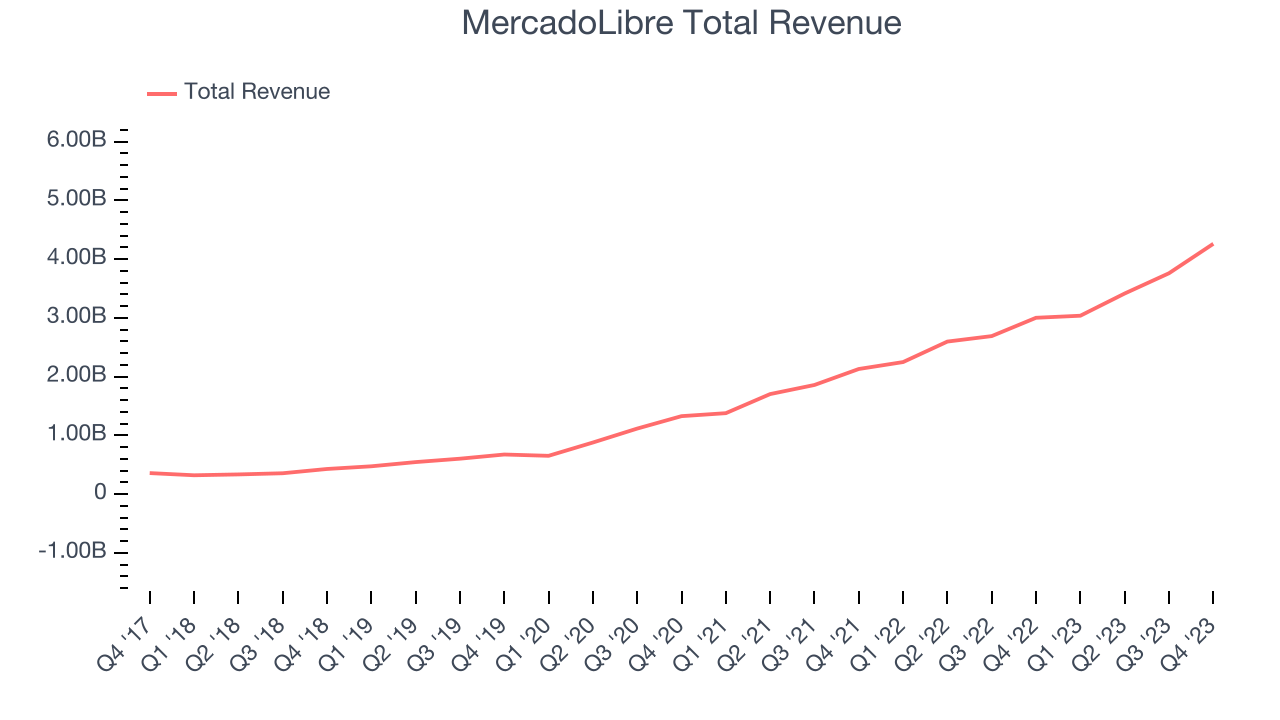

Latin American e-commerce and fintech company MercadoLibre (NASDAQ:MELI) reported Q4 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 41.9% year on year to $4.26 billion. Its GAAP profit of $3.25 per share was flat year on year.

MercadoLibre (MELI) Q4 FY2023 Highlights:

- Revenue: $4.26 billion vs analyst estimates of $4.13 billion (3.2% beat)

- EPS: $3.25 vs analyst estimates of $6.96 (53.3% miss)

