Technology real estate company Opendoor (NASDAQ:OPEN) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue down 62.1% year on year to $1.18 billion. On the other hand, next quarter's revenue guidance of $1.45 billion was less impressive, coming in 3.1% below analysts' estimates. It made a GAAP loss of $0.16 per share, improving from its loss of $0.16 per share in the same quarter last year.

Opendoor (OPEN) Q1 CY2024 Highlights:

- Revenue: $1.18 billion vs analyst estimates of $1.09 billion (8.8% beat)

- Adjusted EBITDA: ($50) million vs analyst estimates of ($72) million (beat)

- EPS: -$0.16 vs analyst estimates of -$0.21 (24.4% beat)

- Revenue Guidance for Q2 CY2024 is $1.45 billion at the midpoint, below analyst estimates of $1.50 billion

- Adjusted EBITDA Guidance for Q2 CY2024 is ($30) million at the midpoint, better than analyst estimates of ($47) million

- Gross Margin (GAAP): 9.7%, up from 5.4% in the same quarter last year

- Free Cash Flow was -$186 million compared to -$551 million in the previous quarter

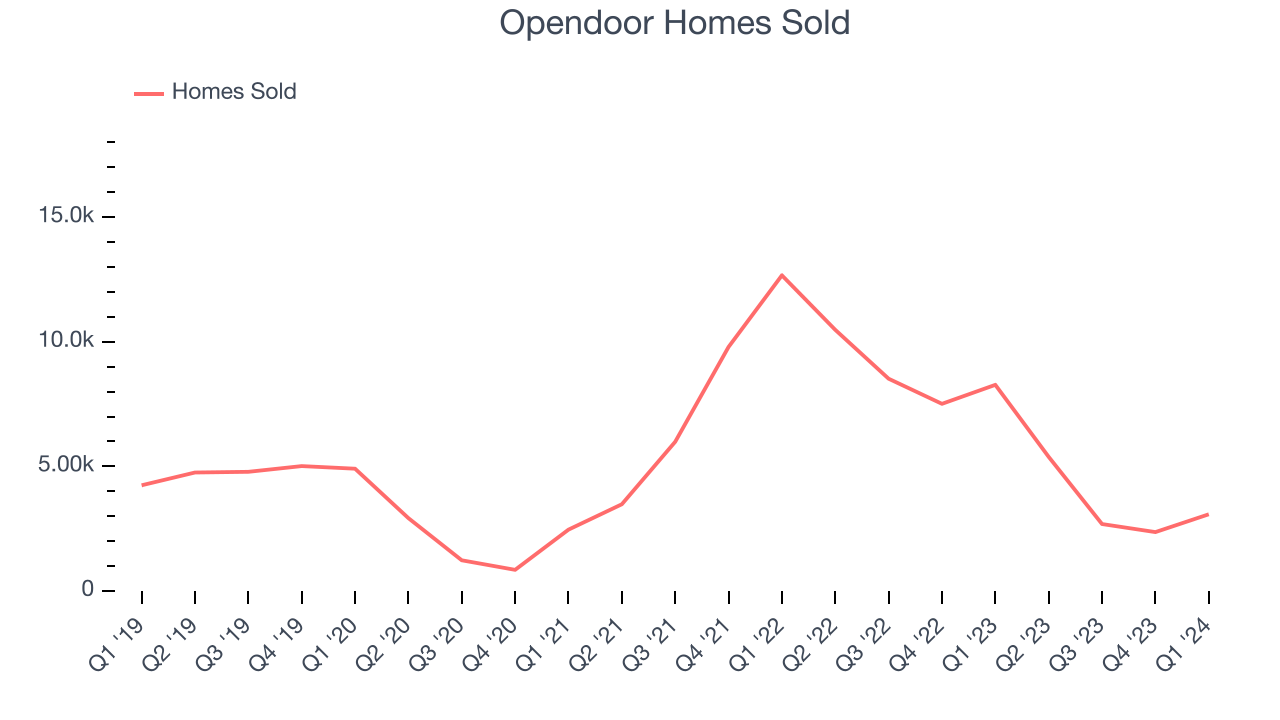

- Homes Sold: 3,078

- Market Capitalization: $1.38 billion

Founded by real estate guru Eric Wu, Opendoor (NASDAQ:OPEN) offers a technology-driven, convenient, and streamlined process to buy and sell homes.

