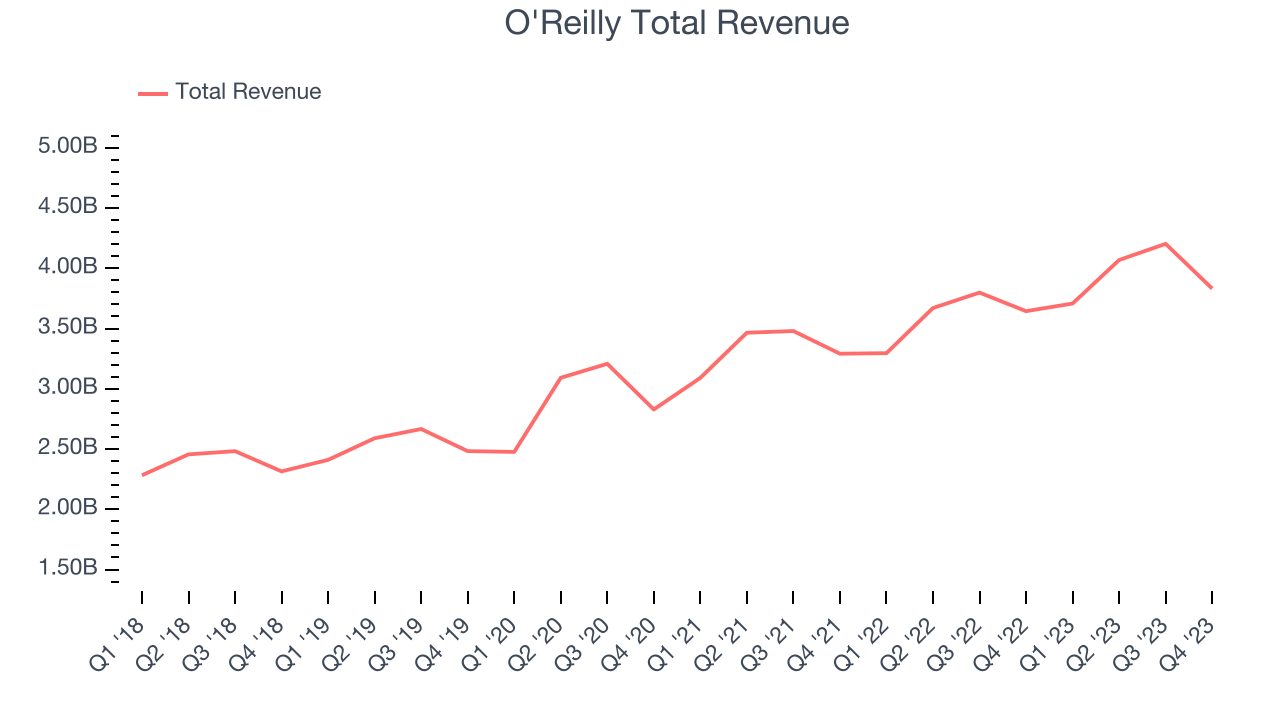

Auto parts and accessories retailer O’Reilly Automotive (NASDAQ:ORLY) fell short of analysts' expectations in Q4 FY2023, with revenue up 5.1% year on year to $3.83 billion. On the other hand, the company's full-year revenue guidance of $16.95 billion at the midpoint came in slightly above analysts' estimates. It made a GAAP profit of $9.26 per share, improving from its profit of $8.36 per share in the same quarter last year.

Is now the time to buy O'Reilly? Find out by accessing our full research report, it's free.

O'Reilly (ORLY) Q4 FY2023 Highlights:

- Revenue: $3.83 billion vs analyst estimates of $3.86 billion (0.8% miss)

- EPS: $9.26 vs analyst estimates of $9.21 (small beat)

- Management's revenue guidance for the upcoming financial year 2024 is $16.95 billion at the midpoint, beating analyst estimates by 0.9% and implying 7.2% growth (vs 9.8% in FY2023)