- Free Cash Flow of $1.75 billion, up 114% from the previous quarter

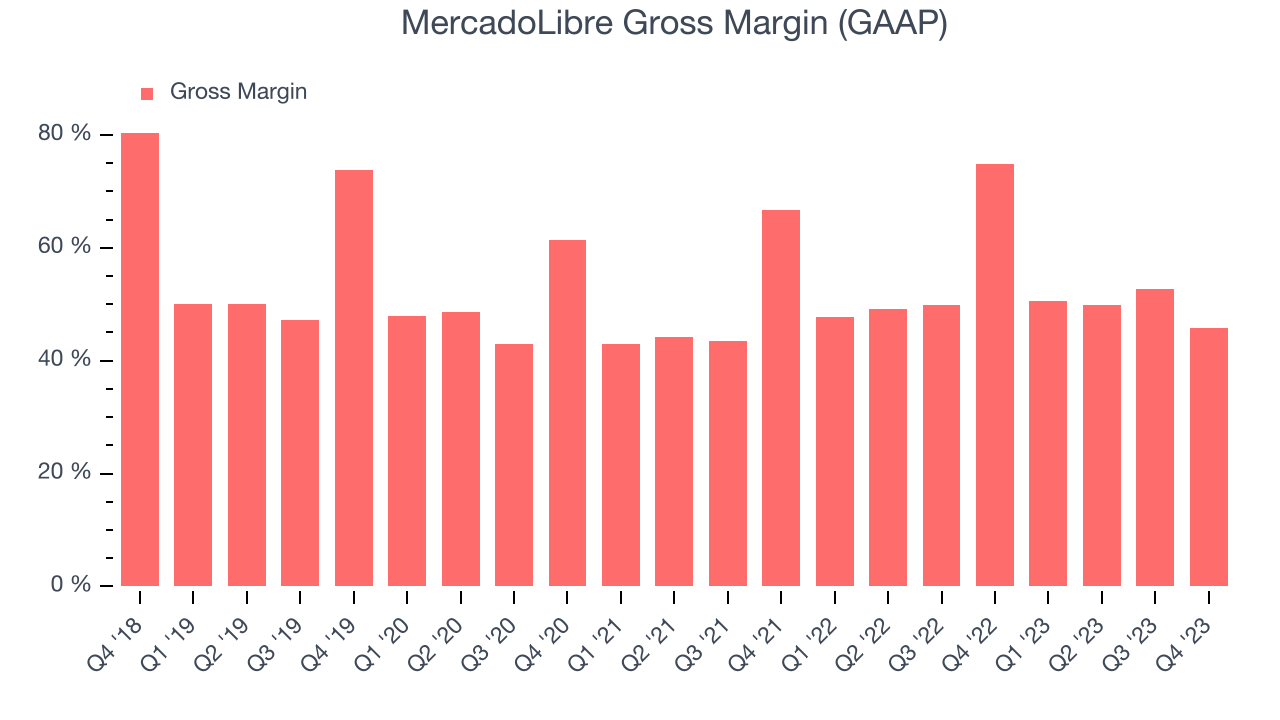

- Gross Margin (GAAP): 45.9%, down from 74.9% in the same quarter last year

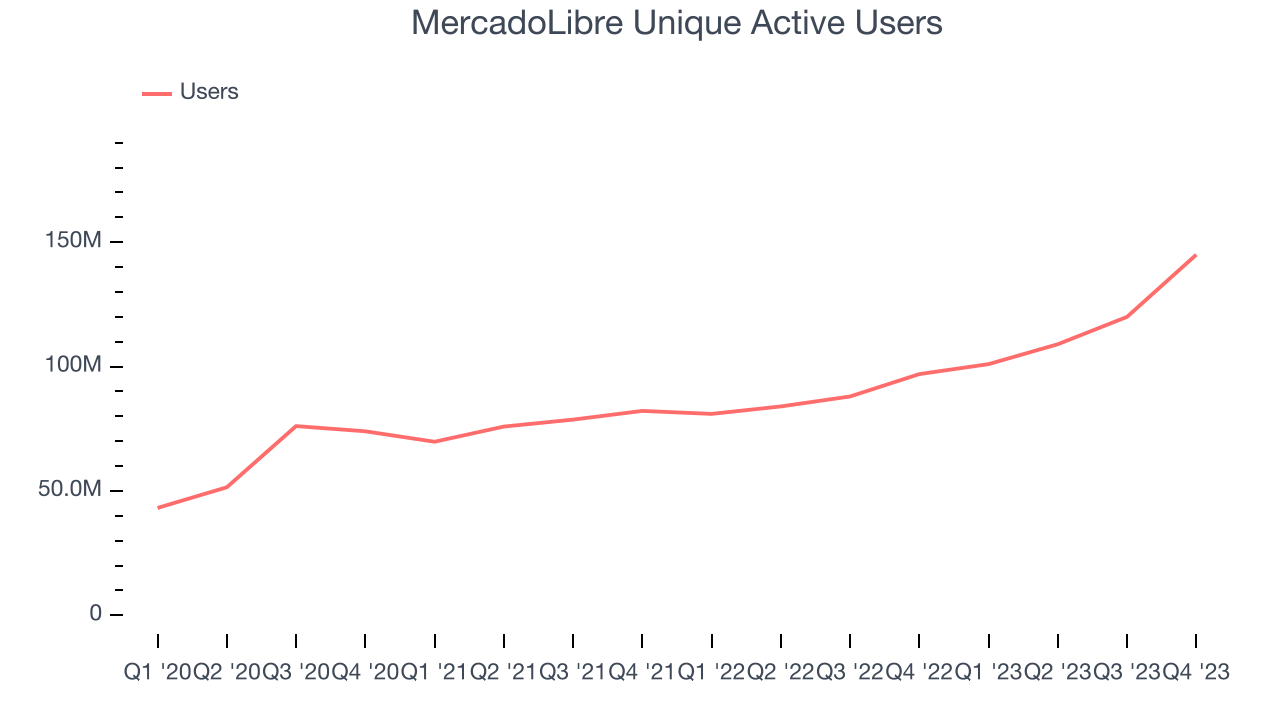

- Unique Active Users: 145 million, up 48 million year on year

- Total Payment Volume: $56.5 billion vs analyst estimates of $49 billion (15.3% beat)

- Gross Merchandise Volume: $13.5 billion vs analyst estimates of $12.4 billion (8.9% beat)

- Market Capitalization: $87.86 billion

Originally started as an online auction platform, MercadoLibre (NASDAQ:MELI) is a one-stop e-commerce marketplace and fintech platform in Latin America.

The company connects buyers and sellers in the majority of countries across the continent. MercadoLibre allows buyers to browse and purchase products ranging from furniture to groceries, while sellers can list products and access tools to manage online stores. The company also offers payment and shipping solutions, as well as financial services such as loans through subsidiary MercadoPago.

MercadoLibre addresses the lack of a reliable and convenient e-commerce platform in Latin America. Before MercadoLibre, consumers in the region had to rely on traditional stores or informal markets to purchase goods, which often meant time spent going from one physical location to another, limited options, and sometimes uncompetitive prices. Sellers could only reach buyers who were close enough to physically visit their store or stand. MercadoLibre therefore provides a convenient and trusted way for consumers to shop online, while also allowing sellers to reach a wider audience.

MercadoLibre generates revenue primarily through commissions on transactions, as the company holds no inventory. For example, when a seller makes a sale, MercadoLibre charges a commission ranging from mid-single-digits percentages to mid-teens percentages, depending on the category and sales volume. Advertising and its fintech services are additional sources of revenue.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors operating similar platforms include Amazon.com (NASDAQ:AMZN), Alibaba (NYSE:BABA), and eBay (NASDAQ:EBAY).Sales Growth

MercadoLibre's revenue growth over the last three years has been exceptional, averaging 56.8% annually. This quarter, MercadoLibre beat analysts' estimates and reported impressive 41.9% year-on-year revenue growth.

Usage Growth

As an online marketplace, MercadoLibre generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, MercadoLibre's daily active users, a key performance metric for the company, grew 24.6% annually to 145 million. This is fast growth for a consumer internet company.

In Q4, MercadoLibre added 48 million daily active users, translating into 49.5% year-on-year growth.

