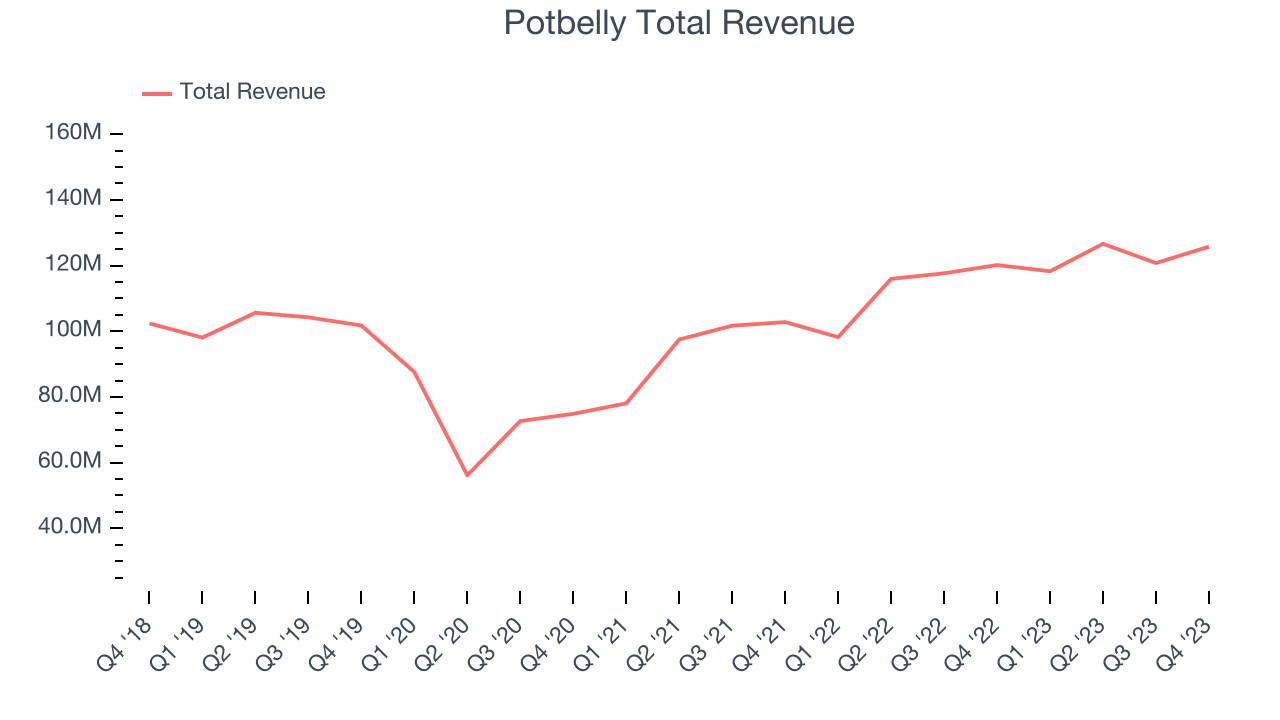

Casual sandwich chain Potbelly (NASDAQ:PBPB) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 4.7% year on year to $125.7 million. It made a non-GAAP profit of $0.02 per share, down from its profit of $0.09 per share in the same quarter last year.

Is now the time to buy Potbelly? Find out by accessing our full research report, it's free.

Potbelly (PBPB) Q4 FY2023 Highlights:

- Revenue: $125.7 million vs analyst estimates of $125.2 million (small beat)

- EPS (non-GAAP): $0.02 vs analyst expectations of $0.03 (33.3% miss)

