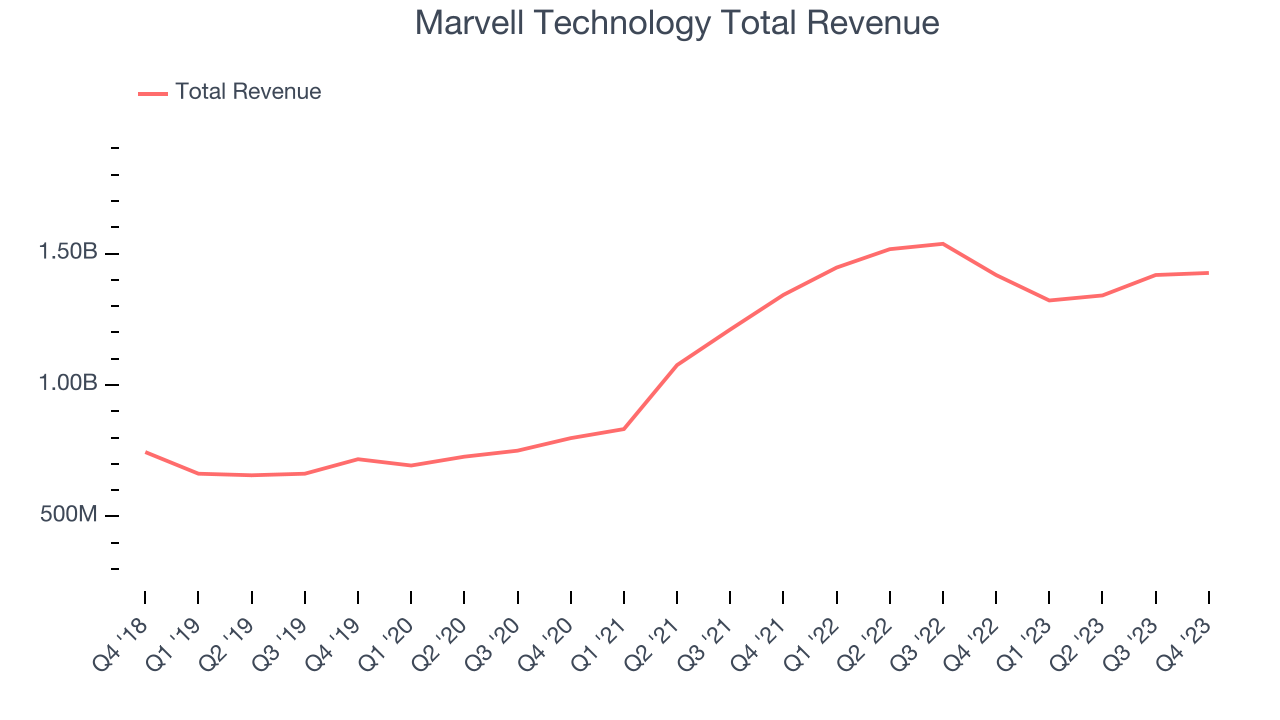

Networking chips designer Marvell Technology (NASDAQ: MRVL) reported results in line with analysts' expectations in Q4 FY2024, with revenue flat year on year at $1.43 billion. On the other hand, next quarter's revenue guidance of $1.15 billion was less impressive, coming in 16% below analysts' estimates. Its non-GAAP profit of $0.46 per share was flat year on year.

Marvell Technology (MRVL) Q4 FY2024 Highlights:

- Revenue: $1.43 billion vs analyst estimates of $1.42 billion (small beat)

- EPS (non-GAAP): $0.46 vs analyst expectations of $0.46 (small miss)

- Revenue Guidance for Q1 2025 is $1.15 billion at the midpoint, below analyst estimates of $1.37 billion

- EPS (non-GAAP) Guidance for Q1 2025 is $0.23 per share at the midpoint, well below analyst estimates of $0.40

