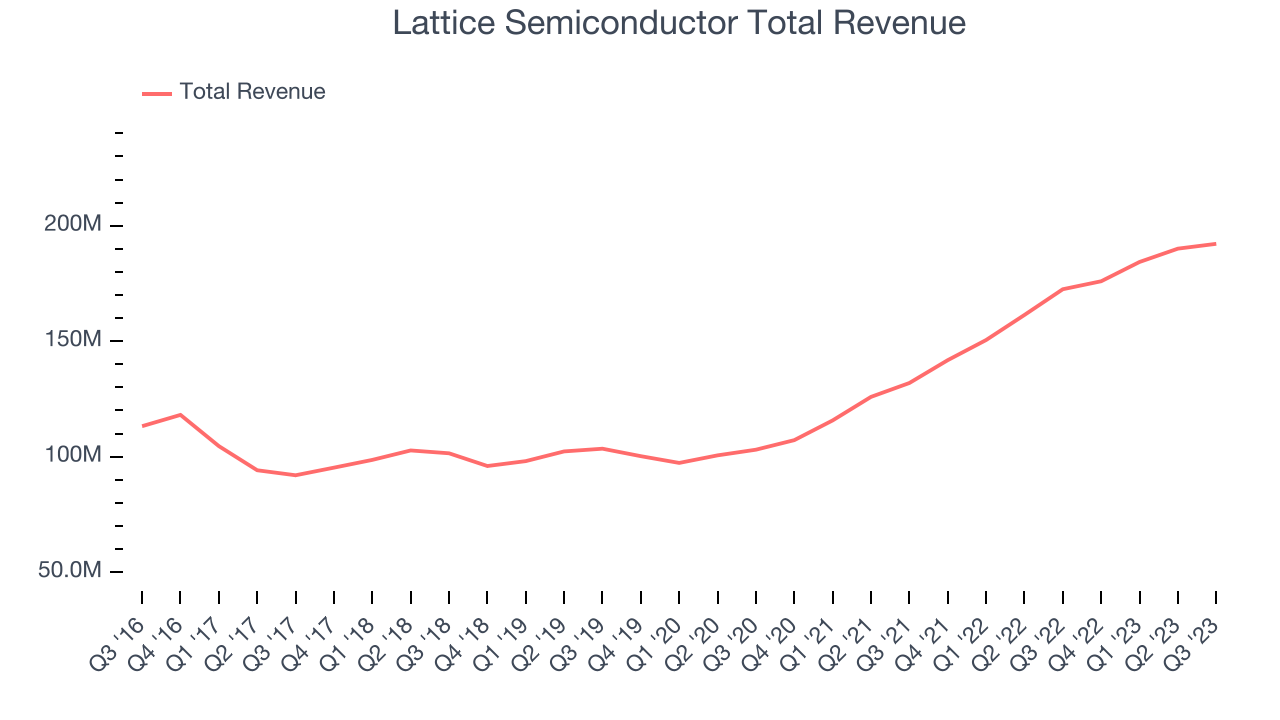

Semiconductor designer Lattice Semiconductor (NASDAQ:LSCC) reported results in line with analysts' expectations in Q3 FY2023, with revenue up 11.4% year on year to $192.2 million. However, next quarter's revenue guidance of $176 million was less impressive, coming in 10% below analysts' estimates. Turning to EPS, Lattice Semiconductor made a non-GAAP profit of $0.53 per share, improving from its profit of $0.33 per share in the same quarter last year.

Is now the time to buy Lattice Semiconductor? Find out by accessing our full research report, it's free.

Lattice Semiconductor (LSCC) Q3 FY2023 Highlights:

- Revenue: $192.2 million vs analyst estimates of $191.8 million (small beat)

- EPS (non-GAAP): $0.53 vs analyst estimates of $0.52 (1.72% beat)

- Revenue Guidance for Q4 2023 is $176 million at the midpoint, below analyst estimates of $195.7 million

