research? Access our full analysis of the earnings results here, it's free.

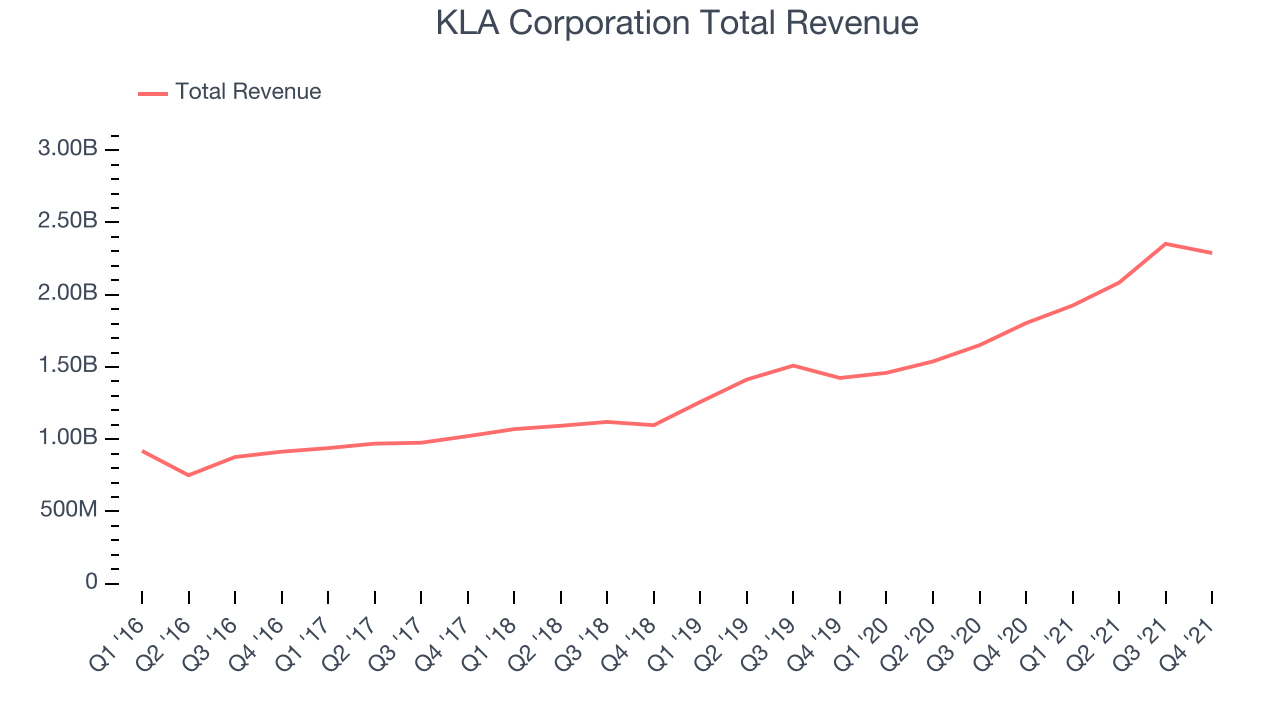

Best Q1: KLA Corporation (NASDAQ:KLAC)

Formed by the 1997 merger of the two leading semiconductor yield management companies, KLA Corporation (NASDAQ:KLAC) is the leading supplier of equipment used to measure and inspect semiconductor chips.

KLA Corporation reported revenues of $2.28 billion, up 26.8% year on year, beating analyst expectations by 3.84%. It was a decent quarter for the company, with a beat on the bottom line but an increase in inventory levels.

KLA Corporation achieved the strongest analyst estimates beat among its peers. The stock is down 2.75% since the results and currently trades at $323.81.

Is now the time to buy KLA Corporation? Access our full analysis of the earnings results here, it's free.

Applied Materials (NASDAQ:AMAT)

Founded in 1967 as the first company that built the tools for other companies to use to make semiconductors, Applied Materials (NASDAQ:AMAT) is the largest provider of semiconductor wafer fabrication equipment.

Applied Materials reported revenues of $6.24 billion, up 11.8% year on year, missing analyst expectations by 1.63%. It was a weak quarter for the company, with an underwhelming revenue guidance for the next quarter and a miss of the top line analyst estimates.

The stock is down 15% since the results and currently trades at $94.08.

Read our full analysis of Applied Materials's results here.

Marvell Technology (NASDAQ:MRVL)

Moving away from a low margin storage device management chips in one of the biggest semiconductor business model pivots of the past decade, Marvell Technology (NASDAQ: MRVL) is a fabless designer of special purpose data processing and networking chips used by data centers, communications carriers, enterprises, and autos.

Marvell Technology reported revenues of $1.44 billion, up 73.8% year on year, beating analyst expectations by 1.46%. It was a mixed quarter for the company, with an improvement in gross margin, but an increase in inventory levels.

Marvell Technology achieved the fastest revenue growth among the peers. The stock is down 18.8% since the results and currently trades at $46.19.

Read our full, actionable report on Marvell Technology here, it's free.

The author has no position in any of the stocks mentioned