Leading edge card issuer Marqeta (NASDAQ: MQ) reported Q1 CY2024 results topping analysts' expectations, with revenue down 45.7% year on year to $118 million. It made a GAAP loss of $0.07 per share, improving from its loss of $0.13 per share in the same quarter last year.

Is now the time to buy Marqeta? Find out by accessing our full research report, it's free.

Marqeta (MQ) Q1 CY2024 Highlights:

- Revenue: $118 million vs analyst estimates of $116.9 million (small beat)

- EPS: -$0.07 vs analyst expectations of -$0.08 (in line)

- Gross Margin (GAAP): 71.3%, up from 41% in the same quarter last year

- Free Cash Flow was -$6.07 million, down from $16.48 million in the previous quarter

- Market Capitalization: $2.97 billion

"Our business once again showed itself to be on a solid trajectory this quarter," said Simon Khalaf, CEO of Marqeta.

Founded by CEO Jason Gardner in 2009, Marqeta (NASDAQ: MQ) is an innovative card issuer that provides companies with the ability to issue and process virtual, physical, and tokenized credit and debit cards.

Payments Software

Consumers want the ability to make payments whenever and wherever they prefer – and to do so without having to worry about fraud or other security threats. However, building payments infrastructure from scratch is extremely resource-intensive for engineering teams. That drives demand for payments platforms that are easy to integrate into consumer applications and websites.

Sales Growth

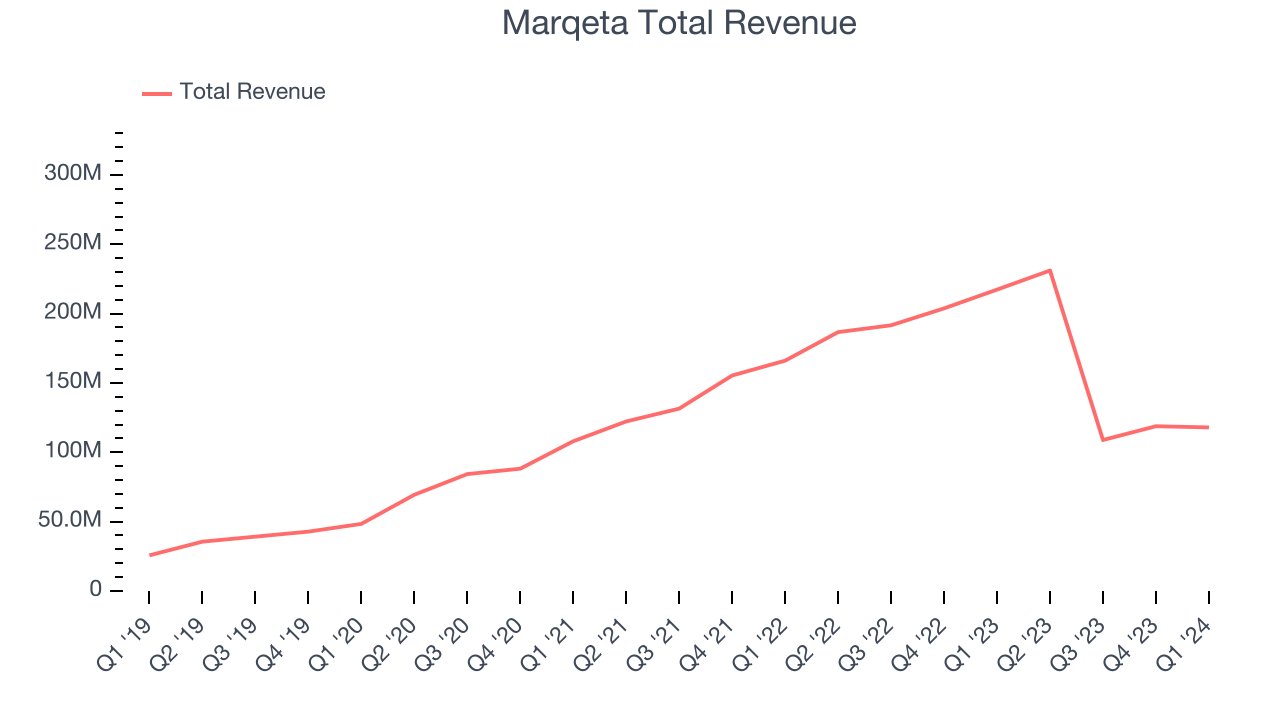

As you can see below, Marqeta's revenue growth has been solid over the last three years, growing from $108 million in Q1 2021 to $118 million this quarter.

