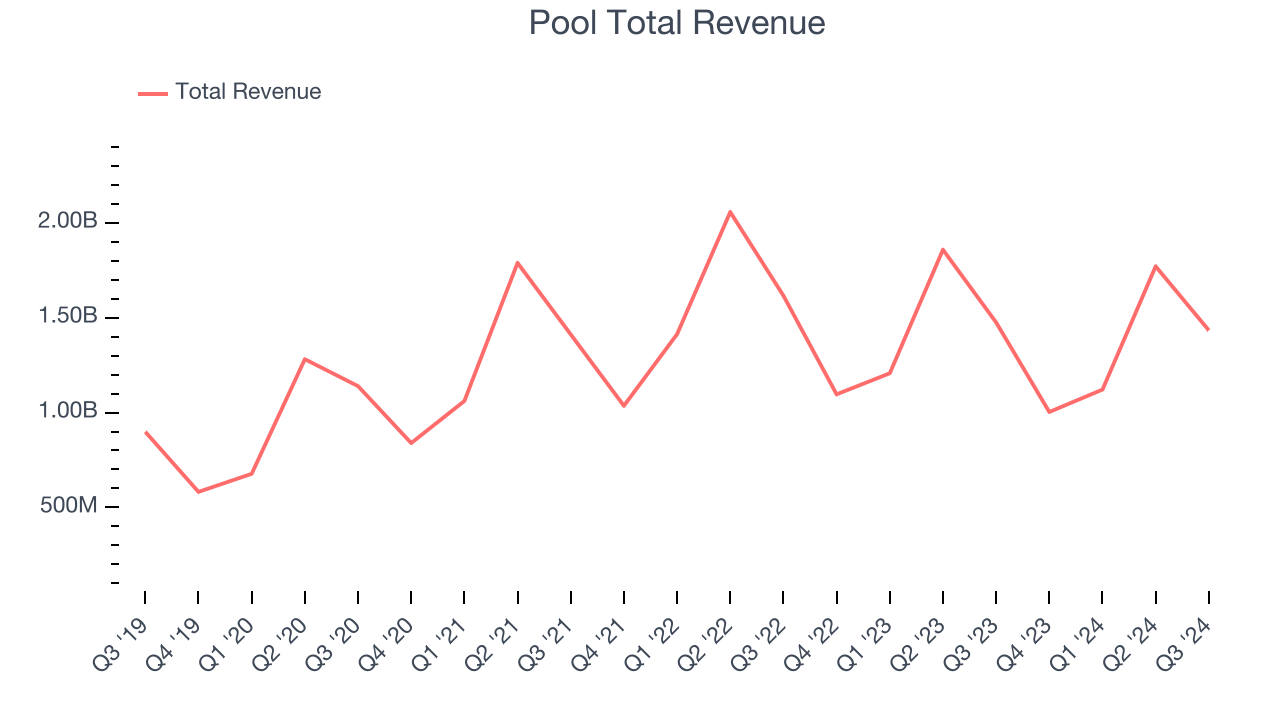

Swimming pool distributor Pool (NASDAQ:POOL) reported Q3 CY2024 results exceeding the market’s revenue expectations, but sales fell 2.8% year on year to $1.43 billion. Its GAAP profit of $3.27 per share was also 4% above analysts’ consensus estimates.

Is now the time to buy Pool? Find out by accessing our full research report, it’s free.

Pool (POOL) Q3 CY2024 Highlights:

- Revenue: $1.43 billion vs analyst estimates of $1.40 billion (2.1% beat)

- EPS: $3.27 vs analyst estimates of $3.14 (4% beat)

- EBITDA: $191.5 million vs analyst estimates of $187.3 million (2.2% beat)

- EPS (GAAP) guidance for the full year is $11.26 at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 29.1%, in line with the same quarter last year

