Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Monolithic Power Systems (NASDAQ:MPWR) and its peers.

Demand for analog chips is generally linked to the overall level of economic growth, as analog chips serve as the building blocks of most electronic goods and equipment. Unlike digital chip designers, analog chip makers tend to produce the majority of their own chips, as analog chip production does not require expensive leading edge nodes. Less dependent on major secular growth drivers, analog product cycles are much longer, often 5-7 years.

The 15 analog semiconductors stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 1% while next quarter’s revenue guidance was 1.2% below.

The Fed cut its policy rate by 50bps (half a percent) in September 2024, the first in roughly four years. This marks the end of its most pointed inflation-busting campaign since the 1980s. While CPI (inflation) readings have been supportive lately, employment measures have bordered on worrisome. The markets will be assessing whether this rate cut's timing (and more potential ones in 2024 and 2025) is ideal for supporting the economy or a bit too late for a macro that has already cooled too much.

While some analog semiconductors stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1% since the latest earnings results.

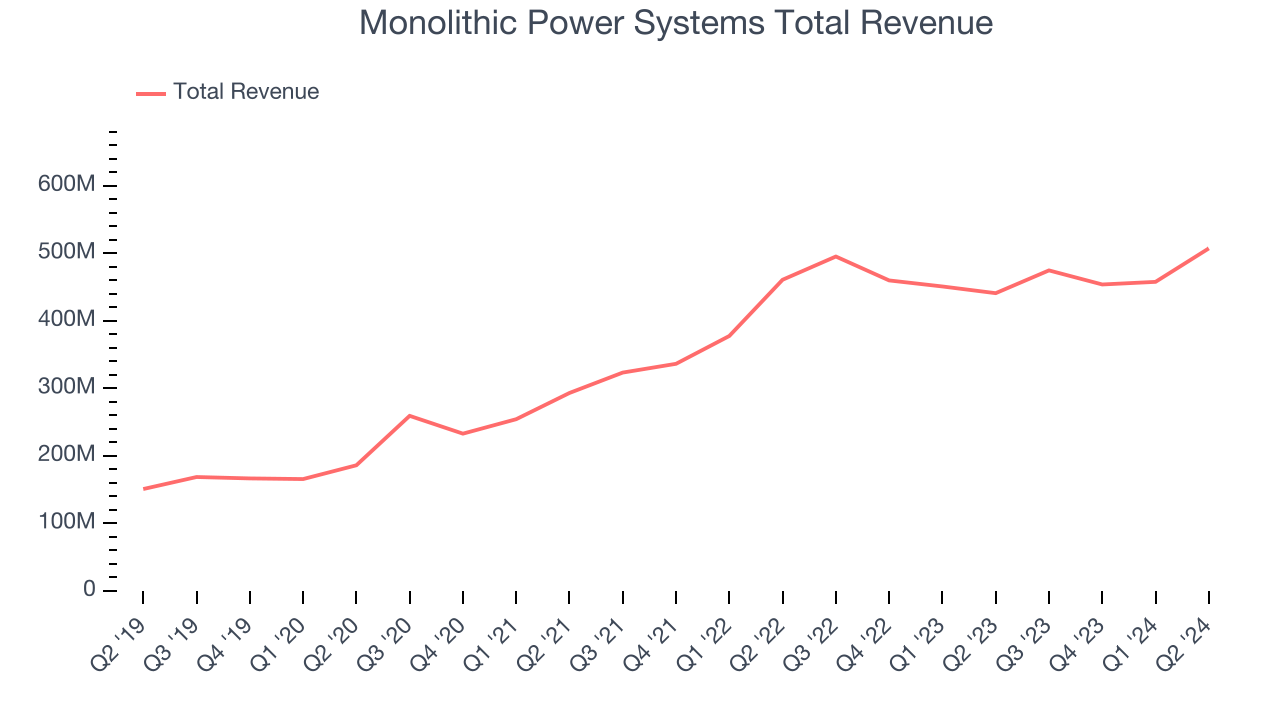

Monolithic Power Systems (NASDAQ:MPWR)

Founded in 1997 by its longtime CEO Michael Hsing, Monolithic Power Systems (NASDAQ:MPWR) is an analog and mixed signal chipmaker that specializes in power management chips meant to minimize total energy consumption.

Monolithic Power Systems reported revenues of $507.4 million, up 15% year on year. This print exceeded analysts’ expectations by 3.4%. Overall, it was a strong quarter for the company with optimistic revenue guidance for the next quarter and a decent beat of analysts’ EPS estimates.

“As we have emphasized for many years, our results reflect the continued success of our proven, long-term growth strategy and our transformation from being only a chip supplier to a full solutions provider,” said Michael Hsing, CEO and founder of MPS.

Interestingly, the stock is up 15.2% since reporting and currently trades at $906.