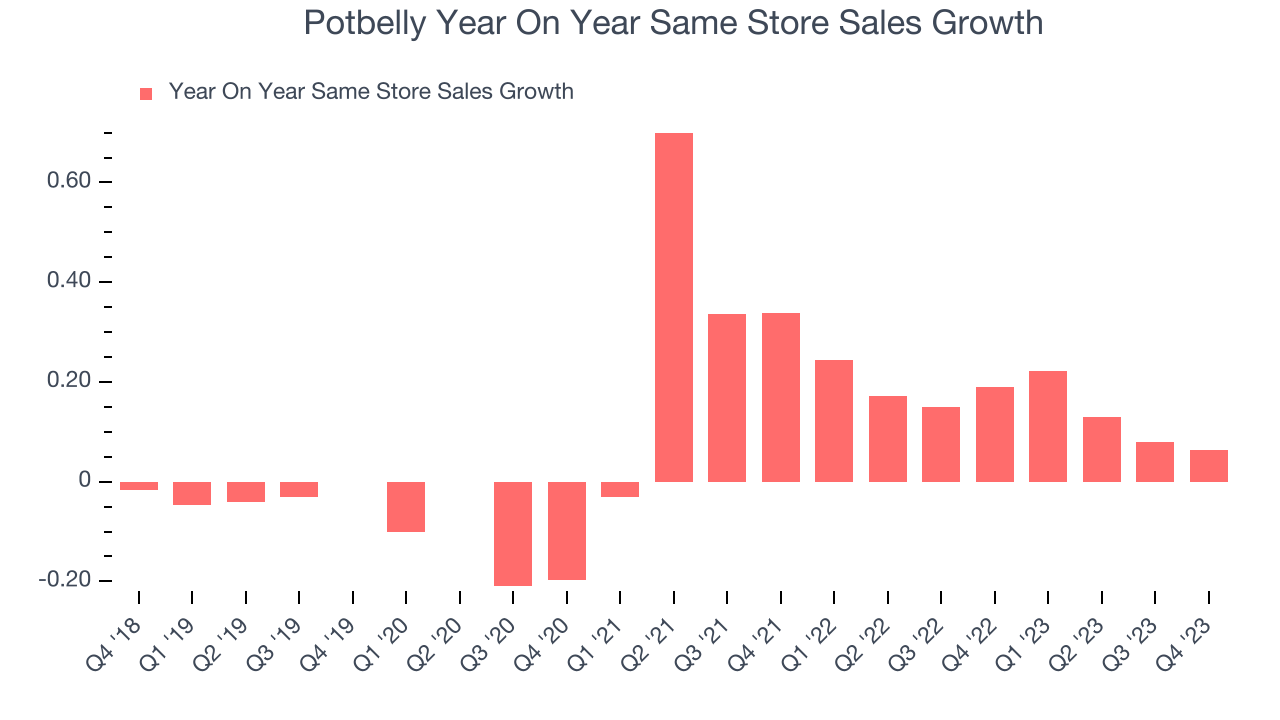

- Same-Store Sales were up 6.3% year on year

- Store Locations: 425 at quarter end, decreasing by 4 over the last 12 months

- Market Capitalization: $392.5 million

Bob Wright, President and Chief Executive Officer of Potbelly Corporation, commented, “I am very proud of what our team accomplished in the 4th quarter and full year 2023. Our Five-Pillar Strategy maintains our focus on what matters most to our customers and associates while growing our brand to the benefit of our franchisees and shareholders. Traffic driven sales, shop level and company profitability and unit growth development efforts headlined our success.”

With a unique origin story where the company actually started as an antique shop, Potbelly (NASDAQ:PBPB) today is a chain known for its toasty sandwiches.

Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Sales Growth

Potbelly is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale.

As you can see below, the company's annualized revenue growth rate of 4.7% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak , but to its credit, it opened new restaurants and grew sales at existing, established dining locations.

This quarter, Potbelly grew its revenue by 4.7% year on year, and its $125.7 million in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to decline 3.1% over the next 12 months, a deceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for restaurants.

Potbelly's demand has been spectacular for a restaurant business over the last eight quarters. On average, the company has grown its same-store sales by an impressive 15.6% year on year. This performance suggests its steady rollout of new restaurants is beneficial for shareholders. When a chain has strong demand, more locations should help it reach more customers seeking its meals.

In the latest quarter, Potbelly's same-store sales rose 6.3% year on year. By the company's standards, this growth was a meaningful deceleration from the 18.9% year-on-year increase it posted 12 months ago. We'll be watching Potbelly closely to see if it can reaccelerate growth.

Key Takeaways from Potbelly's Q4 Results

We were impressed by how significantly Potbelly blew past analysts' gross margin expectations this quarter. Other than that, most financial metrics were in line with estimates, including revenue, same-store sales growth, and EPS. For the full-year 2024, Potbelly expects same-store sales growth in the mid-to-low single digits and 10% growth in its number of restaurants. Zooming out, we think this was still a decent quarter, showing that the company is staying on track. The stock is flat after reporting and currently trades at $13.55 per share.

So should you invest in Potbelly right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.