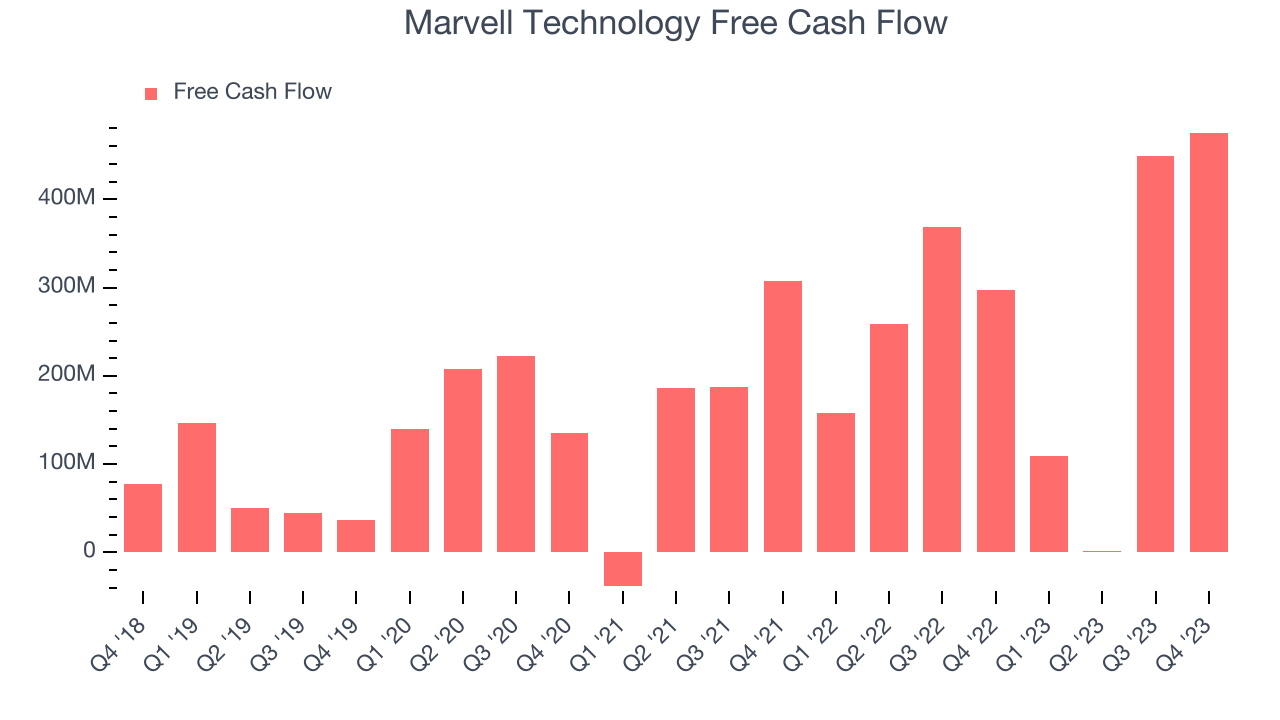

- Free Cash Flow of $475.6 million, similar to the previous quarter

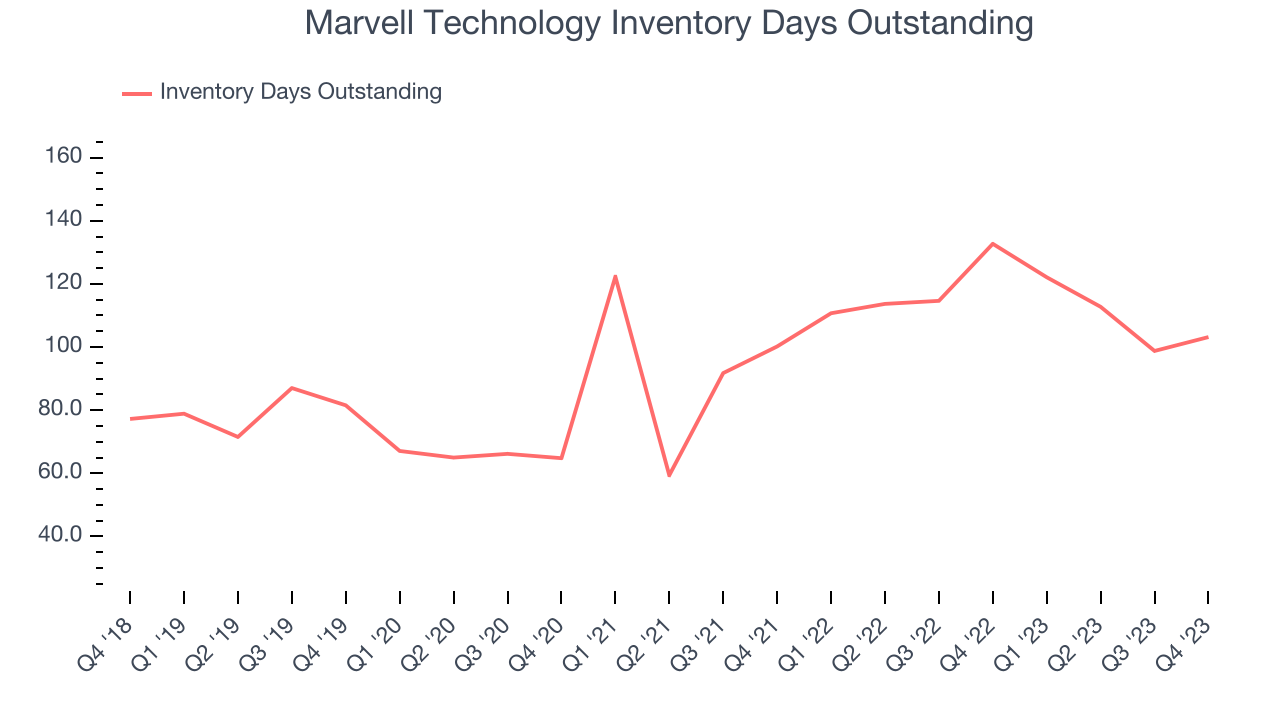

- Inventory Days Outstanding: 103, up from 99 in the previous quarter

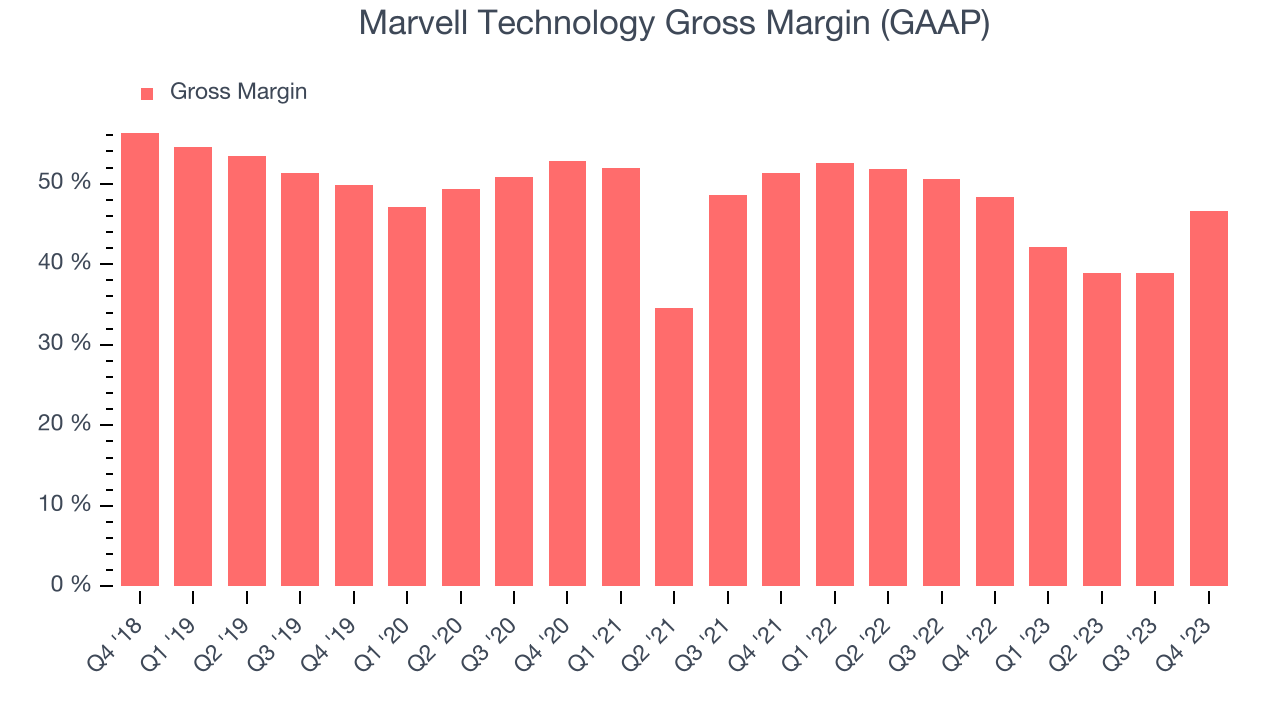

- Gross Margin (GAAP): 46.6%, down from 48.4% in the same quarter last year

- Market Capitalization: $70.34 billion

Moving away from a low margin storage device management chips in one of the biggest semiconductor business model pivots of the past decade, Marvell Technology (NASDAQ: MRVL) is a fabless designer of special purpose data processing and networking chips used by data centers, communications carriers, enterprises, and autos.

