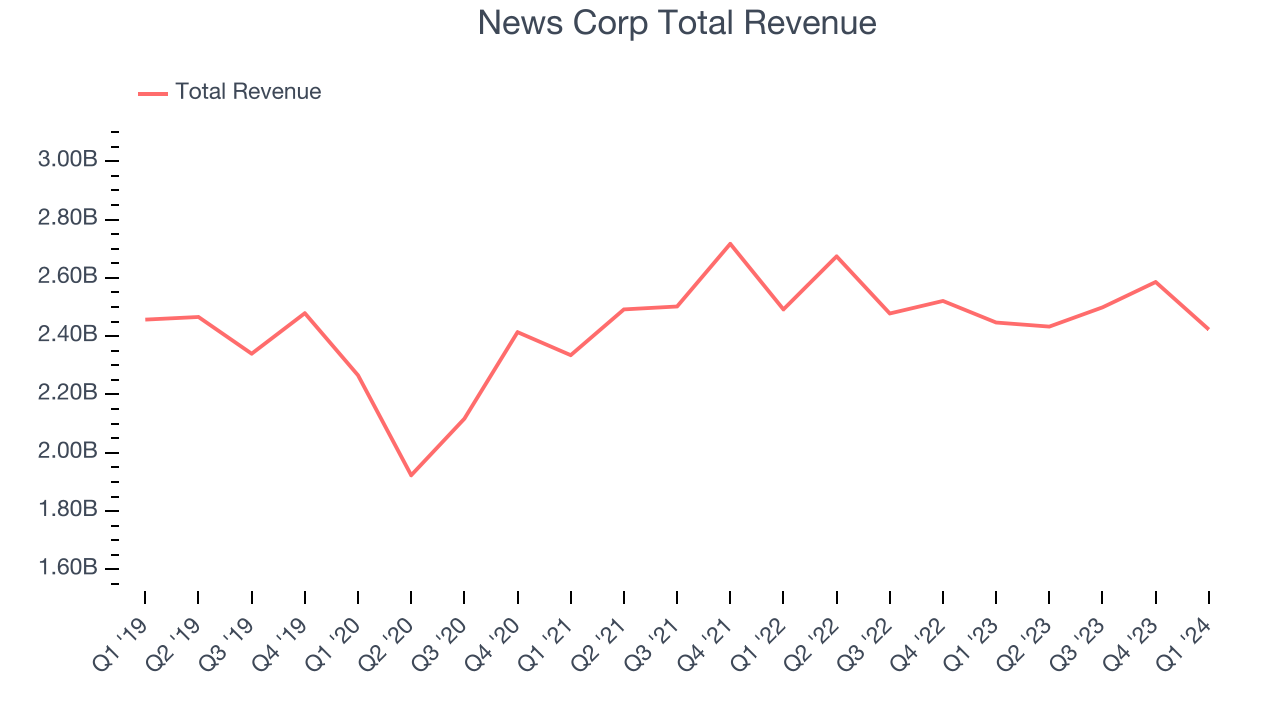

Global media and publishing company News Corp (NASDAQ:NWSA) missed analysts' expectations in Q1 CY2024, with revenue flat year on year at $2.42 billion. It made a GAAP profit of $0.05 per share, down from its profit of $0.09 per share in the same quarter last year.

Is now the time to buy News Corp? Find out by accessing our full research report, it's free.

News Corp (NWSA) Q1 CY2024 Highlights:

- Revenue: $2.42 billion vs analyst estimates of $2.45 billion (1% miss)

- EPS: $0.05 vs analyst expectations of $0.08 (41.1% miss)

