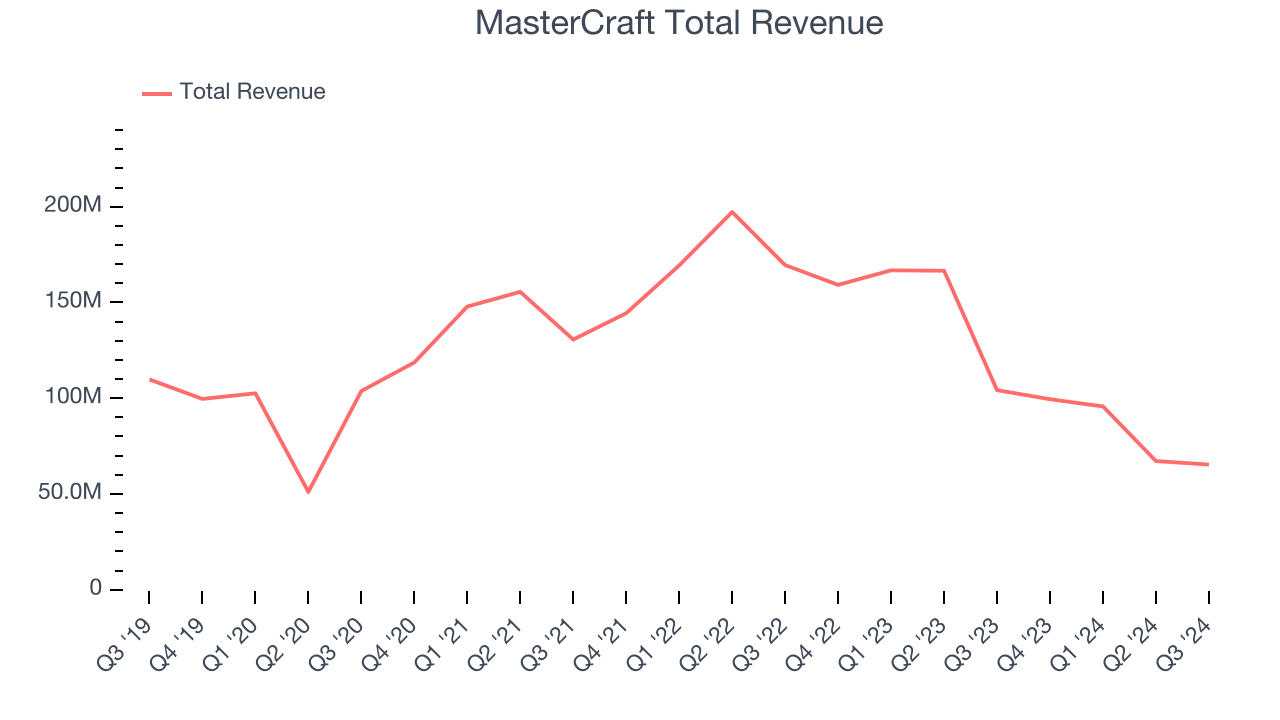

Sport boat manufacturer MasterCraft (NASDAQ:MCFT) reported Q3 CY2024 results beating Wall Street’s revenue expectations, but sales fell 37.3% year on year to $65.36 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $60 million was less impressive, coming in 1.1% below expectations. Its non-GAAP profit of $0.12 per share was also 320% above analysts’ consensus estimates.

Is now the time to buy MasterCraft? Find out by accessing our full research report, it’s free.

MasterCraft (MCFT) Q3 CY2024 Highlights:

- Revenue: $65.36 million vs analyst estimates of $61.25 million (6.7% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.03 ($0.09 beat)

- EBITDA: $3.84 million vs analyst estimates of $2.46 million (56.1% beat)

- The company slightly lifted its revenue guidance for the full year to $285 million at the midpoint from $282.5 million

- Management raised its full-year Adjusted EPS guidance to $0.75 at the midpoint, a 22% increase

- EBITDA guidance for the full year is $21.5 million at the midpoint, above analyst estimates of $21.28 million