Opendoor's core business is its iBuying service, allowing homeowners to quickly sell their homes directly to Opendoor at a competitive price, bypassing the traditional real estate market's complexities and uncertainties. Homeowners can request an offer online, receive a data-driven valuation, and, if they accept, sell their home to Opendoor in a matter of days. This model has been appealing for its speed, convenience, and certainty.

After purchasing homes, Opendoor makes necessary renovations, lists the properties for sale, and provides a streamlined buying experience for new homeowners. The company’s digital platform enables buyers to browse listings, schedule tours, and purchase homes directly online, further simplifying the home-buying process.

The company leverages data analytics, machine learning algorithms, and market insights to value homes and streamline operations. This technology-first approach allows Opendoor to efficiently manage a large inventory of homes.

In addition to buying and selling homes, Opendoor provides ancillary services that complement its primary business. These include Opendoor Home Loans for financing, Opendoor-backed home warranties, and other services aimed at simplifying the transaction process.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Opendoor's primary competitors include Zillow (NASDAQ:ZG), Redfin (NASDAQ:RDFN), Offerpad Solutions (NYSE:OPAD), and eXp World (NASDAQ:EXPI).Sales Growth

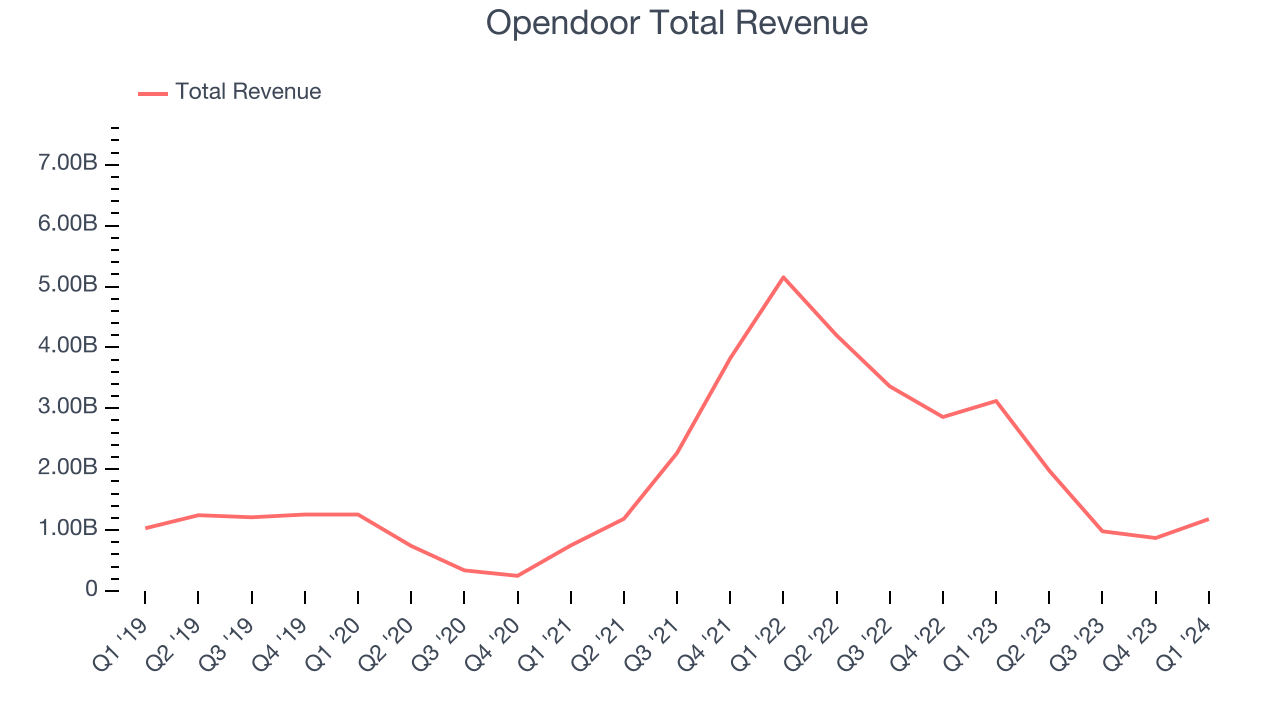

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Opendoor's annualized revenue growth rate of 14.8% over the last five years was mediocre for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Opendoor's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 36.5% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Opendoor's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 36.5% over the last two years.

