Bank software company nCino (NASDAQ:NCNO) announced better-than-expected results in Q2 CY2024, with revenue up 12.9% year on year to $132.4 million. On the other hand, next quarter’s revenue guidance of $137 million was less impressive, coming in 1.2% below analysts’ estimates. It made a non-GAAP profit of $0.14 per share, improving from its loss of $0.14 per share in the same quarter last year.

Is now the time to buy nCino? Find out by accessing our full research report, it’s free.

nCino (NCNO) Q2 CY2024 Highlights:

- Revenue: $132.4 million vs analyst estimates of $131.1 million (1% beat)

- Adjusted Operating Income: $19.3 million vs analyst estimates of $17.93 million (7.6% beat)

- EPS (non-GAAP): $0.14 vs analyst estimates of $0.13 (9.8% beat)

- The company reconfirmed its revenue guidance for the full year of $541.5 million at the midpoint

- Gross Margin (GAAP): 59.3%, in line with the same quarter last year

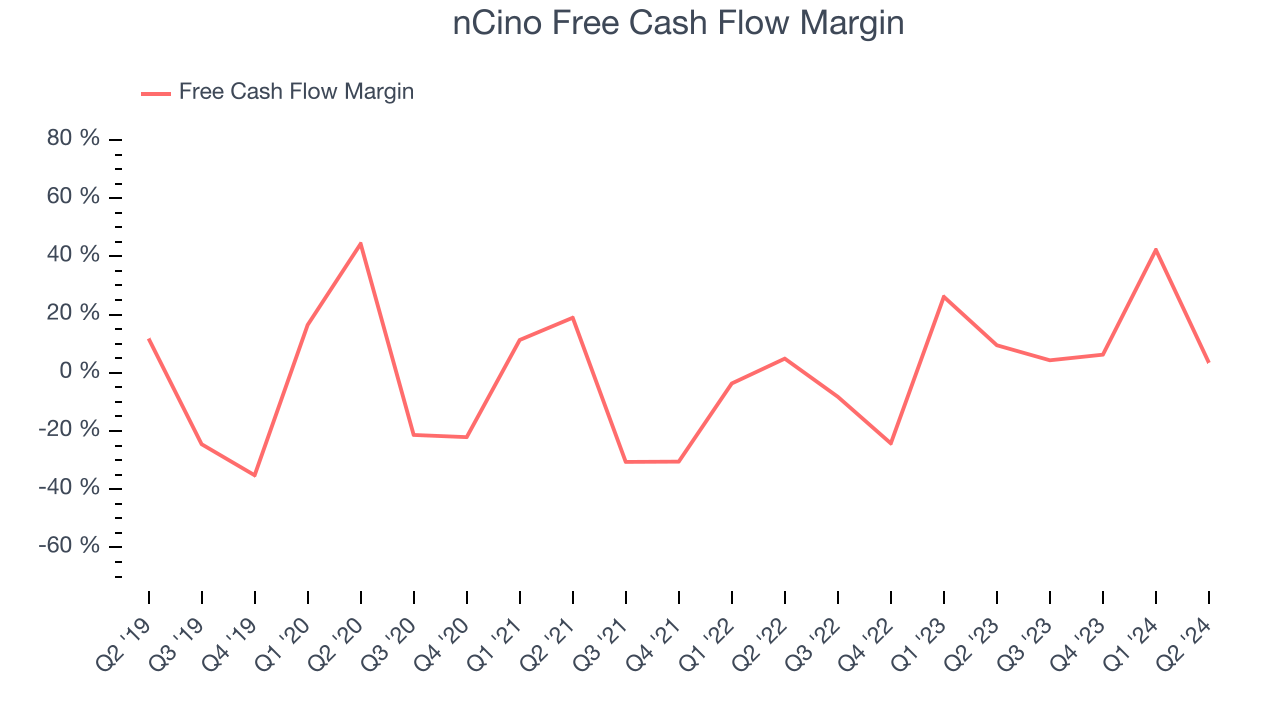

- Free Cash Flow Margin: 3.4%, down from 42.2% in the previous quarter

- Market Capitalization: $3.99 billion

WILMINGTON, N.C., Aug. 27, 2024 (GLOBE NEWSWIRE) -- nCino, Inc. (NASDAQ: NCNO), a pioneer in cloud banking for the global financial services industry, today announced financial results for the second quarter of fiscal year 2025, ended July 31, 2024."We are pleased to report that we again exceeded quarterly guidance for total and subscription revenues as well as non-GAAP operating income," said Pierre Naudé, Chairman and CEO at nCino.

Founded in 2011 in North Carolina, nCino (NASDAQ:NCNO) makes cloud-based operating systems for banks and provides that software-as-a-service.

Banking Software

Consumers these days are accustomed to frictionless digital experiences from online shopping to ordering food or hailing a cab. Financial services firms are notoriously risk averse in adopting modern software, often lacking the resources or competency to develop the digital solutions in-house. That drives demand for software as a service platforms that allows banks and other finance institutions to offer the digital services without having to run or maintain them.

Sales Growth

As you can see below, nCino’s 28.3% annualized revenue growth over the last three years has been impressive, and its sales came in at $132.4 million this quarter.

This quarter, nCino’s quarterly revenue was once again up 12.9% year on year. We can see that nCino’s revenue increased by $4.32 million in Q2, which was roughly the same growth rate observed in Q1 CY2024. This steady quarter-on-quarter growth shows that the company can maintain its paced growth trajectory.

Next quarter’s guidance suggests that nCino is expecting revenue to grow 12.3% year on year to $137 million, slowing down from the 15.8% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 15% over the next 12 months before the earnings results announcement.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

nCino has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14.2% over the last year, better than the broader software sector.

nCino’s free cash flow clocked in at $4.56 million in Q2, equivalent to a 3.4% margin. The company’s cash profitability regressed as it was 6 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict nCino’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 14.2% for the last 12 months will increase to 16.7%, giving it more money to invest.

Key Takeaways from nCino’s Q2 Results

It was encouraging to see nCino narrowly top analysts’ revenue expectations this quarter. On the other hand, its revenue guidance for next quarter missed analysts’ expectations and its gross margin decreased. Overall, this quarter could have been better. The stock traded down 9.4% to $31.25 immediately following the results.

nCino may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.