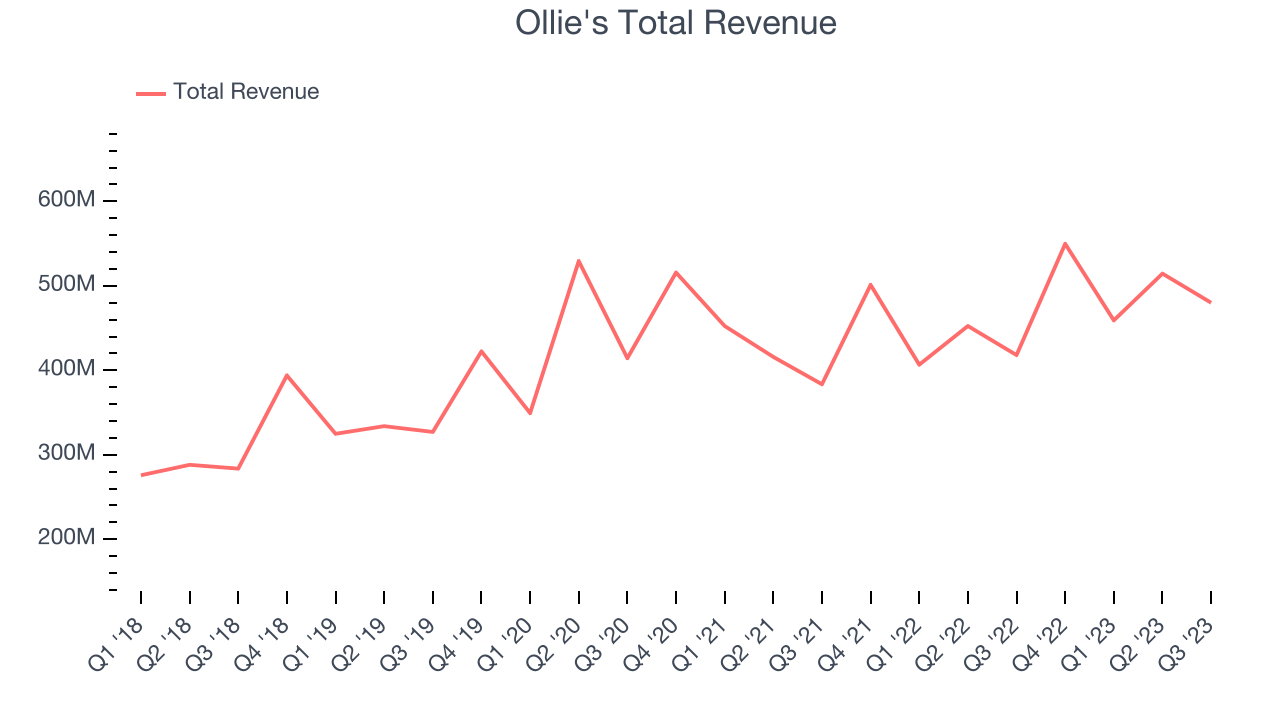

Discount retail company Ollie’s Bargain Outlet (NASDAQ:OLLI) reported Q3 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 14.8% year on year to $480.1 million. The company's full-year revenue guidance of $2.10 billion at the midpoint also came in slightly above analysts' estimates. It made a non-GAAP profit of $0.51 per share, improving from its profit of $0.37 per share in the same quarter last year.

Is now the time to buy Ollie's? Find out by accessing our full research report, it's free.

Ollie's (OLLI) Q3 FY2023 Highlights:

- Revenue: $480.1 million vs analyst estimates of $469.3 million (2.3% beat)

- EPS (non-GAAP): $0.51 vs analyst estimates of $0.45 (13.7% beat)

- The company reconfirmed its revenue guidance for the full year of $2.10 billion at the midpoint

