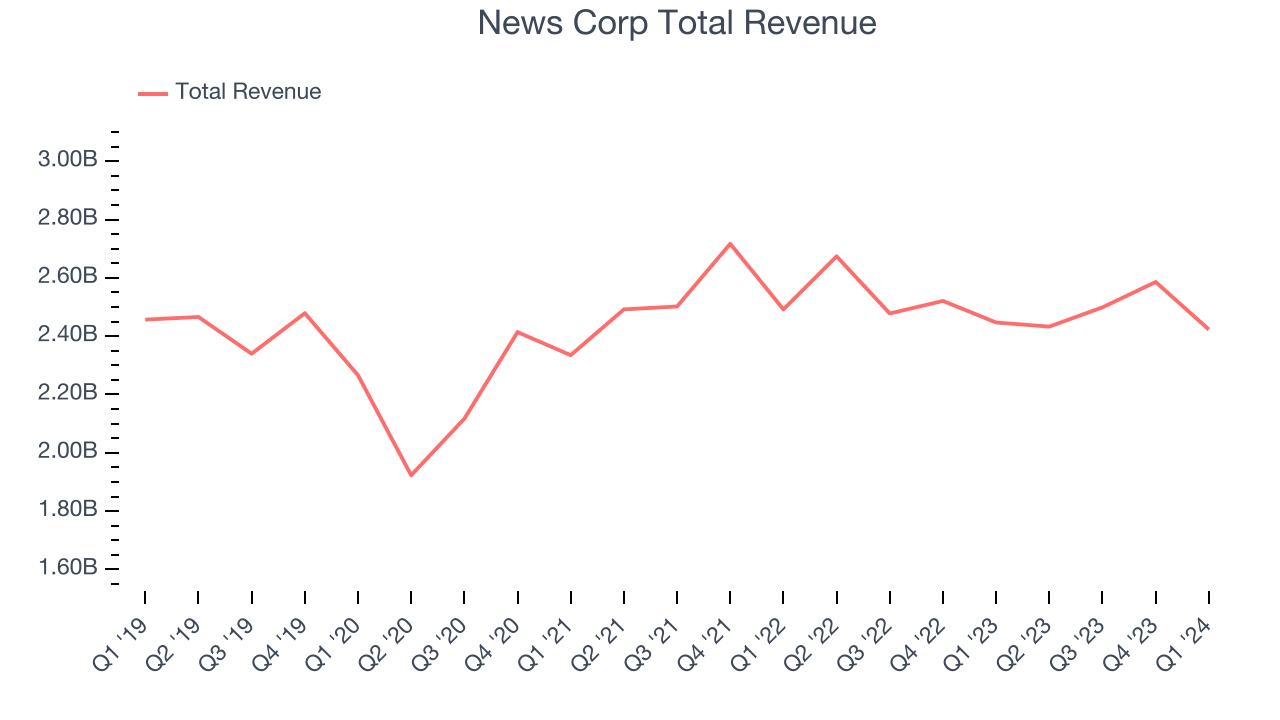

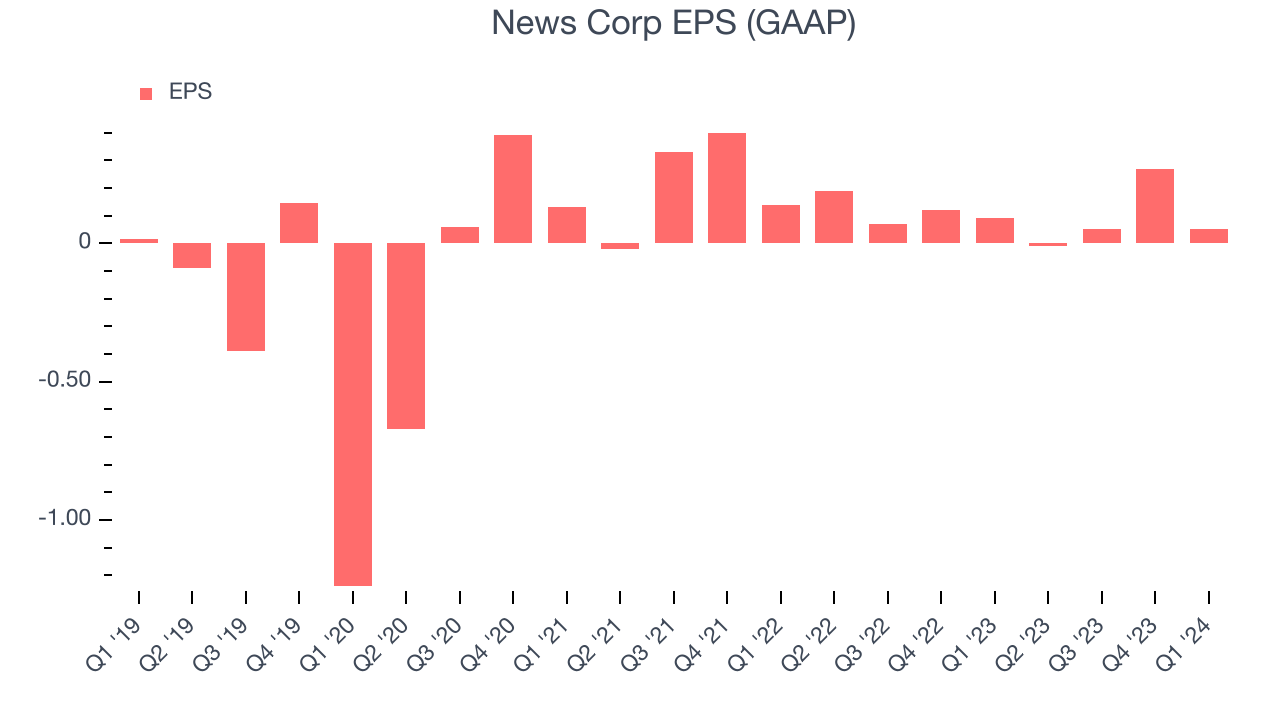

Global media and publishing company News Corp (NASDAQ:NWSA) missed analysts' expectations in Q1 CY2024, with revenue flat year on year at $2.42 billion. It made a GAAP profit of $0.05 per share, down from its profit of $0.09 per share in the same quarter last year.

News Corp (NWSA) Q1 CY2024 Highlights:

- Revenue: $2.42 billion vs analyst estimates of $2.45 billion (1% miss)

- EPS: $0.05 vs analyst expectations of $0.08 (41.1% miss)

