Casino, sports betting and entertainment operator PENN Entertainment (NASDAQ:PENN) fell short of analysts' expectations in Q1 CY2024, with revenue down 4% year on year to $1.61 billion. It made a GAAP loss of $0.76 per share, down from its profit of $3.05 per share in the same quarter last year.

PENN Entertainment (PENN) Q1 CY2024 Highlights:

- Revenue: $1.61 billion vs analyst estimates of $1.63 billion (1.4% miss)

- EPS: -$0.76 vs analyst expectations of -$0.59 (29.8% miss)

- Gross Margin (GAAP): 29.6%, down from 41.8% in the same quarter last year

- Market Capitalization: $2.51 billion

Established in 1982, PENN Entertainment (NASDAQ:PENN) is a diversified American operator of casinos, sports betting, and entertainment venues.

PENN Entertainment started as a small casino operator and has since expanded to include sports betting and entertainment venues.

Today, the company's services encompass casino gaming, sports betting, and diverse entertainment options across its properties. It has strategically embraced the surge in online sports betting, offering digital wagering alongside traditional in-person services. This approach not only caters to the classic casino-goer but also to a newer, tech-savvy audience. Beyond gaming, PENN Entertainment's venues provide a variety of dining and entertainment choices, addressing the demand for multifaceted leisure experiences.

The company's revenue streams are a blend of physical and online gaming operations, sports betting, and entertainment services.

Casino Operator

Casino operators enjoy limited competition because gambling is a highly regulated industry. These companies can also enjoy healthy margins and profits. Have you ever heard the phrase ‘the house always wins’? Regulation cuts both ways, however, and casinos may face stroke-of-the-pen risk that suddenly limits what they can or can't do and where they can do it. Furthermore, digitization is changing the game, pun intended. Whether it’s online poker or sports betting on your smartphone, innovation is forcing these players to adapt to changing consumer preferences, such as being able to wager anywhere on demand.

Competitors in the gaming and entertainment sector include Caesars Entertainment (NASDAQ:CZR), MGM Resorts (NYSE:MGM), and Boyd Gaming (NYSE:BYD).Sales Growth