Revenue Per User

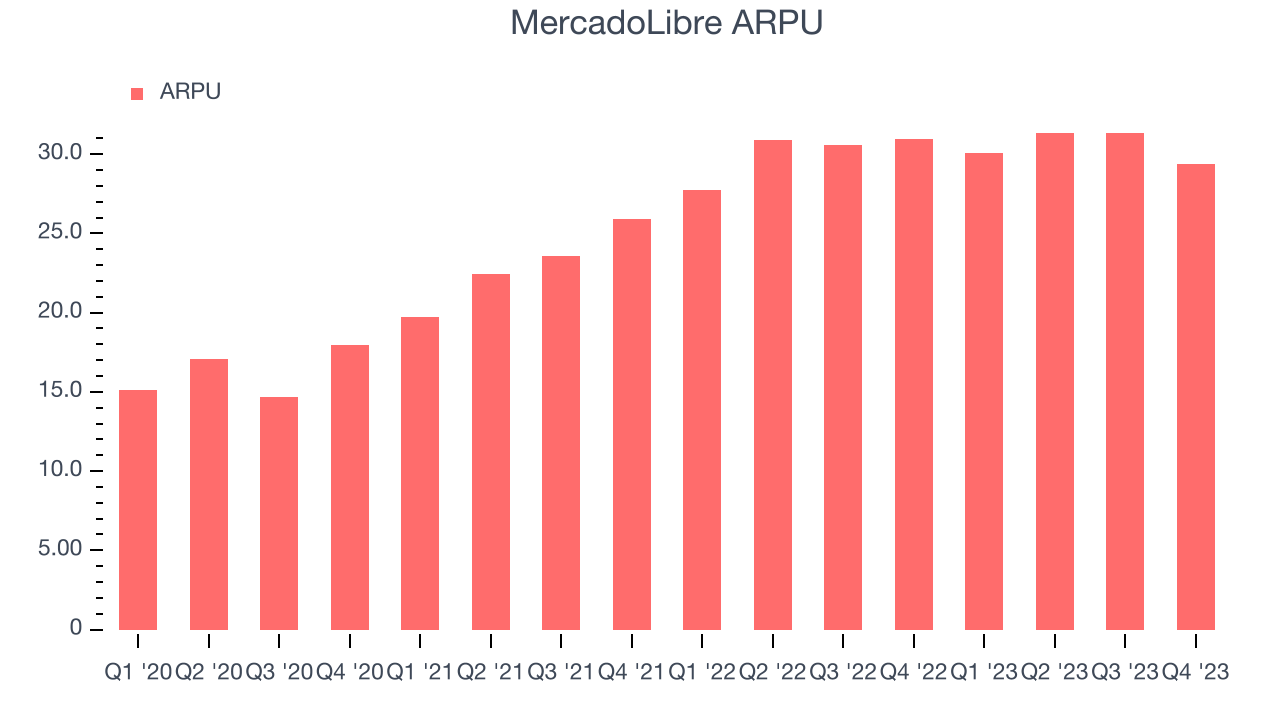

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like MercadoLibre because it measures how much the company earns in transaction fees from each user. Furthermore, ARPU gives us unique insights as it's a function of a user's average order size and MercadoLibre's take rate, or "cut", on each order.

MercadoLibre's ARPU growth has been excellent over the last two years, averaging 16.8%. The company's ability to increase prices while growing its daily active users at such a fast rate reflects the strength of its platform, as its users are spending significantly more than last year. This quarter, ARPU declined 5% year on year to $29.39 per user.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor.

MercadoLibre's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 45.9% this quarter, down 29 percentage points year on year.

For online marketplaces like MercadoLibre, these aforementioned costs typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification. After paying for these expenses, MercadoLibre had $0.46 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

MercadoLibre's gross margins have been trending down over the past year, averaging 49.6%. This weakness isn't great as MercadoLibre's margins are already slightly below other consumer internet companies and falling margins point to potentially deteriorating pricing power.

User Acquisition Efficiency

Unlike enterprise software that's typically sold by dedicated sales teams, consumer internet businesses like MercadoLibre grow from a combination of product virality, paid advertisement, and incentives.

MercadoLibre is very efficient at acquiring new users, spending only 24.2% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a strong brand reputation and customer acquisition advantages from scale, giving MercadoLibre the freedom to invest its resources into new growth initiatives while maintaining optionality.