We can dig even further into the company's revenue dynamics by analyzing its number of homes sold, which reached 3,078 in the latest quarter. Over the last two years, Opendoor's homes sold averaged 7.9% year-on-year declines. Because this number is higher than its revenue growth during the same period, we can see the company's monetization of its consumers has fallen.

This quarter, Opendoor's revenue fell 62.1% year on year to $1.18 billion but beat Wall Street's estimates by 8.8%. The company is guiding for a 26.6% year-on-year revenue decline next quarter to $1.45 billion, an improvement from the 52.9% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 30.2% over the next 12 months, an acceleration from this quarter.

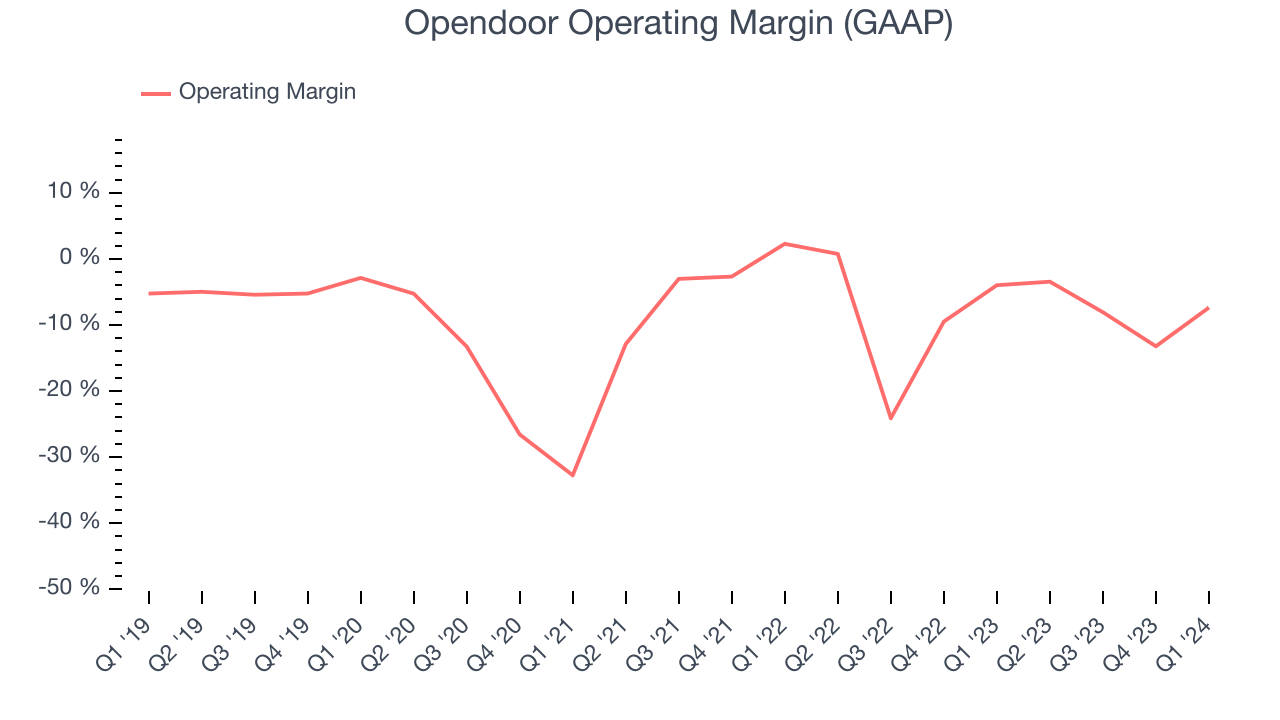

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Given the consumer discretionary industry's volatile demand characteristics, unprofitable companies should be scrutinized. Over the last two years, Opendoor's high expenses have contributed to an average operating margin of negative 8.2%.