Marvell was founded in 1995 by Dr. Sehat Sutardja, his wife, and his brother, and for the first two decades was focused on chips used to run storage devices like disk drives and networking equipment like ethernet switches. It also supplied Wi-Fi chipsets used in mobile devices like the iPhone and Google’s Chromecast. In 2016, in the wake of an internal accounting investigation activist investor Starboard Value acquired a minority stake and ousted Dr. Sutardja and his wife, installing Matt Murphy as CEO.

Murphy quickly exited low margin businesses like the consumer hard drives and Wi-Fi chips and refocused R&D efforts to focus on the higher margin networking business. He made multiple transformative acquisitions: Cavium in 2018, Avera and Aquantia in 2019, and Inphi and Innovium in 2021. The result is a company with leading chipsets that enable data transfer – within and between datacenters, across 5G cellular networks, and throughout autos.

The chips used to power today’s cloud data centers are no longer just general purpose CPUs like we think of that run a PC, but there is also a range of chips that are customized for specific tasks like AI used to scan online videos or machine learning used to make ecommerce recommendations. Marvell specializes in these types of chipsets, known as customized ASICs. Marvell also increasingly competes with chip heavyweights Intel and Nvidia with its Octeon data processing units or “DPUs” which is an ARM-based CPU that offloads networking, storage, security, and other infrastructure workloads from the CPU in the server and accelerates them, saving CPU capacity for other tasks, like running applications.

Marvell’s peers and competitors include AMD (NASDAQ:AMD), Broadcom (NASDAQ:AVGO), Intel (NASDAQ:INTC), and Nvidia (NASDAQ: NDVA).Analog Semiconductors

Longer manufacturing duration allows analog chip makers to generate greater efficiencies, leading to structurally higher gross margins than their fabless digital peers. The downside of vertical integration is that cyclicality can be more pronounced for analog chipmakers, as capacity utilization upsides work in reverse during down periods.

Sales Growth

Marvell Technology's revenue growth over the last three years has been strong, averaging 26.5% annually. But as you can see below, this quarter wasn't particularly strong, with revenue growing from $1.42 billion in the same quarter last year to $1.43 billion. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

This was a sluggish quarter for the company as its revenue dropped 0.6% year on year, in line with analysts' estimates. Marvell Technology's growth, however, flipped from negative to positive this quarter. This encouraging sign will likely be welcomed by shareholders.

Although Marvell Technology returned to positive revenue growth this quarter, its management team expects revenue to decline 13% next quarter. On the other hand, Wall Street expects the favorable trend to continue, projecting 9.7% revenue growth over the next 12 months.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Marvell Technology's DIO came in at 103, which is 10 days above its five-year average, suggesting that the company's inventory has grown to higher levels than we've seen in the past.

Pricing Power

In the semiconductor industry, a company's gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor. Marvell Technology's gross profit margin, which shows how much money the company gets to keep after paying key materials, input, and manufacturing costs, came in at 46.6% in Q4, down 1.8 percentage points year on year.

Marvell Technology's gross margins have been trending down over the last 12 months, averaging 41.6%. This weakness isn't great as Marvell Technology's margins are already far below other semiconductor companies and suggest shrinking pricing power and loose cost controls.