This quarter, Marqeta's revenue was down 45.7% year on year, due to a contract renewal with Cash App and resulting change in revenue presentation. The impact of fees owed to Issuing Banks and Card Networks related to the Cash App primary Card Network volume is since Q3 netted against revenue earned from the Cash App program within Net Revenue, negatively impacting the growth rate. In prior periods, these costs were included within Costs of Revenue, so on the other hand Gross Margin has improved significantly.

Looking ahead, Wall Street was expecting revenue to decline 3.4% over the next 12 months before the earnings results announcement.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

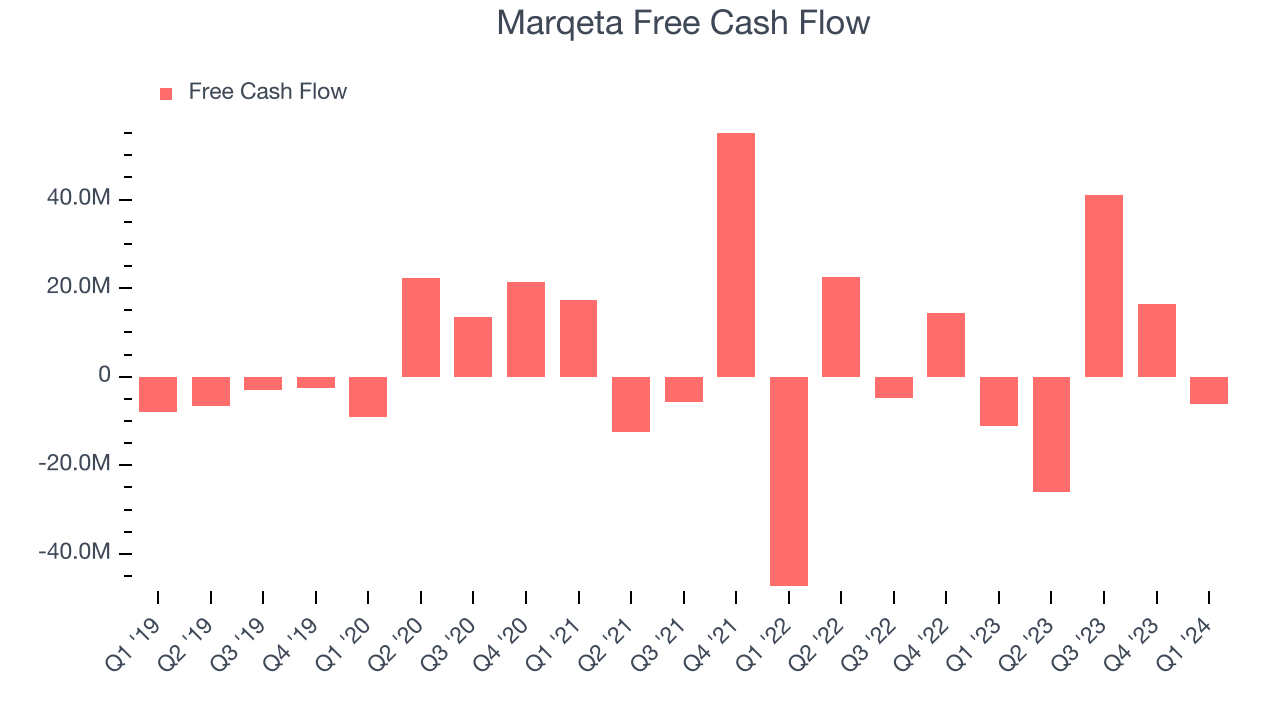

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Marqeta burned through $6.07 million of cash in Q1 , increasing its cash burn by 45.4% year on year.

Marqeta has generated $25.39 million in free cash flow over the last 12 months, or 4.4% of revenue. This FCF margin enables it to reinvest in its business without depending on the capital markets.

Key Takeaways from Marqeta's Q1 Results

Zooming out, we think this was a decent quarter, showing that the company is staying on target. The stock is up 3.8% after reporting and currently trades at $6.05 per share.

So should you invest in Marqeta right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.