This quarter, Opendoor generated an operating profit margin of negative 7.4%, down 3.4 percentage points year on year.

Over the next 12 months, Wall Street expects Opendoor to shrink its losses but remain unprofitable. Analysts are expecting the company’s LTM operating margin of negative 7% to rise to negative 5.6%.EPS

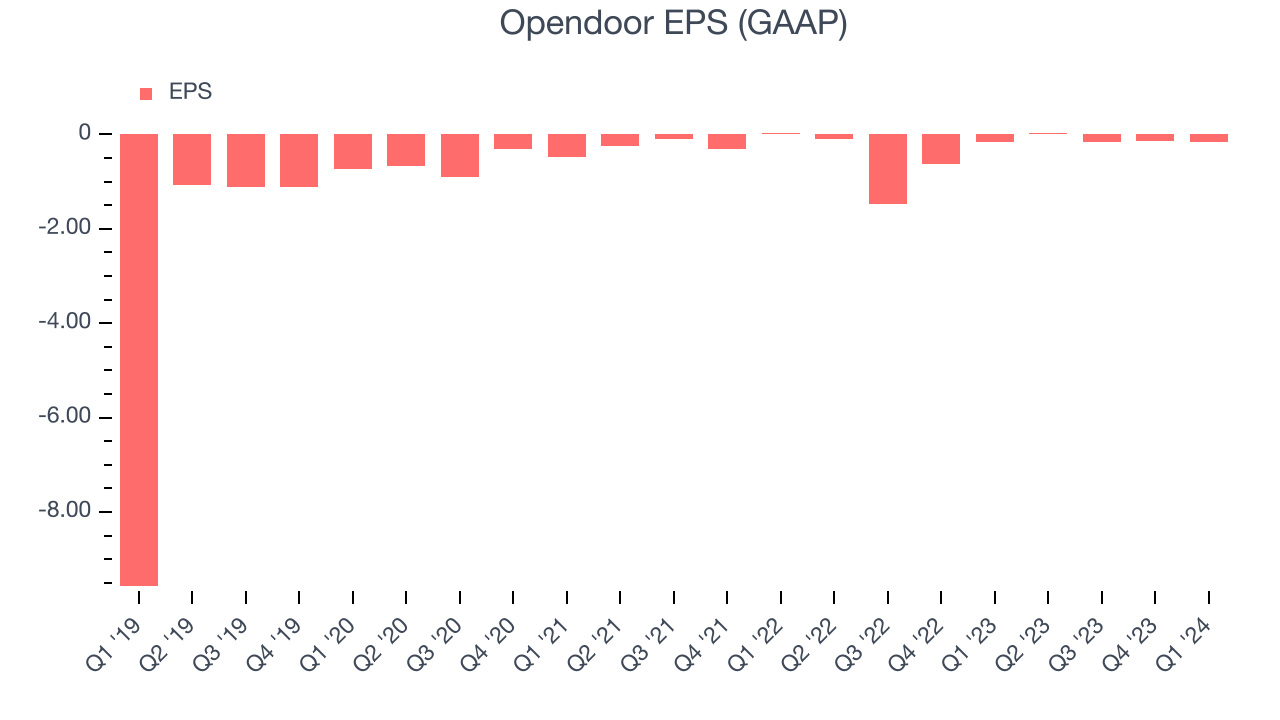

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, Opendoor cut its earnings losses and improved its EPS by 48.7% each year.

In Q1, Opendoor reported EPS at negative $0.16, up from negative $0.16 in the same quarter last year. This print beat analysts' estimates by 24.4%. Over the next 12 months, Wall Street expects Opendoor to perform poorly. Analysts are projecting its LTM EPS of negative $0.43 to tumble to negative $0.72.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