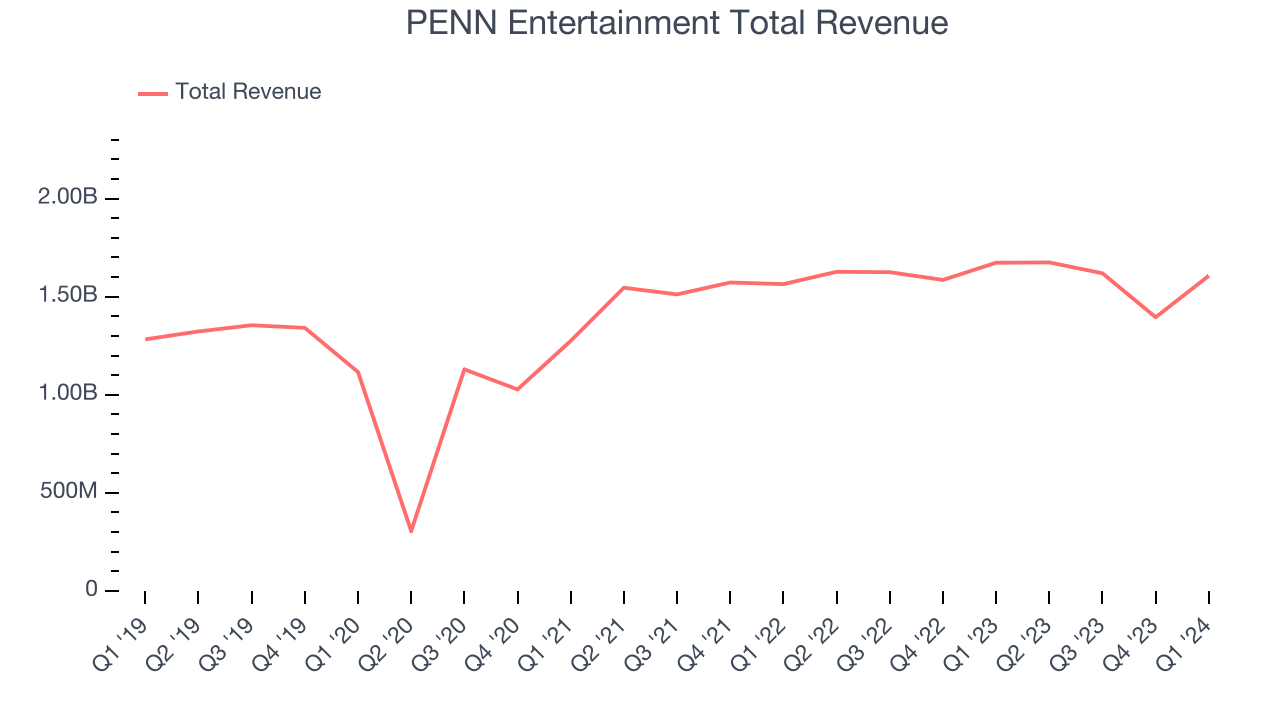

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. PENN Entertainment's annualized revenue growth rate of 7.5% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. PENN Entertainment's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. PENN Entertainment's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

This quarter, PENN Entertainment missed Wall Street's estimates and reported a rather uninspiring 4% year-on-year revenue decline, generating $1.61 billion of revenue. Looking ahead, Wall Street expects sales to grow 10.9% over the next 12 months, an acceleration from this quarter.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

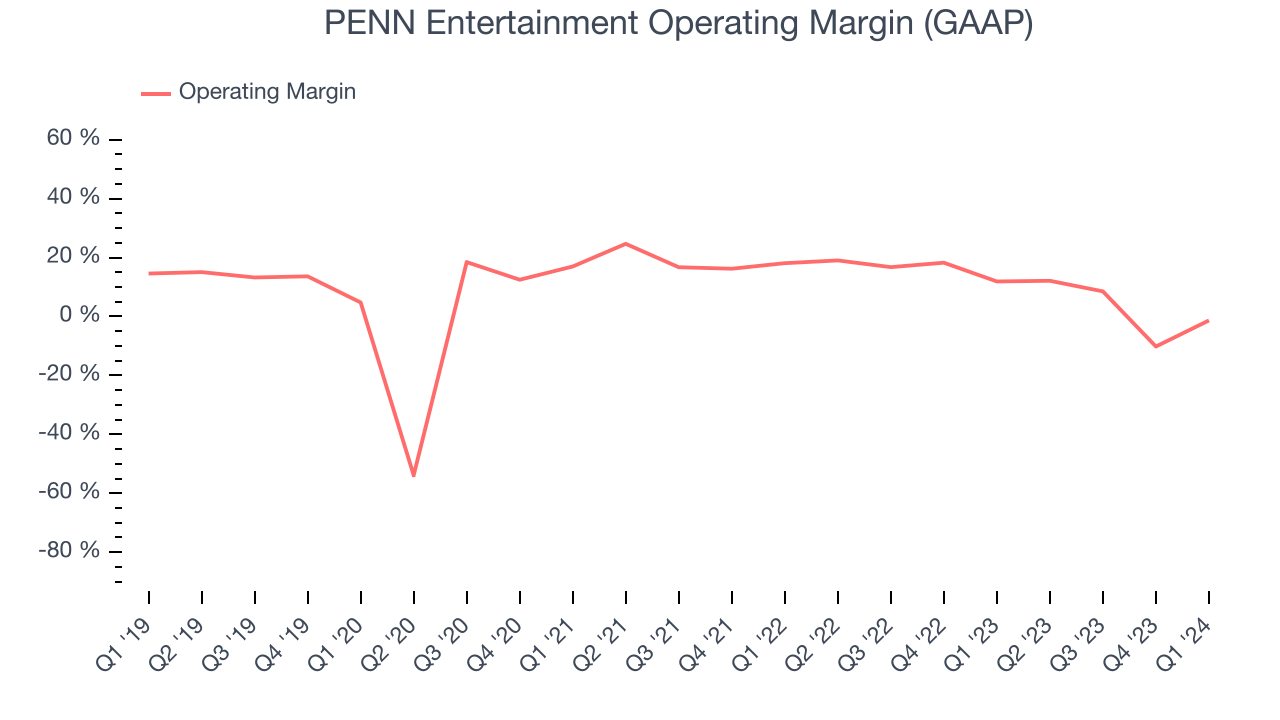

PENN Entertainment was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer discretionary business, producing an average operating margin of 9.7%.