- Free Cash Flow of $77.7 million, up 15.9% from the previous quarter

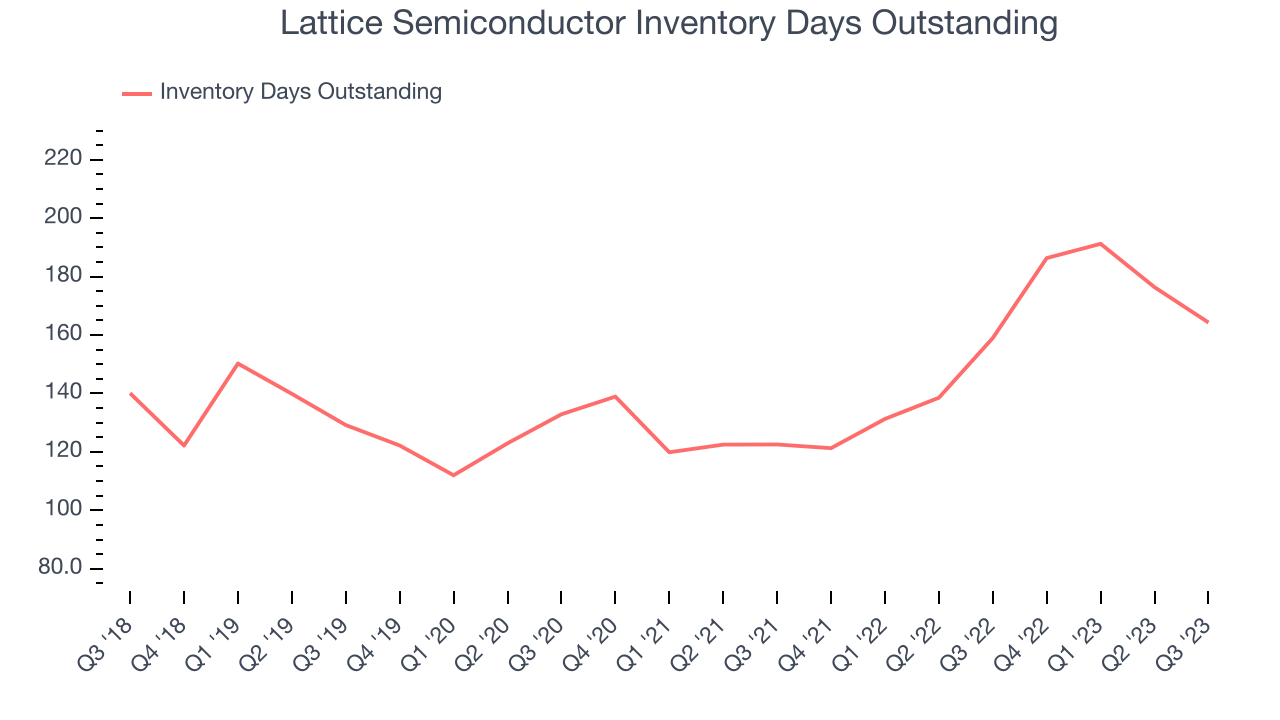

- Inventory Days Outstanding: 164, down from 176 in the previous quarter

- Gross Margin (GAAP): 70%, up from 68.8% in the same quarter last year

Jim Anderson, president and CEO, said, "We delivered another quarter of solid growth, with Q3 2023 revenue and net income increasing 11% on a year-over-year basis. Today Lattice has the strongest product portfolio in our 40-year history and we continue to rapidly expand our product lineup. We look forward to our Developers Conference in December, when we expect to launch two new members of the Lattice Avant™ mid-range FPGA product family. "

A global leader in its category, Lattice Semiconductor (NASDAQ:LSCC) is a semiconductor designer specializing in customer-programmable chips that enhance CPU performance for intensive tasks such as machine learning.

Processors and Graphics Chips

The biggest demand drivers for processors (CPUs) and graphics chips at the moment are secular trends related to 5G and Internet of Things, autonomous driving, and high performance computing in the data center space, specifically around AI and machine learning. Like all semiconductor companies, digital chip makers exhibit a degree of cyclicality, driven by supply and demand imbalances and exposure to PC and Smartphone product cycles.

Sales Growth

Lattice Semiconductor's revenue growth over the last three years has been strong, averaging 23% annually. But as you can see below, this quarter wasn't particularly strong, with revenue growing from $172.5 million in the same quarter last year to $192.2 million. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Lattice Semiconductor had an average quarter as its revenue grew 11.4% year on year, in line with analysts' estimates. However, this was its third consecutive quarter of decelerating growth, potentially indicating a coming cycle downturn.

Although Lattice Semiconductor's revenue growth has decelerated over the past three quarters, its management team thinks it will continue growing next quarter. The company is guiding to 0.02% year-on-year growth, which is relatively in line with analysts' estimates of 11.6% growth over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Lattice Semiconductor's DIO came in at 164, which is 24 days above its five-year average. These numbers suggest that despite the recent decrease, the company's inventory levels are higher than what we've seen in the past.

Key Takeaways from Lattice Semiconductor's Q3 Results

Sporting a market capitalization of $9.67 billion, Lattice Semiconductor is among smaller companies, but its more than $114.4 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We were glad Lattice Semiconductor's revenue and EPS outperformed Wall Street's estimates, even if the beats weren't too big. It was also good to see an improvement in Lattice Semiconductor's inventory levels. On the other hand, its revenue guidance for next quarter underwhelmed, and this is where the market is focused and why the stock is weak. The industry has seen some choppy results, starting with bellwether Texas Instruments and continuing with ON Semiconductor. Overall, the results could have been better. The company is down 12.3% on the results and currently trades at $59 per share.

So should you invest in Lattice Semiconductor right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.