- Gross Margin (GAAP): 18.1%, down from 21% in the same quarter last year

- Operating Margin: 1.5%, down from 8.2% in the same quarter last year

- EBITDA Margin: 5.9%, down from 11.7% in the same quarter last year

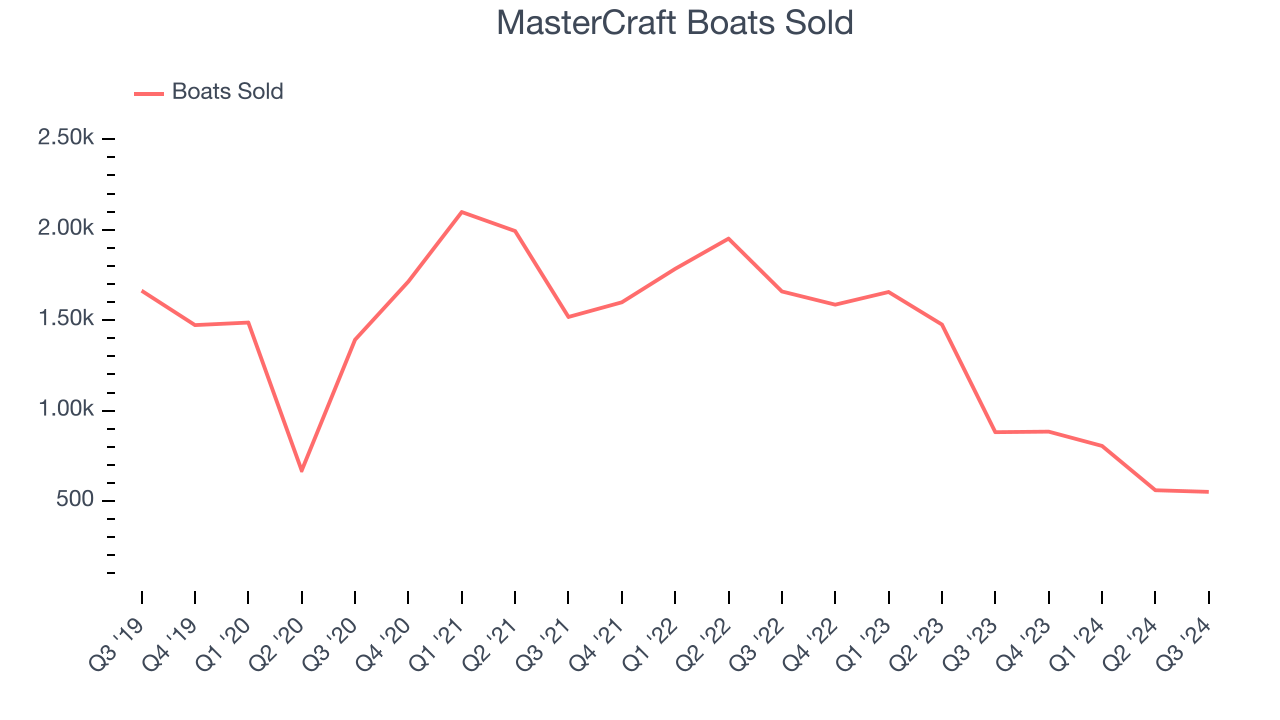

- Boats Sold: 551, down 330 year on year

- Market Capitalization: $292.8 million

Brad Nelson, Chief Executive Officer, commented, “Our business executed well during the first quarter as we delivered results above expectations despite facing a backdrop of continued economic and industry headwinds. Our strong quarter was led by significant progress rebalancing dealer inventories and sets a strong foundation for the rest of the fiscal year. With the summer selling season now complete, we are focused on shipping our enhanced product ahead of the boat show season, while we continue to carefully manage dealer health.”

Company Overview

Started by a waterskiing instructor, MasterCraft (NASDAQ:MCFT) specializes in designing, manufacturing, and selling sport boats.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