In Q1, PENN Entertainment generated an operating profit margin of negative 1.3%, down 13.2 percentage points year on year.

Over the next 12 months, Wall Street expects PENN Entertainment to become more profitable. Analysts are expecting the company’s LTM operating margin of 2.8% to rise to 5.5%.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

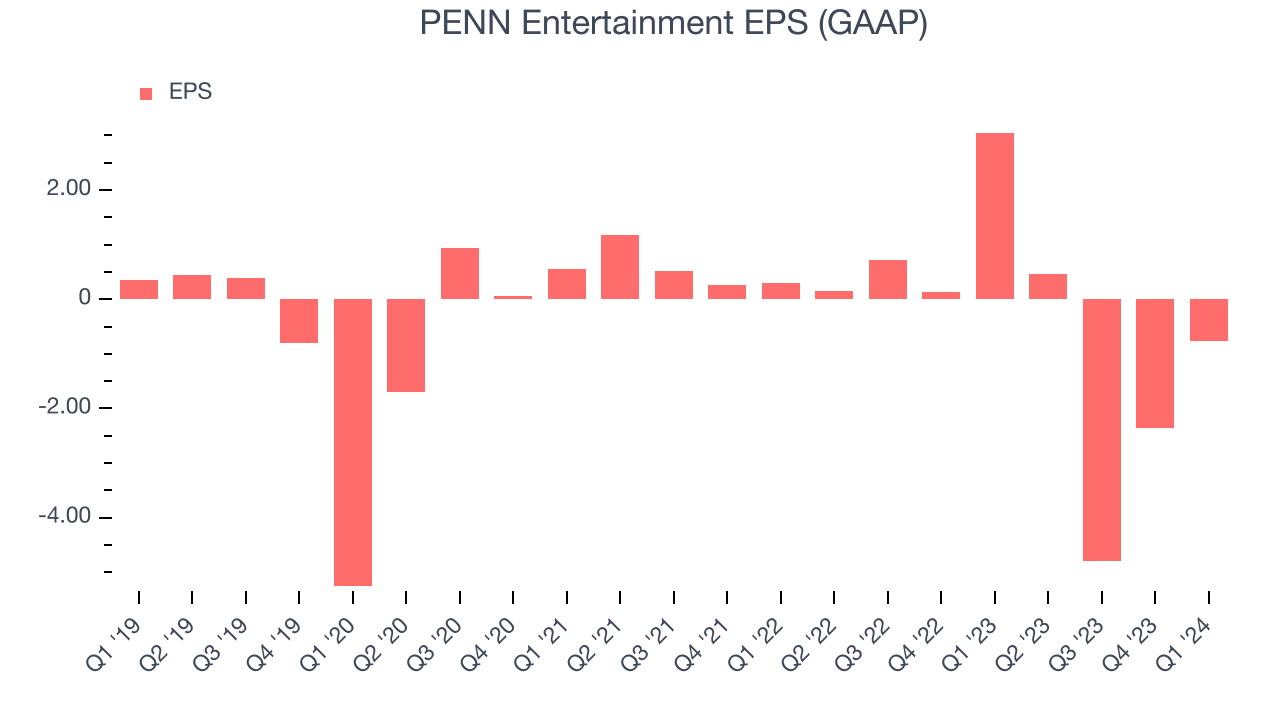

Over the last five years, PENN Entertainment's EPS dropped 2,333%, translating into 89.3% annualized declines. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends or consumer preferences. Consumer discretionary companies are particularly exposed to this, leaving a low margin of safety around the company (making the stock susceptible to large downward swings).

In Q1, PENN Entertainment reported EPS at negative $0.76, down from $3.05 in the same quarter last year. This print unfortunately missed analysts' estimates. Over the next 12 months, Wall Street is optimistic. Analysts are projecting PENN Entertainment's LTM EPS of negative $7.47 to reach break even.

