Online survey platform Momentive (NASDAQ:MNTV) reported results in line with analyst expectations in Q3 FY2021 quarter, with revenue up 20.2% year on year to $114.7 million. Momentive made a GAAP loss of $22.9 million, improving on its loss of $26.1 million, in the same quarter last year.

Is now the time to buy Momentive? Access our full analysis of the earnings results here, it's free.

Momentive (MNTV) Q3 FY2021 Highlights:

- Revenue: $114.7 million vs analyst estimates of $113.8 million (small beat)

- EPS (non-GAAP): $0.03 vs analyst estimates of $0.01 ($0.02 beat)

- Free cash flow of $14.6 million, down 38.3% from previous quarter

- Customers: 883,100, up from 862,200 in previous quarter

- Gross Margin (GAAP): 80.6%, up from 77% same quarter last year

Previously known as SurveyMonkey, Momentive (NASDAQ:MNTV) offers software as a service that makes it easy for users create, manage and distribute online surveys.

A lot of research used to be done in person using pen and paper, so Momentive might somewhat benefit from an environment where work is done remotely. But the biggest driver of the business is an increased pressure on efficiency of marketing budgets, as more teams now do the research in-house using do-it-yourself tools rather than hiring an outside agency to do it.

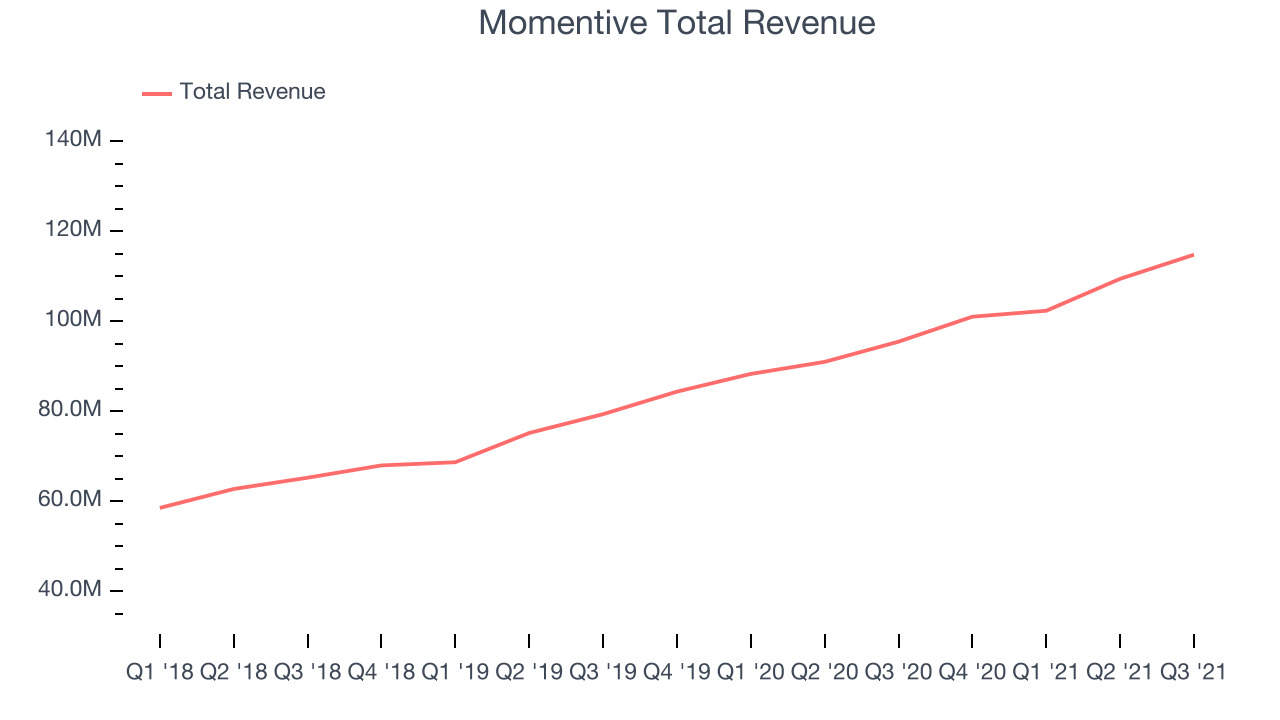

Sales Growth

As you can see below, Momentive's revenue growth has been moderate over the last year, growing from quarterly revenue of $95.4 million, to $114.7 million.