Profitability & Free Cash Flow

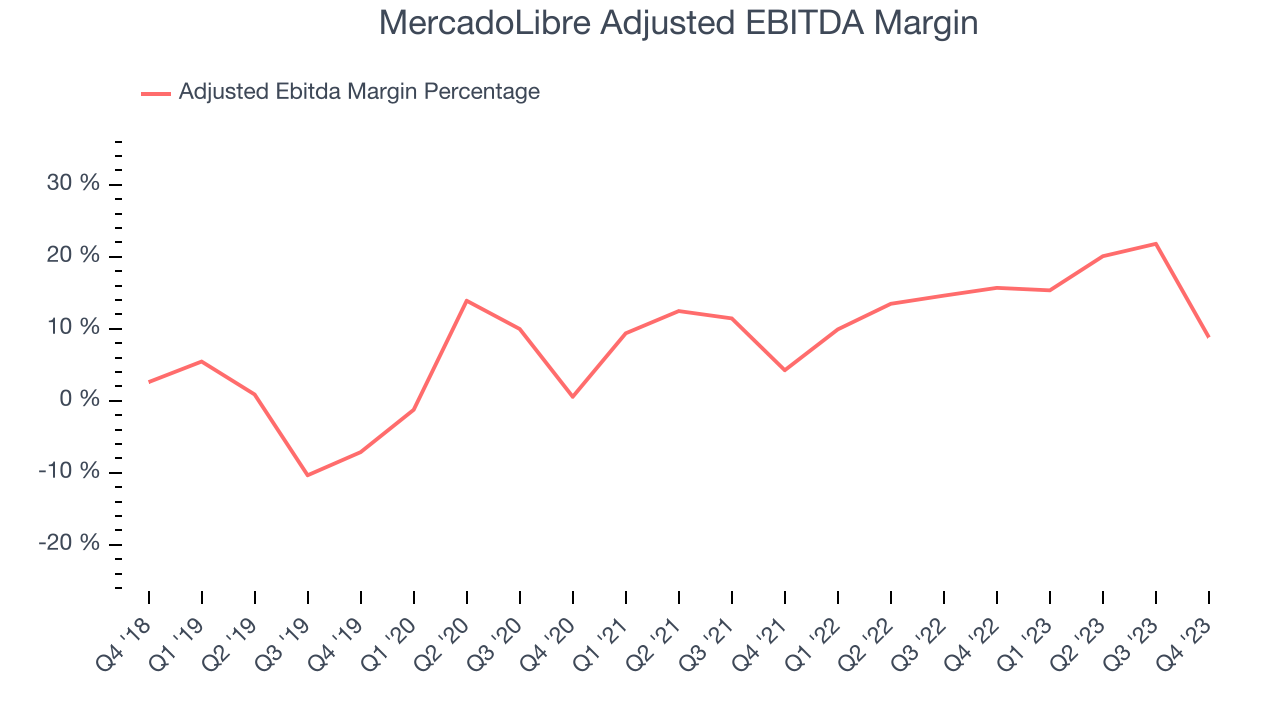

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

MercadoLibre's EBITDA was $375 million this quarter, translating into a 8.8% margin. Furthermore, MercadoLibre has shown strong profitability over the last four quarters, with average EBITDA margins of 16.2%.