Return on Invested Capital (ROIC)

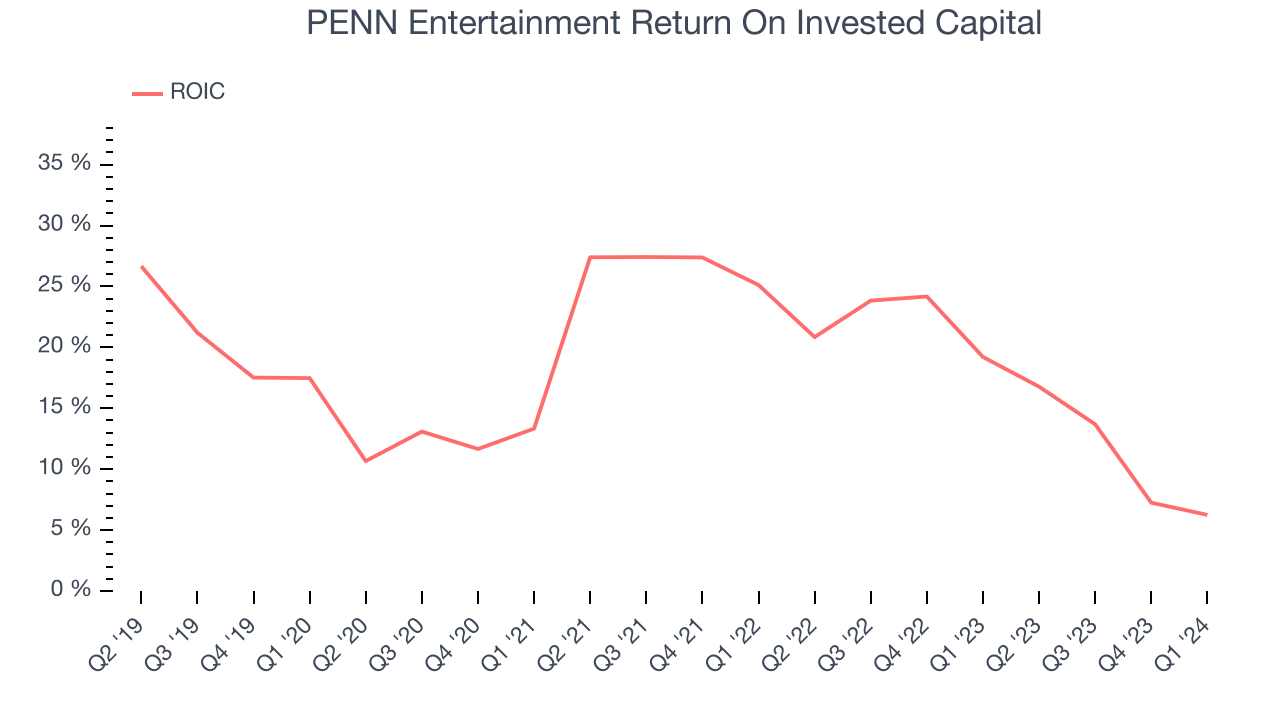

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

PENN Entertainment's five-year average return on invested capital was 16.3%, slightly better than the broader sector. Just as you’d like your investment dollars to generate returns, PENN Entertainment's invested capital has produced decent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, PENN Entertainment's ROIC averaged 2.7 percentage point decreases over the last few years. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

PENN Entertainment reported $903.6 million of cash and $2.63 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $612.5 million of EBITDA over the last 12 months, we view PENN Entertainment's 2.8x net-debt-to-EBITDA ratio as safe. We also see its $209.8 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from PENN Entertainment's Q1 Results

Revenue missed but ESPN BET was a bright spot. "ESPN BET...led to record online sports betting handle and iCasino gross gaming revenue in the quarter." The company also announced the hiring of Aaron LaBerge as the new Chief Technology Officer. “Mr. LaBerge brings more than 20 years of experience at The Walt Disney Company, most recently serving as the CTO for both Disney Entertainment and ESPN." The stock is up 2.1% after reporting and currently trades at $16.75 per share.

Is Now The Time?

PENN Entertainment may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of PENN Entertainment, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last five years, but at least growth is expected to increase in the short term. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its declining EPS over the last five years makes it hard to trust. On top of that, its low free cash flow margins give it little breathing room.

While there are some things to like about PENN Entertainment and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $25.56 per share right before these results (compared to the current share price of $16.75).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.