- Gross Margin (GAAP): 40.4%, up from 39.4% in the same quarter last year

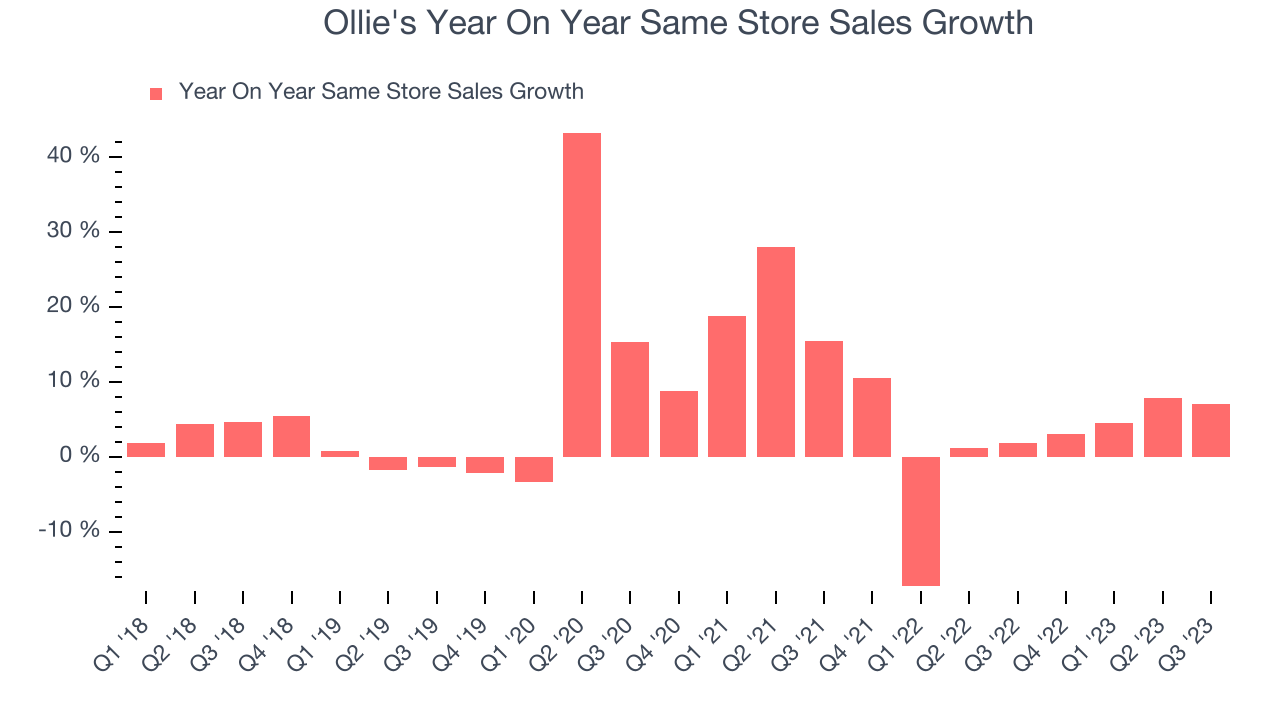

- Same-Store Sales were up 7% year on year

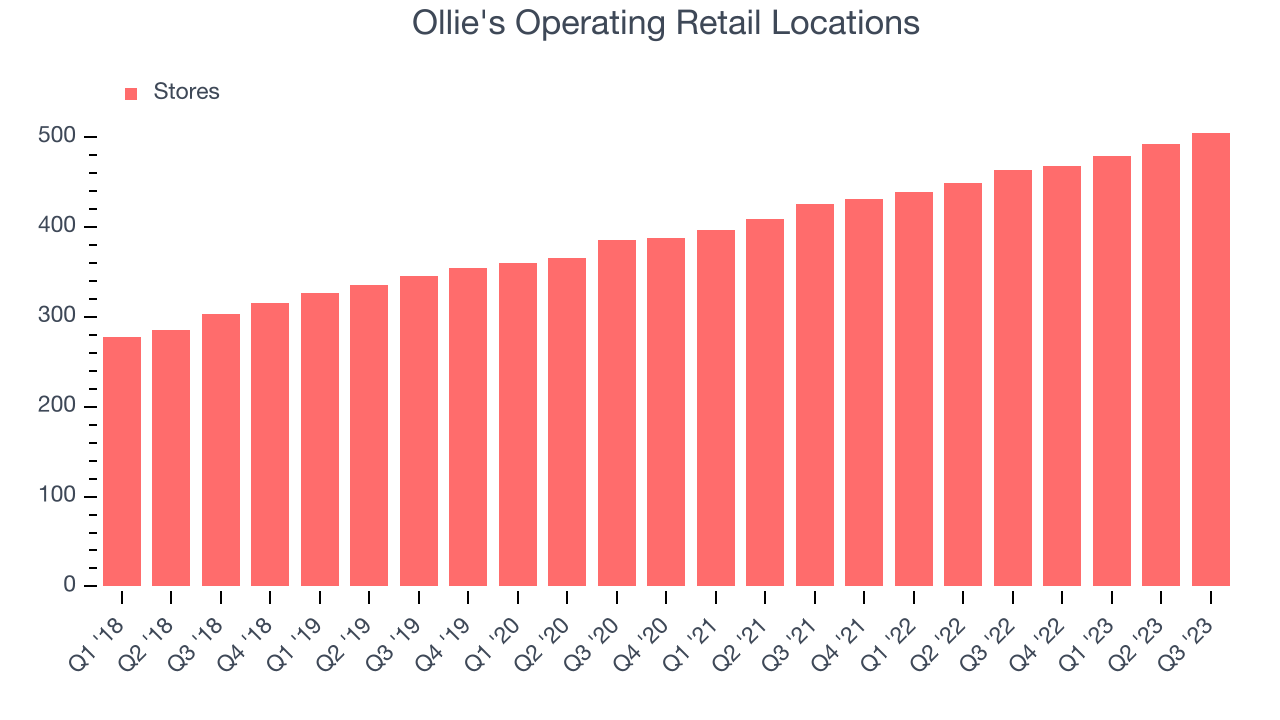

- Store Locations: 505 at quarter end, increasing by 42 over the last 12 months

“We had another strong quarter and are pleased with the positive trends in our business. Our third quarter sales and margins came in ahead of our expectations, driven by strong deal flow, lower supply chain costs, and continued execution throughout the organization. In the quarter, comparable store sales increased 7.0%, net sales increased 14.8% to $480 million, and adjusted EBITDA increased 29.5% to $51 million. We also opened a record 23 new stores in the quarter and saw very healthy new store productivity in the period,” said John Swygert, President and Chief Executive Officer.

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ:OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

Discount General Merchandise Retailer

Broadline discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Sales Growth

Ollie's is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 9.8% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new stores and grew sales at existing, established stores.

This quarter, Ollie's reported robust year-on-year revenue growth of 14.8%, and its $480.1 million in revenue exceeded Wall Street's estimates by 2.3%. Looking ahead, analysts expect sales to grow 12.6% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

When a retailer like Ollie's is opening new stores, it usually means it's investing for growth because demand is greater than supply. Ollie's store count increased by 42 locations, or 9.1%, over the last 12 months to 505 total retail locations in the most recently reported quarter.

Taking a step back, the company has rapidly opened new stores over the last eight quarters, averaging 9.6% annual growth in its physical footprint. This store growth is much higher than other retailers and gives Ollie's a chance to scale towards a mid-sized company over time. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Ollie's demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company's same-store sales have grown by 2.3% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Ollie's is reaching more customers and growing sales.

In the latest quarter, Ollie's same-store sales rose 7% year on year. This growth was an acceleration from the 1.9% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Ollie's Q3 Results

With a market capitalization of $4.70 billion, Ollie's is among smaller companies, but its $264 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

We enjoyed seeing Ollie's raise its revenue guidance for next quarter and exceed analysts' revenue expectations this quarter, driven by robust same-store sales growth (7% vs expectations of 3.5%). We were also excited its adjusted EBITDA and EPS outperformed Wall Street's estimates. Management noted that "consumers remain under pressure and are looking for ways to save money on [the] branded merchandise they need and want in their homes". Overall, we think this was a strong quarter that should satisfy shareholders. The stock is up 3.6% after reporting and currently trades at $79.07 per share.

So should you invest in Ollie's right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.