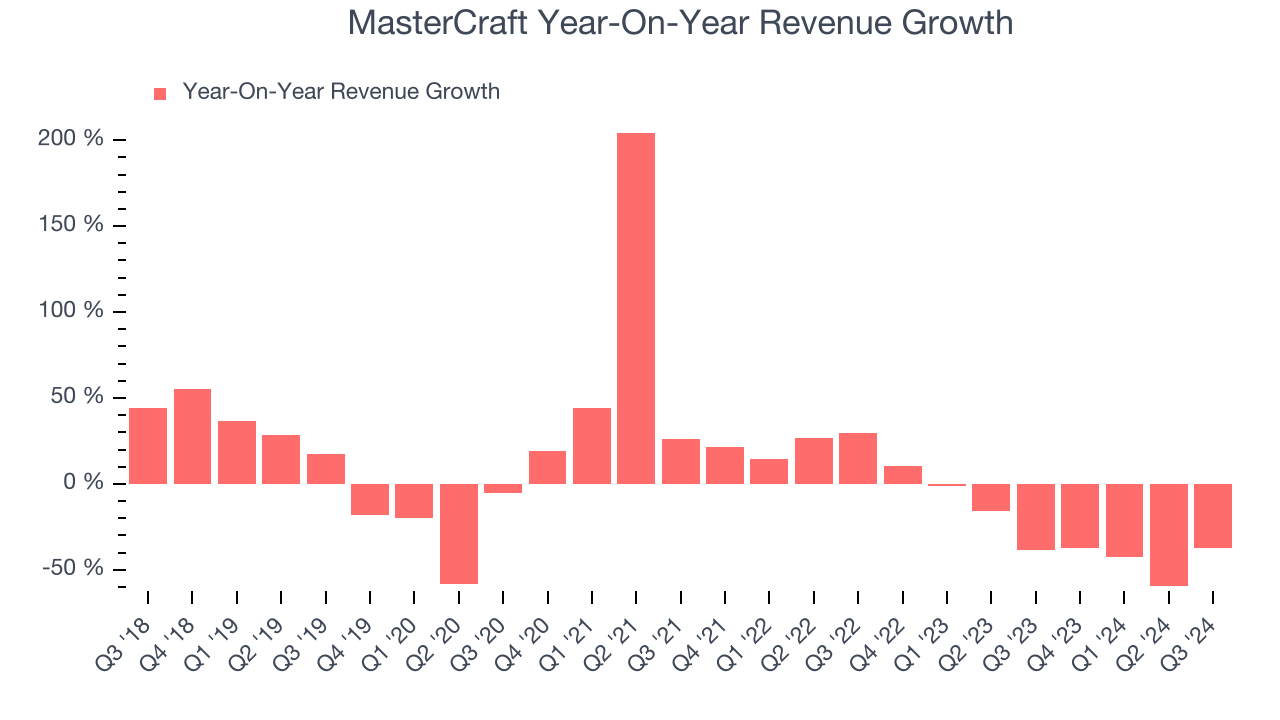

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. MasterCraft struggled to generate demand over the last five years as its sales dropped by 7.4% annually, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. MasterCraft’s recent history shows its demand has stayed suppressed as its revenue has declined by 30.6% annually over the last two years.

We can better understand the company’s revenue dynamics by analyzing its number of boats sold, which reached 551 in the latest quarter. Over the last two years, MasterCraft’s boats sold averaged 34.3% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, MasterCraft’s revenue fell 37.3% year on year to $65.36 million but beat Wall Street’s estimates by 6.7%. Management is currently guiding for a 39.7% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to decline 9.8% over the next 12 months. Although this projection is better than its two-year trend it's tough to feel optimistic about a company facing demand difficulties.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

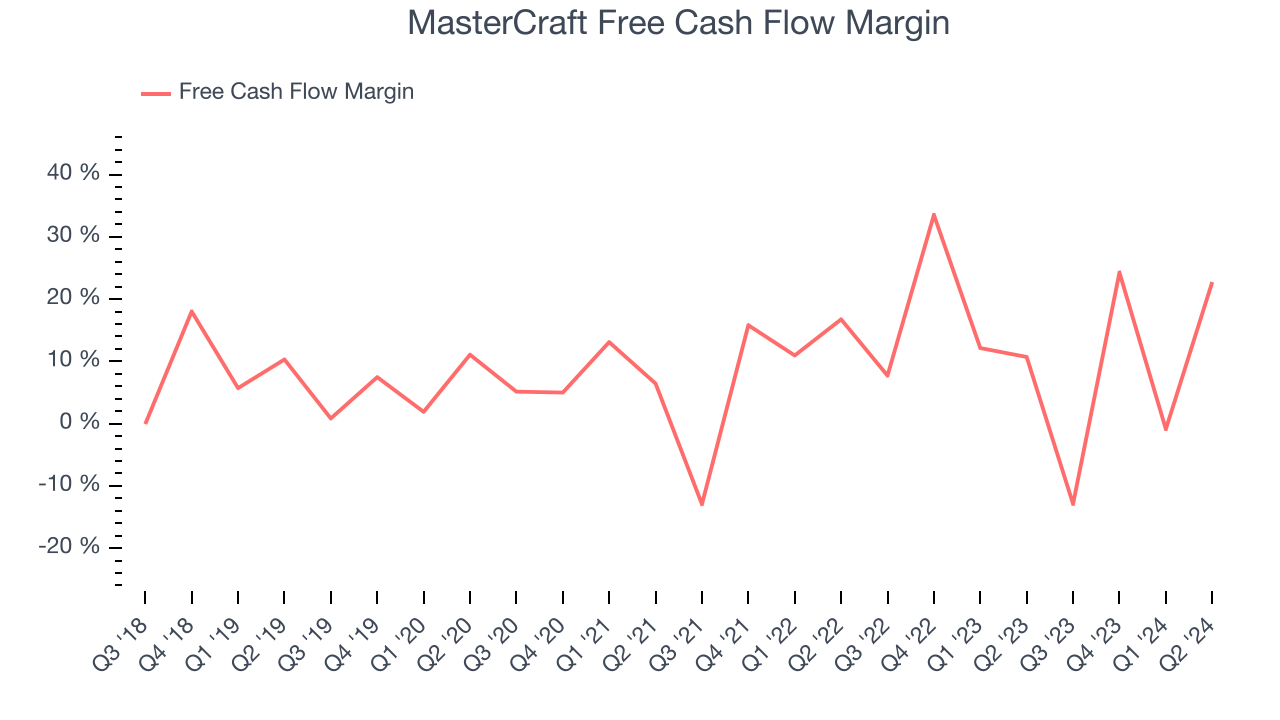

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

MasterCraft has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 13.6% over the last two years, better than the broader consumer discretionary sector.

The company’s cash burn increased from $13.44 million of lost cash in the same quarter last year . These numbers deviate from its longer-term margin, raising some eyebrows.

Key Takeaways from MasterCraft’s Q3 Results

We were impressed by how significantly MasterCraft blew past analysts’ EBITDA and EPS expectations this quarter. We were also excited that the company raised both its full year revenue and EPS guidance. On the other hand, its number of boats sold missed expectations, but this seems to be forgiven by the market. Overall, we think this was still a solid quarter with some key metrics above expectations. The stock traded up 4.9% to $18.50 immediately following the results.

MasterCraft had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.