- Free Cash Flow of $256 million, down 40% from the same quarter last year

- Gross Margin (GAAP): 51.3%, in line with the same quarter last year

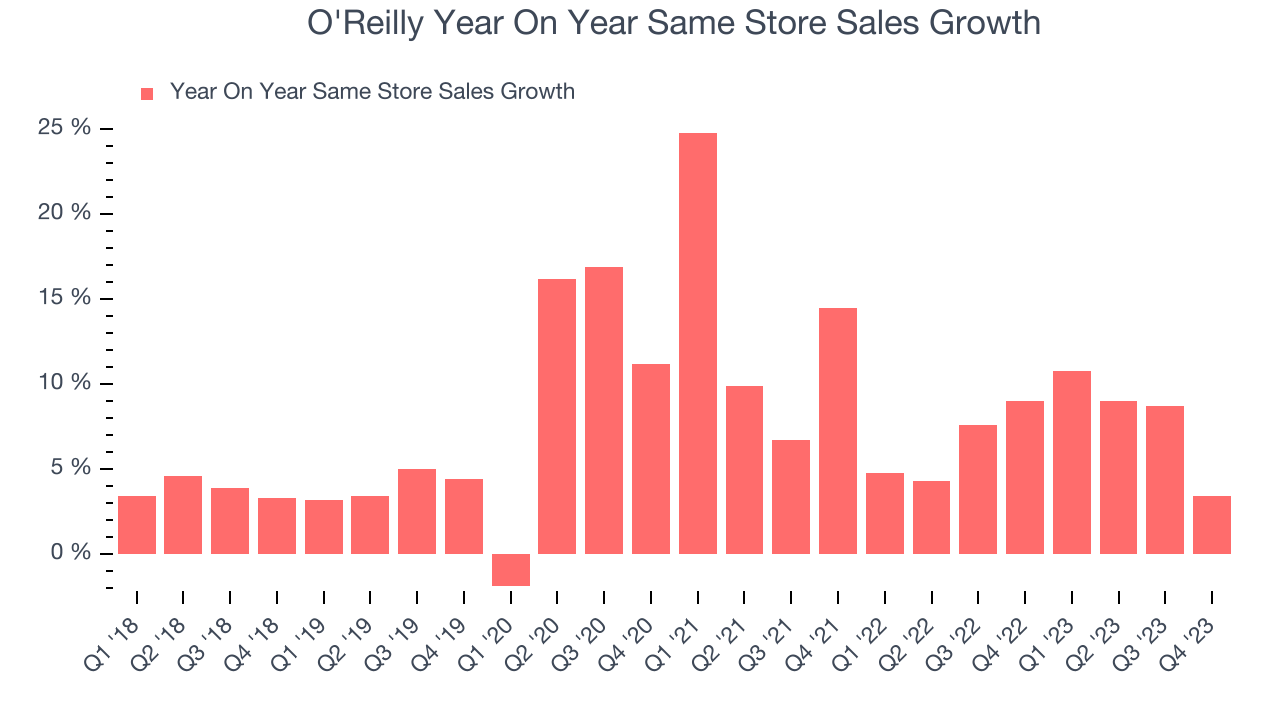

- Same-Store Sales were up 3.4% year on year

- Store Locations: 6,157 at quarter end, increasing by 186 over the last 12 months

- Market Capitalization: $62.23 billion

Brad Beckham, O’Reilly’s Chief Executive Officer (“CEO”), commented, “We are pleased to report another solid quarter, highlighted by a comparable store sales increase of 3.4%, on top of the very strong 9.0% comparable store sales increase Team O’Reilly delivered in the fourth quarter last year.

Serving both the DIY customer and professional mechanic, O’Reilly Automotive (NASDAQ:ORLY) is an auto parts and accessories retailer that sells everything from fuel pumps to car air fresheners to mufflers.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Sales Growth

O'Reilly is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 11.7% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new stores and grew sales at existing, established stores.

This quarter, O'Reilly's revenue grew 5.1% year on year to $3.83 billion, missing Wall Street's expectations. Looking ahead, Wall Street expects sales to grow 6.3% over the next 12 months, an acceleration from this quarter.

It’s not often you find a high-quality company at a significant discount to its historical P/E multiple, but that’s exactly what we found. Click here for your FREE report on this attractive Network Effect stock at a very silly price.

Same-Store Sales

O'Reilly's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 7.2% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, O'Reilly is reaching more customers and growing sales.

In the latest quarter, O'Reilly's same-store sales rose 3.4% year on year. By the company's standards, this growth was a meaningful deceleration from the 9% year-on-year increase it posted 12 months ago. We'll be watching O'Reilly closely to see if it can reaccelerate growth.

Key Takeaways from O'Reilly's Q4 Results

It was unfortunate that O'Reilly missed analysts' revenue and operating income estimates this quarter. That performance was driven by lower-than-expected same-store sales growth of 3.4%, though we note the company was coming off a tough comp period where its same-store sales growth clocked in at 9%.

On the positive side, it was encouraging to see O'Reilly beat Wall Street's EPS projections. Recapping the full year, O'Reilly opened 186 new stores, grew its distribution footprint in Mexico and Puerto Rico, and just closed its acquisition of Groupe Del Vasto in January 2024 to expand its Canadian operations. It also repurchased $3.15 billion of its shares during 2023 at an average price of $883.13 (in Q4, it repurchased $560 million at an average price of $922.86).

For 2024, the company provided full-year revenue guidance that slightly topped analysts' expectations. To arrive at its revenue guidance of $17 billion at the midpoint, O'Reilly expects to open 195 new stores while posting 4% same-store sales growth. Its EPS and free cash flow, however, came in lower. This means it'll be more challenging to sustain its historical pace of share buybacks, which have played a significant role in its return algorithm.

Overall, this was a mixed quarter for O'Reilly. The company is down 4.9% on the results and currently trades at $1,014.3 per share.

O'Reilly may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.