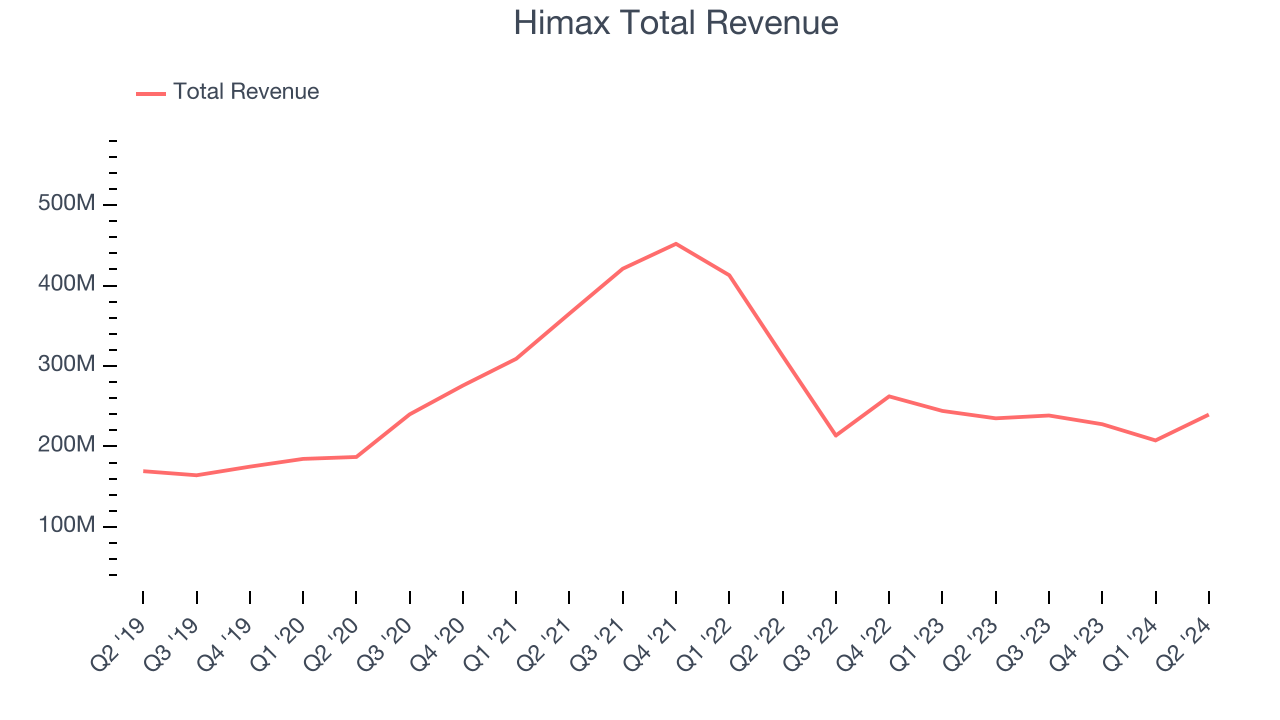

Best Q2: Himax (NASDAQ:HIMX)

Taiwan-based Himax Technologies (NASDAQ:HIMX) is a leading manufacturer of display driver chips and timing controllers used in TVs, laptops, and mobile phones.

Himax reported revenues of $239.6 million, up 2% year on year, outperforming analysts’ expectations by 2.9%. The business had an exceptional quarter with a significant improvement in its gross margin.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.6% since reporting. It currently trades at $5.59.

Is now the time to buy Himax? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Universal Display (NASDAQ:OLED)

Serving major consumer electronics manufacturers, Universal Display (NASDAQ:OLED) is a provider of organic light emitting diode (OLED) technologies used in display and lighting applications.

Universal Display reported revenues of $158.5 million, up 8.1% year on year, in line with analysts’ expectations. It was a softer quarter as it posted a miss of analysts’ EPS estimates and full-year revenue guidance missing analysts’ expectations.

As expected, the stock is down 1.2% since the results and currently trades at $210.

Read our full analysis of Universal Display’s results here.

NXP Semiconductors (NASDAQ:NXPI)

Spun off from Dutch electronics giant Philips in 2006, NXP Semiconductors (NASDAQ: NXPI) is a designer and manufacturer of chips used in autos, industrial manufacturing, mobile devices, and communications infrastructure.

NXP Semiconductors reported revenues of $3.13 billion, down 5.2% year on year. This result was in line with analysts’ expectations. Zooming out, it was a strong quarter as it produced underwhelming revenue guidance for the next quarter and an increase in its inventory levels.

The stock is down 17.2% since reporting and currently trades at $235.12.

Read our full, actionable report on NXP Semiconductors here, it’s free.

Power Integrations (NASDAQ:POWI)

A leading supplier of parts for electronics such as home appliances, Power Integrations (NASDAQ:POWI) is a semiconductor designer and developer specializing in products used for high-voltage power conversion.

Power Integrations reported revenues of $106.2 million, down 13.8% year on year. This print surpassed analysts’ expectations by 1.1%. Zooming out, it was a mixed quarter as it also logged a significant improvement in its inventory levels but underwhelming revenue guidance for the next quarter.

The stock is down 3.6% since reporting and currently trades at $61.88.

Read our full, actionable report on Power Integrations here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.