Marqeta (NASDAQ:MQ) Reports Strong Q4, Stock Jumps 19.1%

Kayode Omotosho /

March 9, 2022

Leading edge card issuer Marqeta (NASDAQ: MQ) beat analyst expectations in Q4 FY2021 quarter, with revenue up 76.2% year on year to $155.4 million. Marqeta made a GAAP loss of $36.8 million, down on its loss of $13.7 million, in the same quarter last year.

Is now the time to buy Marqeta? Access our full analysis of the earnings results here, it's free.

Marqeta (MQ) Q4 FY2021 Highlights:

- Revenue: $155.4 million vs analyst estimates of $137.7 million (12.7% beat)

- EPS (GAAP): -$0.07

- Revenue guidance for Q1 2022 is $161 million at the midpoint, above analyst estimates of $138 million

- Free cash flow was negative $4.61 million, compared to negative free cash flow of $5.61 million in previous quarter

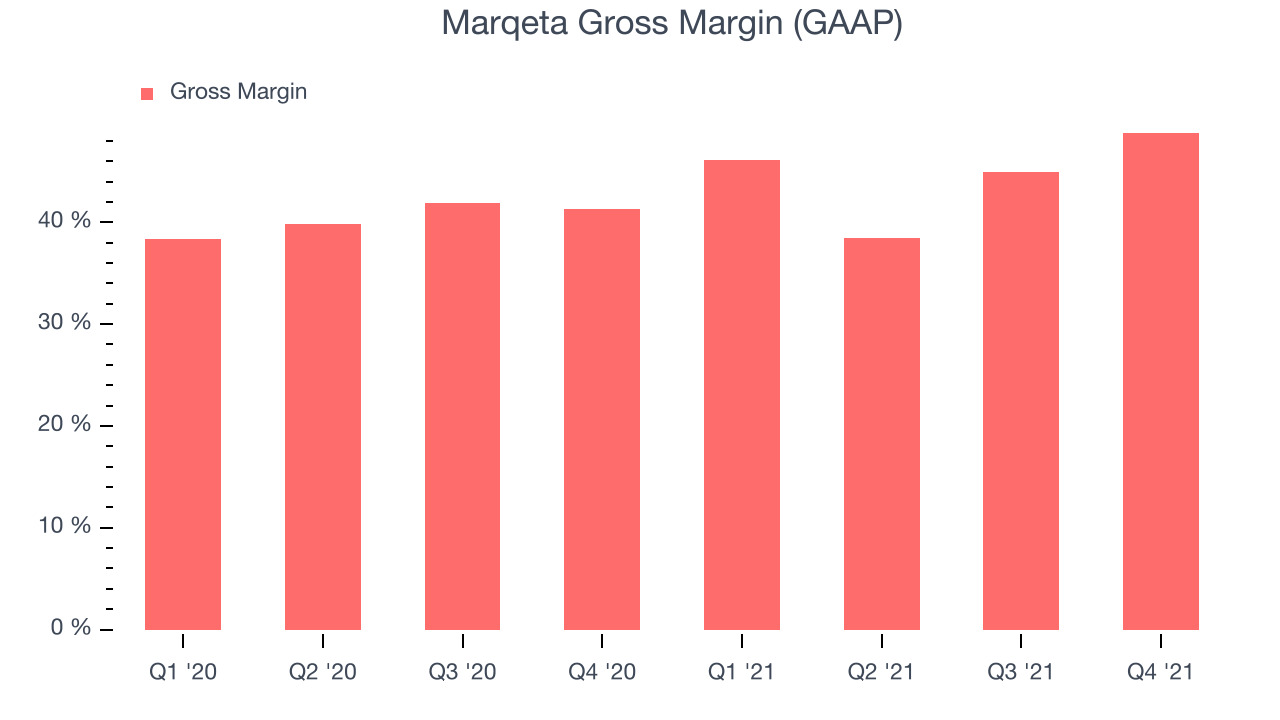

- Gross Margin (GAAP): 48.7%, up from 41.3% same quarter last year

Founded by CEO Jason Gardner in 2009, Marqeta (NASDAQ: MQ) is an innovative card issuer that provides companies with the ability to issue and process virtual, physical, and tokenized credit and debit cards.

Consumers want the ability to make payments whenever and wherever they prefer – and to do so without having to worry about fraud or other security threats. However, building payments infrastructure from scratch is extremely resource-intensive for engineering teams. That drives demand for payments platforms that are easy to integrate into consumer applications and websites.