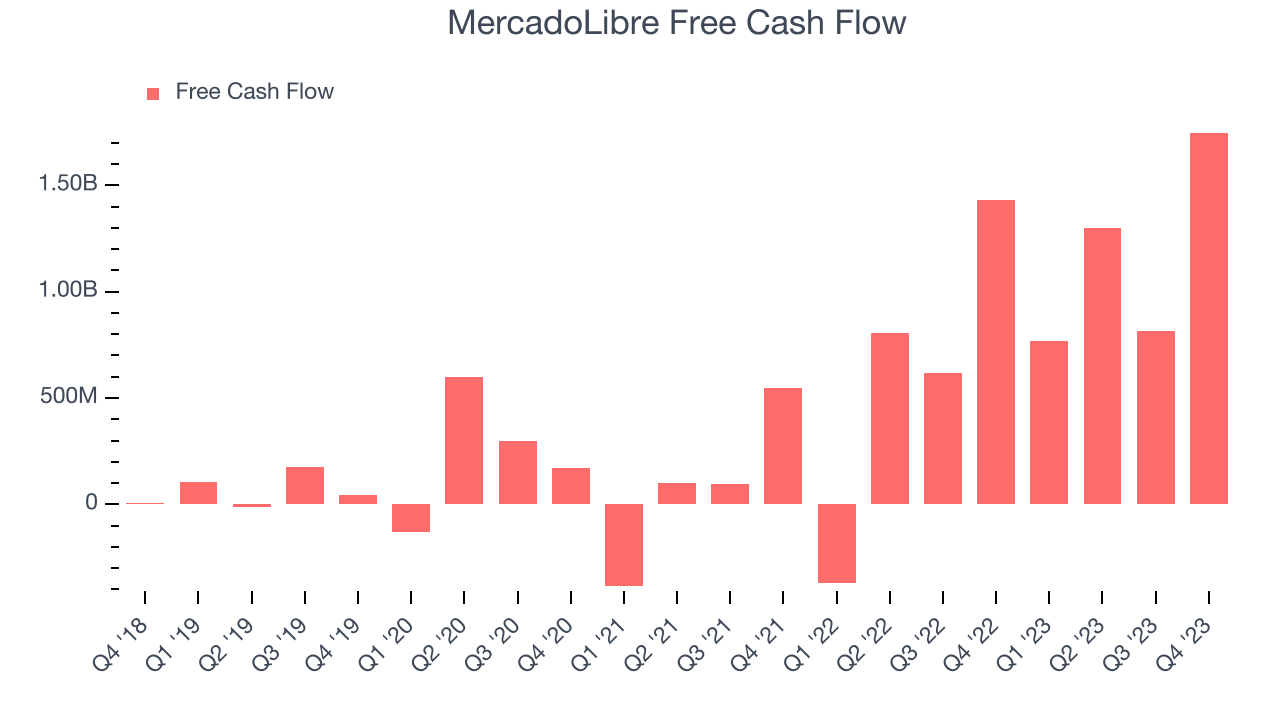

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. MercadoLibre's free cash flow came in at $1.75 billion in Q4, up 22.2% year on year.

MercadoLibre has generated $4.63 billion in free cash flow over the last 12 months, an eye-popping 32% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Key Takeaways from MercadoLibre's Q4 Results

We were impressed by MercadoLibre's robust user growth this quarter, enabling it to beat analysts' revenue, total payment volume (TPV), and gross merchandise volume (GMV) estimates. Specifically for TPV, the company's new credit card offering for its Brazil and Mexico customers stood out, helping accelerate off-platform TPV growth to 64% year on year in Q4 vs 55% growth for the full year 2023 (off-platform refers to payments transacted outside its e-commerce marketplace). Profitability across its entire credit book rose to nearly a 40% margin, which is also quite impressive. We believe MELI achieved this profitability because it can underwrite its customers better than traditional banks through its access to granular transaction-level data from its commerce business.

Double-clicking into the commerce business, two segments stood out during the quarter: Logistics and Advertising. On the Logistics side, MELI delivered more items per vehicle in 2023 as customers increasingly utilized its new MELI+ loyalty program (similar to Amazon Prime, the company re-launched MELI+ in 2023). The increased deliveries per vehicle boosted the company's efficiency, and it ended 2023 having shipped over 50% of all e-commerce orders in Brazil and over 80% of all e-commerce orders in Mexico. Furthermore, it fulfilled 52% of orders in one day or less and 75% within 48 hours. On the nascent but rapidly growing advertising side of the business, MercadoLibre added 50,000 new advertisers to its platform in 2023 and grew its advertising revenue by 70% year on year.

We think this was a great quarter that should delight shareholders, but the market is likely weary of the company's headline numbers, where its operating margin missed analysts' estimates by a wide margin. Looking under the hood, however, we can see that its lower profitability was caused by 1) non-recurring, non-cash expenses of $351 million that are mostly related to outstanding tax liabilities from a 2014 court case it had with the Brazilian federal tax authority, 2) lower Logistics segment margins as it offered more free shipping to customers in Brazil and Mexico through MELI+, and 3) strong growth in its 1P commerce business (61% year-on-year growth), which has lower margins than its 3P marketplace business because in 1P, the company buys and holds inventory on its balance sheet.

We believe each of the concerns above does not impact MELI's fundamentals, and in the cases of points 2 and 3, actually makes the company more attractive. The lower Logistics segment margins may impact profit margins in the near term, but the fast growth the company saw in its MELI+ program paves the way for higher customer lifetime value over the long term as it gives the company predictable subscription revenue and customer loyalty. Regarding the 1P commerce business, we still believe it is a great opportunity for the company despite its lower margins because it fills key product assortment gaps, is additive to overall profit dollars, and bolsters the company's market position.

Although the stock is down 8.1% after reporting because of its lower-than-expected operating margin, our analysis shows the reasons for the margin compression do not impact the company's fundamentals. MELI is expanding its competitive moat while operating with strength and momentum.

Is Now The Time?

When considering an investment in MercadoLibre, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

There are numerous reasons why we think MercadoLibre is one of the best consumer internet companies out there. While we'd expect growth rates to moderate from here, its revenue growth has been exceptional over the last three years. Additionally, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits and its user acquisition efficiency is best in class.

At the moment MercadoLibre trades at 25.8x next 12 months EV-to-EBITDA. Looking at the consumer internet landscape today, MercadoLibre's qualities really stand out, and we really like it at this price.

Wall Street analysts covering the company had a one-year price target of $1,881 per share right before these results (compared to the current share price of $1,674), implying they saw upside in buying MercadoLibre in the short term.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.