- Operating Margin: 12.3%, in line with the same quarter last year

- EBITDA Margin: 13.4%, in line with the same quarter last year

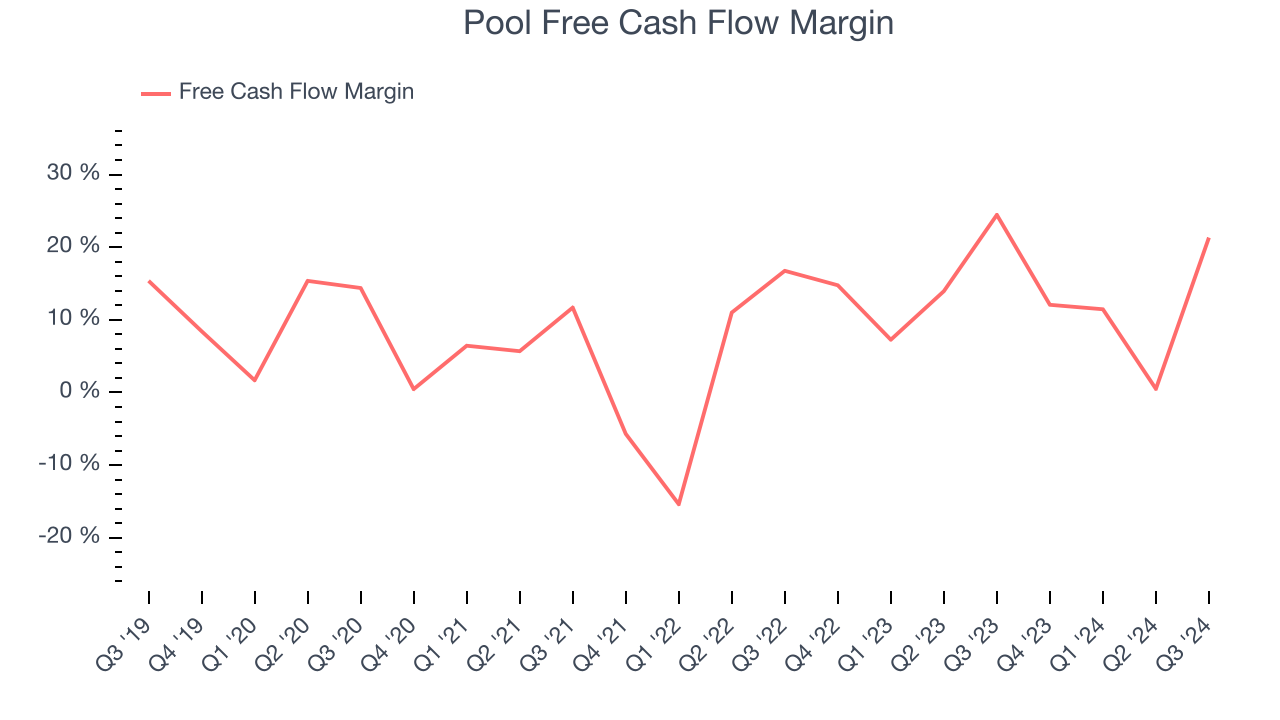

- Free Cash Flow Margin: 21.3%, down from 24.4% in the same quarter last year

- Market Capitalization: $13.42 billion

“We generated third quarter net sales of $1.4 billion, down 3% from the third quarter of 2023, supported by steady demand for maintenance products while the discretionary portions of our business continued to see pressure. During the quarter, we made additional progress on our Pool360 technology rollouts and digital marketing expansion, seeing strong private-label chemical sales growth, higher Pool360 usage and sustained gross margins. Our dedicated team remains focused on delivering a best-in-class customer experience and positioning ourselves for future growth by leveraging our connected software solutions and the power of our nationwide, integrated distribution network, with an efficient capital structure and strong cash flow generation,” commented Peter D. Arvan, president and CEO.

Company Overview

Founded in 1993 and headquartered in Louisiana, Pool (NASDAQ:POOL) is one of the largest wholesale distributors of swimming pool supplies, equipment, and related leisure products.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Pool grew its sales at a tepid 11% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Pool’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.7% annually.

This quarter, Pool’s revenue fell 2.8% year on year to $1.43 billion but beat Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, an acceleration versus the last two years. Although this projection indicates the market thinks its newer products and services will fuel better performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Pool has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 13.1% over the last two years, better than the broader consumer discretionary sector.

Pool’s free cash flow clocked in at $305.5 million in Q3, equivalent to a 21.3% margin. The company’s cash profitability regressed as it was 3.1 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

Over the next year, analysts predict Pool’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 10.6% for the last 12 months will decrease to 8.1%.

Key Takeaways from Pool’s Q3 Results

It was good to see Pool beat analysts’ revenue expectations this quarter. We were also happy its EPS narrowly outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock traded up 1.4% to $355.90 immediately following the results.

So should you invest in Pool right now?When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.