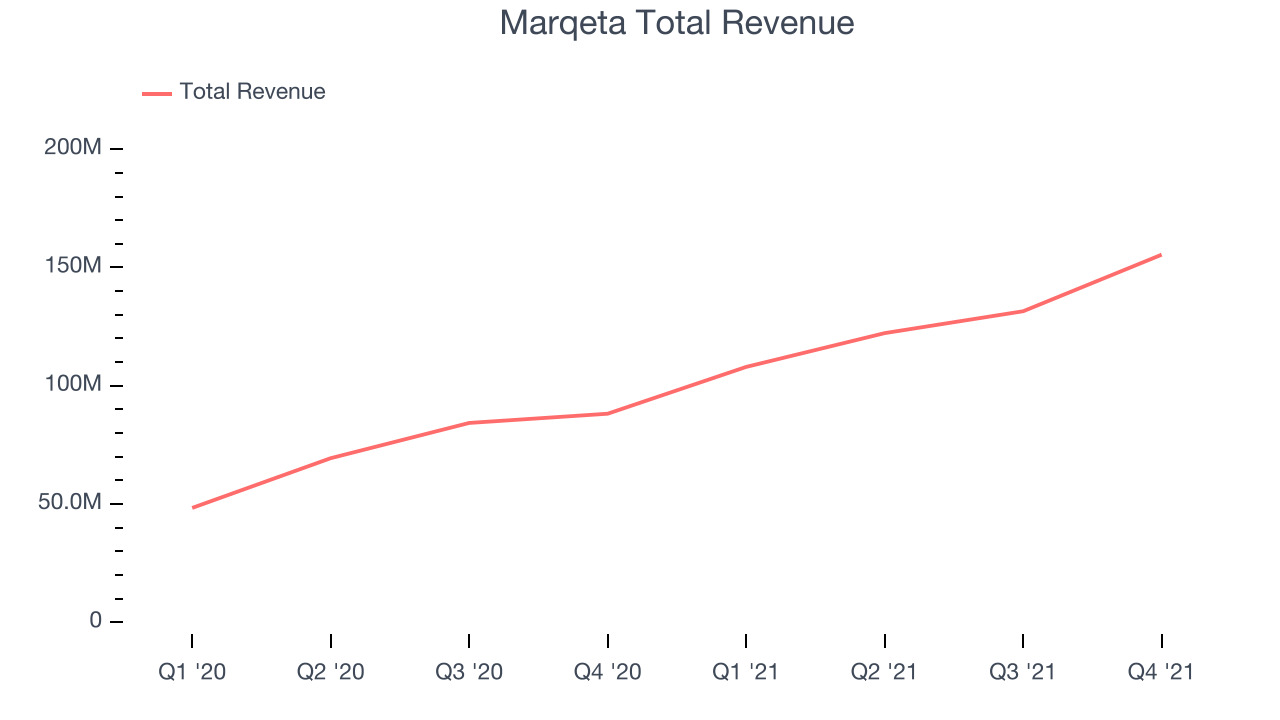

Sales Growth

As you can see below, Marqeta's revenue growth has been incredible over the last year, growing from quarterly revenue of $88.2 million, to $155.4 million.

This was another standout quarter with the revenue up a splendid 76.2% year on year. On top of that, revenue increased $23.9 million quarter on quarter, a very strong improvement on the $9.24 million increase in Q3 2021, and a sign of acceleration of growth, which is very nice to see indeed. Guidance for the next quarter indicates Marqeta is expecting revenue to grow 49% year on year to $161 million.

There are others doing even better than Marqeta. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 150% since the IPO last December. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Marqeta's gross profit margin, an important metric measuring how much money there is left after paying for servers, licenses, technical support and other necessary running expenses was at 48.7% in Q4.

That means that for every $1 in revenue the company had $0.48 left to spend on developing new products, marketing & sales and the general administrative overhead. While it improved significantly from the previous quarter this would still be considered a low gross margin for a SaaS company and we would like to see the improvements continue.

Key Takeaways from Marqeta's Q4 Results

With a market capitalization of $5.25 billion Marqeta is among smaller companies, but its more than $1.24 billion in cash and the fact it is operating close to free cash flow break-even put it in a robust financial position to invest in growth.

We were very impressed by the strong improvements in Marqeta’s gross margin this quarter. And we were also excited to see that it outperformed Wall St’s revenue expectations. Zooming out, we think this impressive quarter should have shareholders feeling very positive. The company is up 19.1% on the results and currently trades at $12.76 per share.

Marqeta may have had a good quarter, so should you invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.