Profitability

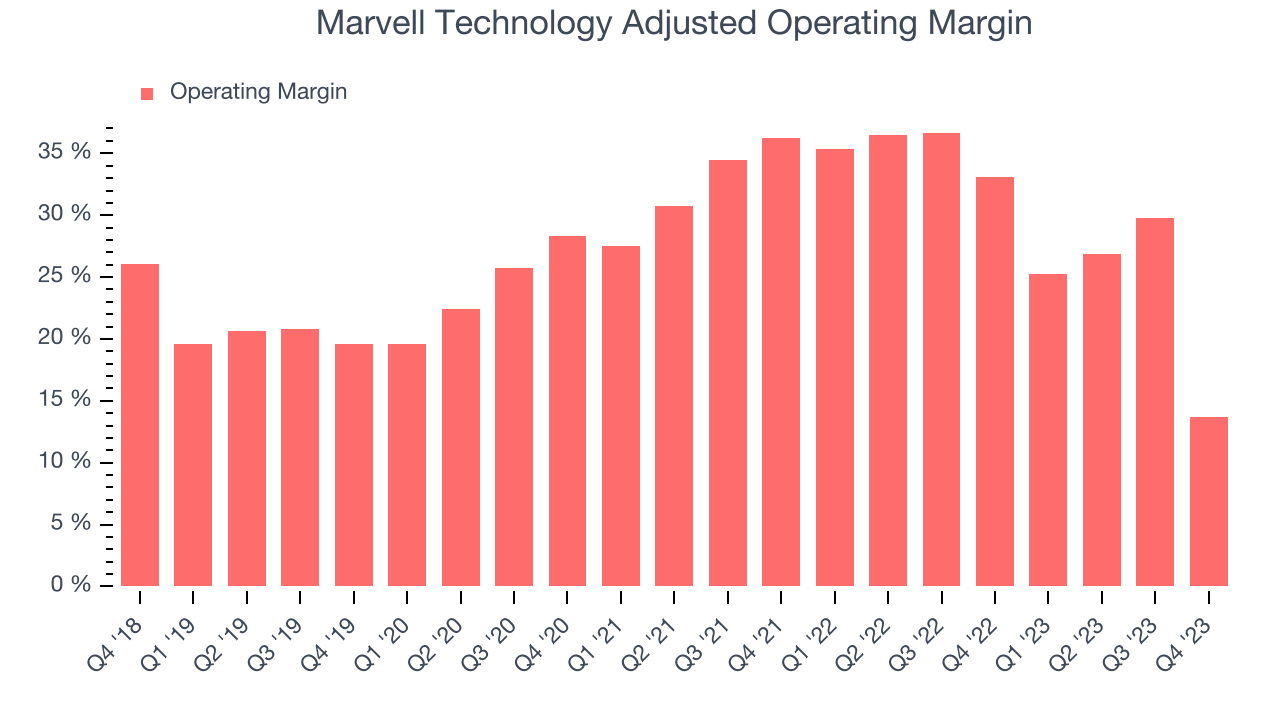

Marvell Technology reported an operating margin of 13.7% in Q4, down 19.4 percentage points year on year. Operating margins are one of the best measures of profitability because they tell us how much money a company takes home after manufacturing its products, marketing and selling them, and, importantly, keeping them relevant through research and development.

Marvell Technology's operating margins have been trending down over the last year, averaging 27.3%. The company's profitability is in line with the broader semiconductor industry and it's working to appropriately manage its operating expenses.

Earnings, Cash & Competitive Moat

Analysts covering Marvell Technology expect earnings per share to grow 32.8% over the next 12 months, although estimates will likely change after earnings.

Although earnings are important, we believe cash is king because you can't use accounting profits to pay the bills. Marvell Technology's free cash flow came in at $475.6 million in Q4, up 59.9% year on year.

As you can see above, Marvell Technology produced $1.03 billion in free cash flow over the last 12 months, a solid 18.8% of revenue. This FCF margin is above average for semiconductor companies and should put Marvell Technology in a relatively strong position to invest in future growth initiatives.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Marvell Technology's five-year average ROIC was negative 0.3%, meaning management lost money while trying to expand the business. Its returns were among the worst in the semiconductor sector.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Marvell Technology's ROIC over the last two years averaged 3.9 percentage point decreases each year. In conjunction with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Marvell Technology's Q4 Results

We struggled to find many strong positives in these results. Both Its revenue and EPS guidance for next quarter missed analysts' expectations and its operating margin shrunk. Overall, the results could have been better. The company is down 11.1% on the results and currently trades at $75.5 per share.

Is Now The Time?

When considering an investment in Marvell Technology, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although we have other favorites, we understand the arguments that Marvell Technology isn't a bad business. We'd expect growth rates to moderate from here, but its revenue growth has been strong over the last three years. And while its relatively low ROIC suggests it has struggled to grow profits historically, the good news is its solid free cash flow generation gives it re-investment options.

Marvell Technology's price-to-earnings ratio based on the next 12 months is 42.5x. There are some things to like about the company, but the state of its balance sheet makes us uncomfortable. We'd like to see the Marvell Technology reduce its leverage before recommending the stock.

Wall Street analysts covering the company had a one-year price target of $75.07 per share right before these results (compared to the current share price of $75.50).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.