This quarter, Momentive's quarterly revenue was once again up a very solid 20.2% year on year. But the growth did slow down compared to last quarter, as the revenue increased by just $5.36 million in Q3, compared to $7.09 million in Q2 2021. We'd like to see revenue increase by a greater amount each quarter, but a one-off fluctuation is usually not concerning.

Analysts covering the company are expecting the revenues to grow 19% over the next twelve months, although estimates are likely to change post earnings.

There are others doing even better than Momentive. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 400% since the IPO in December. You can find it on our platform for free.

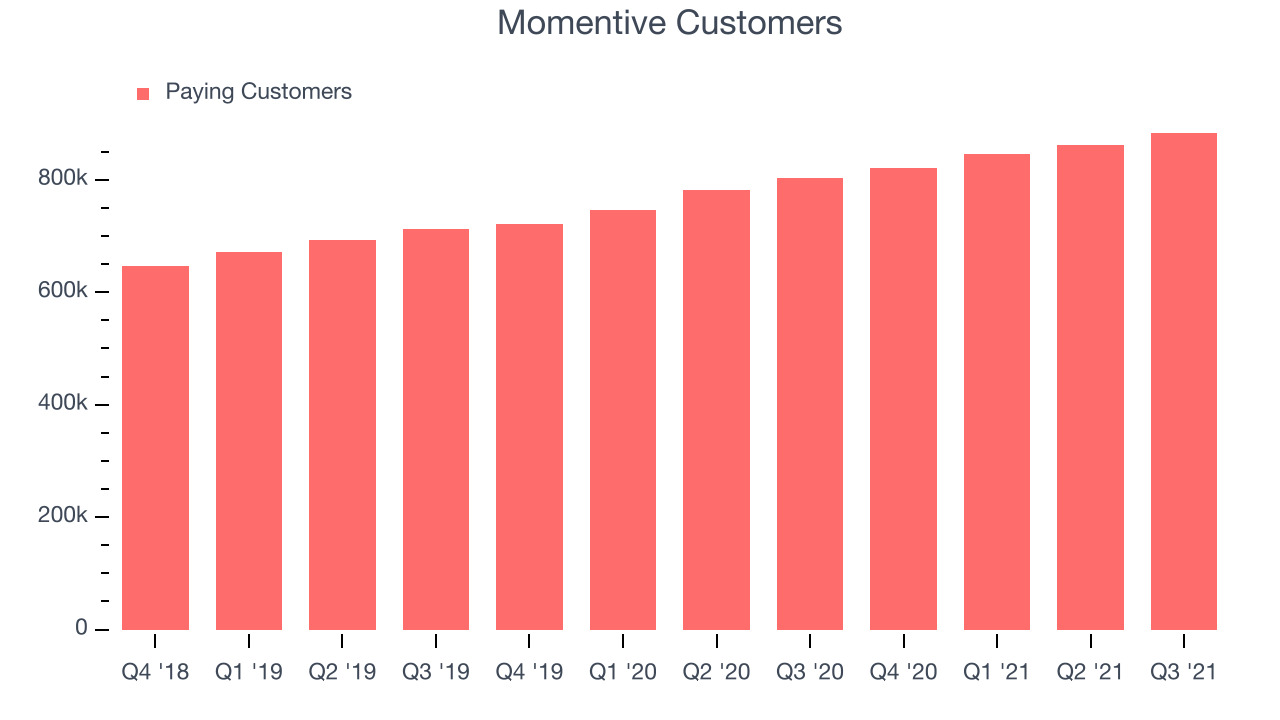

Customer Growth

You can see below that Momentive reported 883,100 customers at the end of the quarter, an increase of 20,900 on last quarter. That is quite a bit better customer growth than last quarter and in line with what we have seen in previous quarters, demonstrating the company has the sales momentum required to drive continued growth. We've no doubt shareholders will take this as an indication that the company's go-to-market strategy is running smoothly.

Key Takeaways from Momentive's Q3 Results

With a market capitalization of $3.29 billion Momentive is among smaller companies, but its more than $300.6 million in cash and positive free cash flow over the last twelve months give us confidence that Momentive has the resources it needs to pursue a high growth business strategy.

It was great to see that Momentive’s customer growth is accelerating. That feature of these results really stood out as a positive. Zooming out, we think this was a decent quarter, showing the company is staying on target. The company is flat on the results and currently trades at $22.23 per share.

Should you invest in Momentive right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.