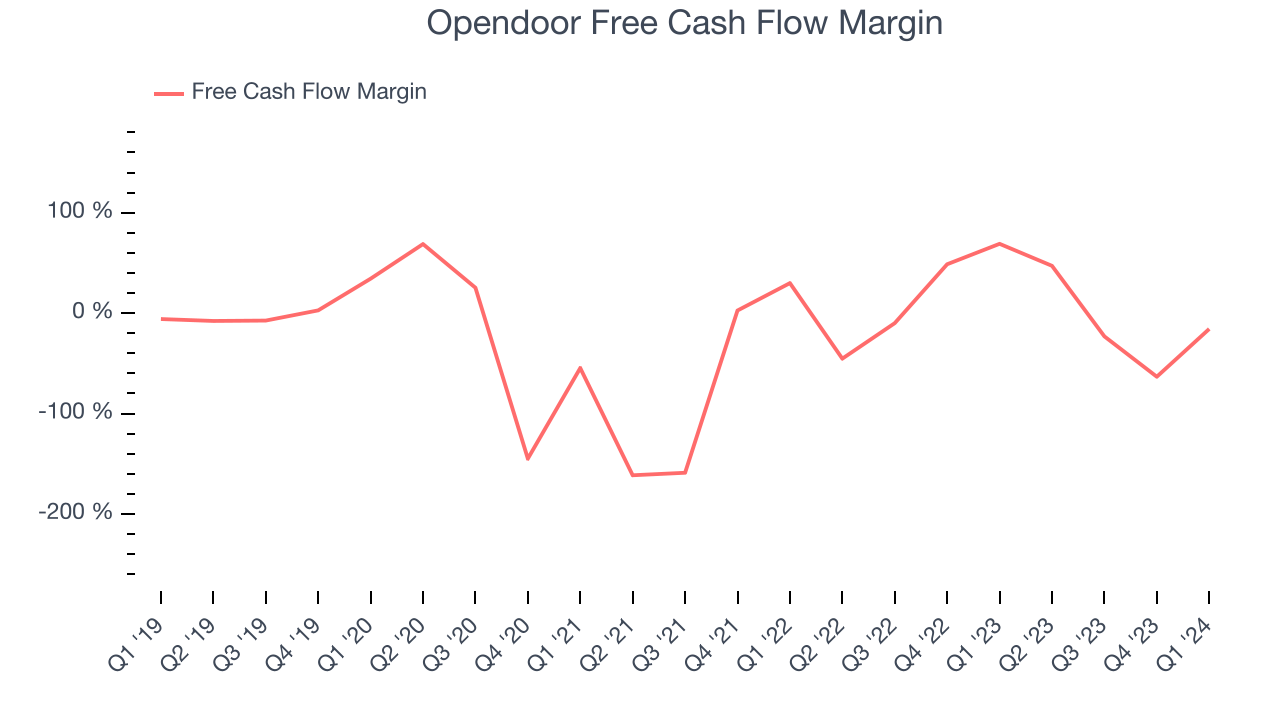

Over the last two years, Opendoor has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 6.9%, subpar for a consumer discretionary business.

Opendoor burned through $186 million of cash in Q1, equivalent to a negative 15.7% margin. This caught our eye as the company shifted from cash flow positive in the same quarter last year to cash flow negative this quarter.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Opendoor, which has $990 million of cash and $2.06 billion of debt on its balance sheet, was unprofitable over the last 12 months. It posted negative $336 million of EBITDA, and as investors in high-quality companies, we seek to avoid indebted loss-making companies.

We implore our readers to do the same because credit agencies could downgrade Opendoor if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Opendoor can improve its profitability and remain cautious until then.

Key Takeaways from Opendoor's Q1 Results

We liked how Opendoor beat analysts' revenue and adjusted EBITDA expectations this quarter, with the latter beating by a convincing amount. While its revenue guidance for next quarter was underwhelming, adjusted EBITDA guidance for the period was well above. Overall, we think this was a really good quarter that should please shareholders. The stock is up 11.4% after reporting and currently trades at $2.25 per share.

Is Now The Time?

Opendoor may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Opendoor, we'll be cheering from the sidelines. Its revenue growth has been mediocre over the last five years, but at least growth is expected to increase in the short term. And while its EPS growth over the last five years has been fantastic, the downside is its number of homes sold has been disappointing. On top of that, its projected EPS for the next year is lacking.

While we've no doubt one can find things to like about Opendoor, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $3.03 per share right before these results (compared to the current share price of $2.25).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.