- Gross Margin (GAAP): 48.9%, up from 47.4% in the same quarter last year

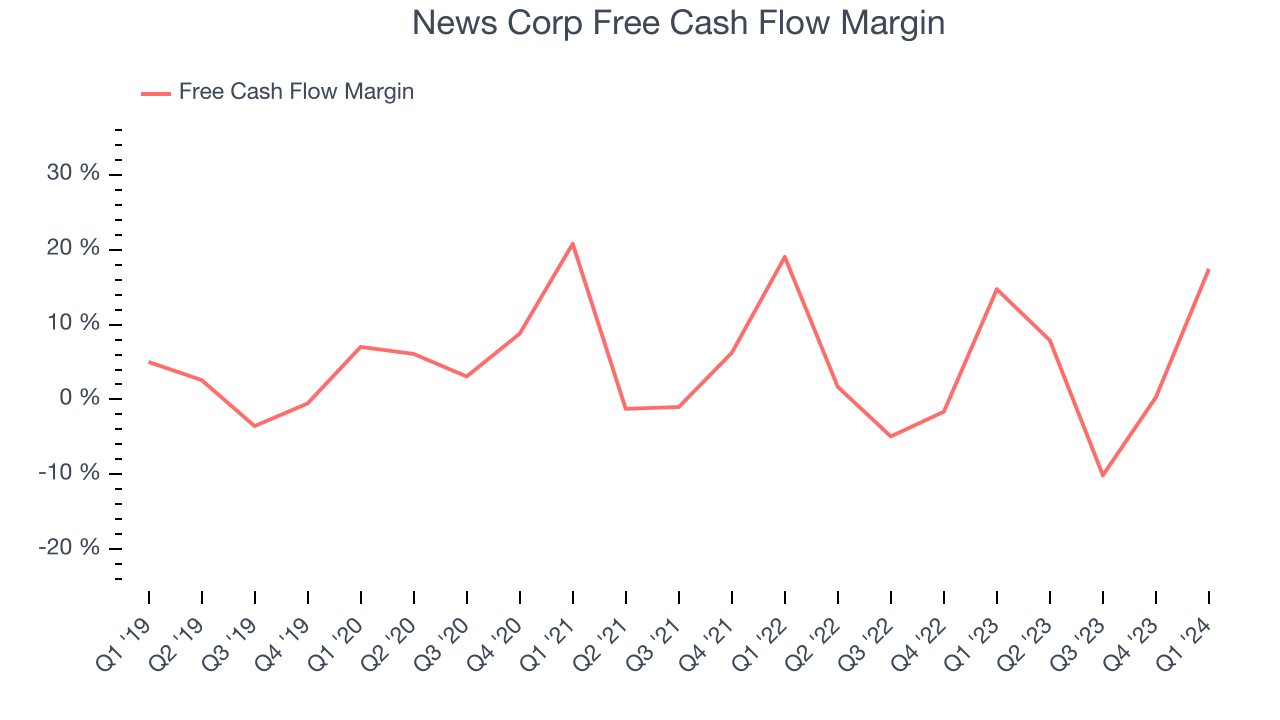

- Free Cash Flow of $422 million, up from $7.71 million in the previous quarter

- Market Capitalization: $14.08 billion

Established in 2013 after a restructuring, News Corp (NASDAQ:NWSA) is a multinational conglomerate known for its news publishing, broadcasting, digital media, and book publishing.

News Corp was created to focus on delivering news and media services in the digital age. At its core, it seeks to address the need for reliable news, diverse entertainment, and educational content.

The company's portfolio spans well-known news outlets such as The Wall Street Journal, TV stations, digital media platforms, and publishing houses. This wide range of perspectives and formats caters to diverse consumer preferences for both traditional and digital media.

News Corp generates revenue through advertising, licensing fees, and subscription fees. Some of its content can also be purchased on a one-off basis.

Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Competitors in the news publishing and media sector include The New York Times (NYSE:NYT), Gannett (NYSE:GCI), and The E.W. Scripps (NASDAQ:SSP).Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. News Corp's revenue was flat over the last five years.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. News Corp's recent history shows a reversal from its five-year trend as its revenue has shown annualized declines of 1.3% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. News Corp's recent history shows a reversal from its five-year trend as its revenue has shown annualized declines of 1.3% over the last two years.

We can dig even further into the company's revenue dynamics by analyzing its three most important segments: Dow Jones, News Media, and Book Publishing, which are 22.5%, 21.9%, and 20.9% of revenue. Over the last two years, News Corp's Dow Jones revenue (media subsidiary) averaged 8.6% year-on-year growth while its News Media (general media) and Book Publishing (general publishing) revenues averaged declines of 3.7% and 3%.

This quarter, News Corp missed Wall Street's estimates and reported a rather uninspiring 1% year-on-year revenue decline, generating $2.42 billion of revenue. Looking ahead, Wall Street expects sales to grow 3.4% over the next 12 months, an acceleration from this quarter.