- Gross Margin (GAAP): 48.9%, up from 47.4% in the same quarter last year

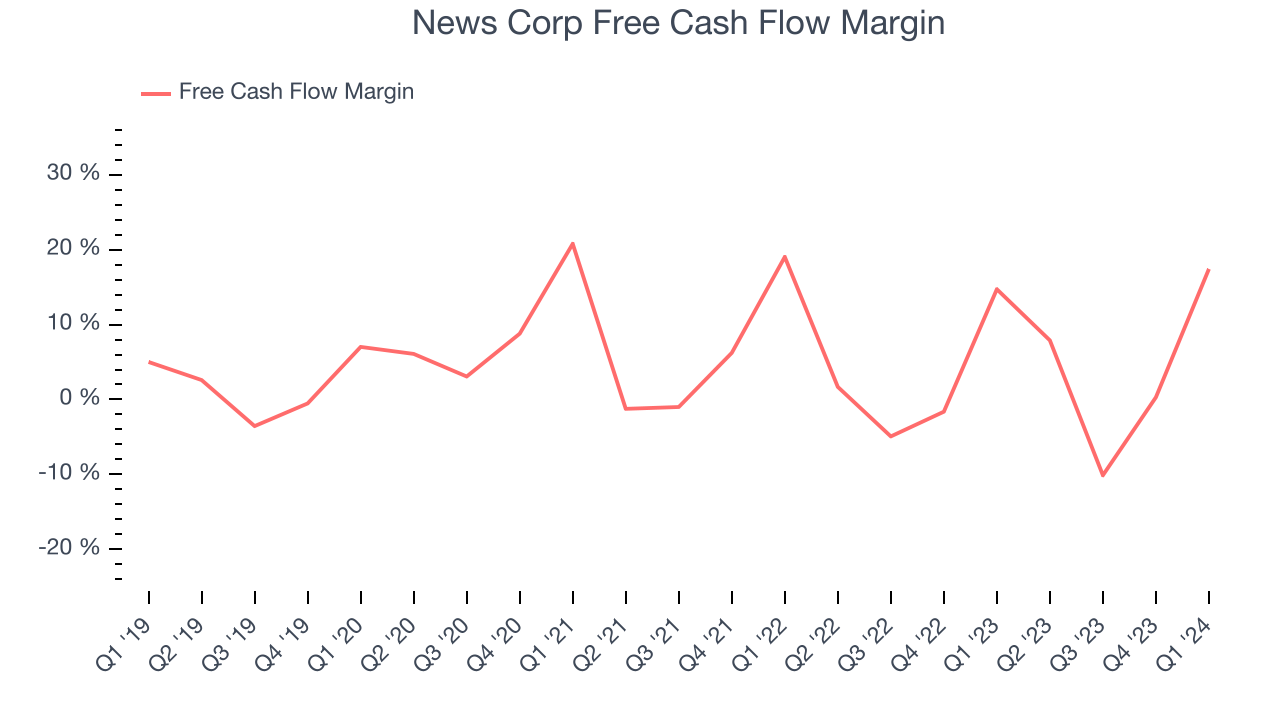

- Free Cash Flow of $422 million, up from $7.71 million in the previous quarter

- Market Capitalization: $14.08 billion

Established in 2013 after a restructuring, News Corp (NASDAQ:NWSA) is a multinational conglomerate known for its news publishing, broadcasting, digital media, and book publishing.

Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. News Corp's revenue was flat over the last five years.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. News Corp's recent history shows a reversal from its five-year trend as its revenue has shown annualized declines of 1.3% over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. News Corp's recent history shows a reversal from its five-year trend as its revenue has shown annualized declines of 1.3% over the last two years.

We can better understand the company's revenue dynamics by analyzing its three most important segments: Dow Jones, News Media, and Book Publishing, which are 22.5%, 21.9%, and 20.9% of revenue. Over the last two years, News Corp's Dow Jones revenue (media subsidiary) averaged 8.6% year-on-year growth while its News Media (general media) and Book Publishing (general publishing) revenues averaged declines of 3.7% and 3%.

This quarter, News Corp missed Wall Street's estimates and reported a rather uninspiring 1% year-on-year revenue decline, generating $2.42 billion of revenue. Looking ahead, Wall Street expects sales to grow 3.4% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, News Corp has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 3%, subpar for a consumer discretionary business.

News Corp's free cash flow came in at $422 million in Q1, equivalent to a 17.4% margin and up 17.2% year on year.

Key Takeaways from News Corp's Q1 Results

We struggled to find many strong positives in these results. Its EPS missed and its News Media revenue fell short of Wall Street's estimates. Overall, this was a bad quarter for News Corp. The company is down 1.2% on the results and currently trades at $23.85 per share.

News Corp may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.