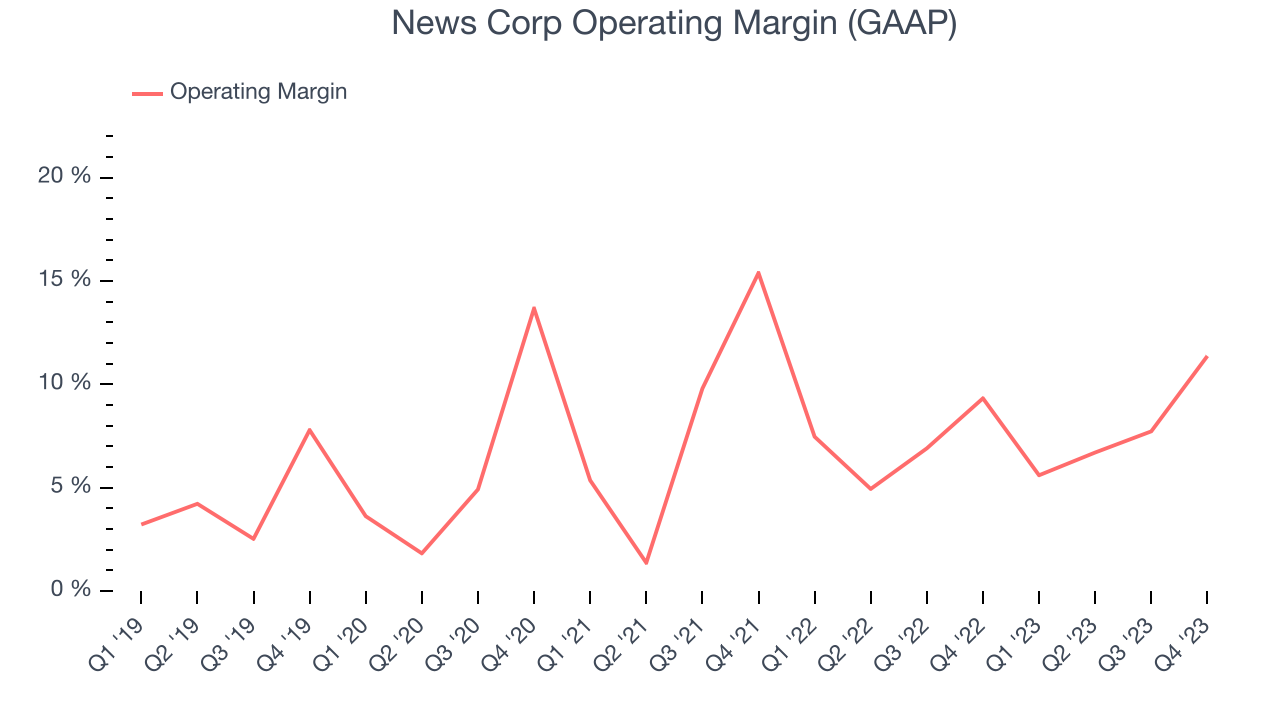

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

News Corp was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer discretionary business, producing an average operating margin of 7.5%.

in line with the same quarter last year. This indicates the company's costs have been relatively stable.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, News Corp cut its earnings losses and improved its EPS by 26.5% each year. This performance is materially higher than its flat revenue over the same period. There are a few reasons for this, and understanding why can shed light on its fundamentals.

A five-year view shows that News Corp has repurchased its stock, shrinking its share count by 2.5%. This has led to higher per share earnings. Taxes and interest expenses can also affect EPS growth, but they don't tell us as much about a company's fundamentals.In Q1, News Corp reported EPS at $0.05, down from $0.09 in the same quarter last year. This print unfortunately missed analysts' estimates, but we care more about long-term EPS growth rather than short-term movements. Over the next 12 months, Wall Street expects News Corp to grow its earnings. Analysts are projecting its LTM EPS of $0.36 to climb by 101% to $0.73.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, News Corp has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 3%, subpar for a consumer discretionary business.

News Corp's free cash flow came in at $422 million in Q1, equivalent to a 17.4% margin and up 17.2% year on year.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

News Corp's five-year average return on invested capital was 6.8%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, News Corp's ROIC averaged 2.8 percentage point increases. This is a good sign, and we hope the company can continue improving.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

News Corp reported $1.94 billion of cash and $3.95 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $1.51 billion of EBITDA over the last 12 months, we view News Corp's 1.3x net-debt-to-EBITDA ratio as safe. We also see its $86 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from News Corp's Q1 Results

We struggled to find many strong positives in these results. Its EPS missed and its News Media revenue fell short of Wall Street's estimates. Overall, this was a bad quarter for News Corp. The company is down 1.2% on the results and currently trades at $23.85 per share.

Is Now The Time?

News Corp may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of News Corp, we'll be cheering from the sidelines. Its revenue has declined over the last five years, but at least growth is expected to increase in the short term. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its relatively low ROIC suggests it has historically struggled to find compelling business opportunities. On top of that, its low free cash flow margins give it little breathing room.

While there are some things to like about News Corp and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $22 per share right before these results (compared to the current share price of $23.85).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.