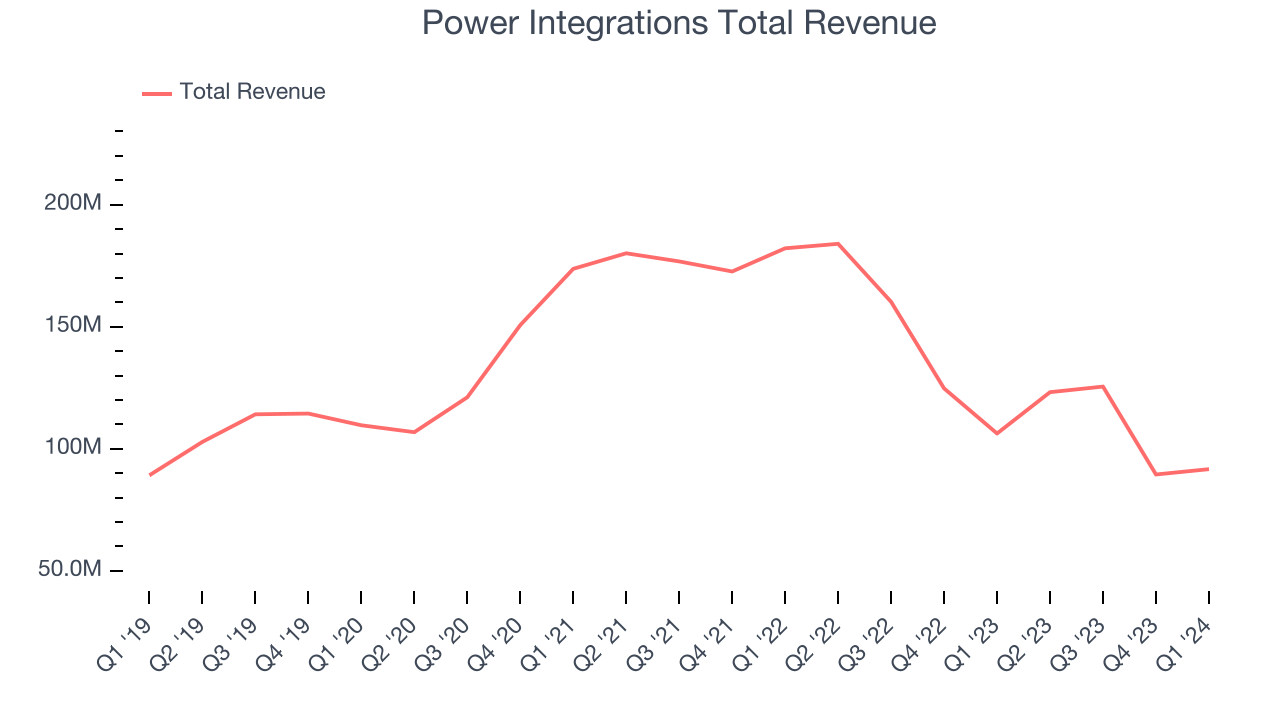

Semiconductor designer Power Integrations (NASDAQ:POWI) reported Q1 CY2024 results topping analysts' expectations, with revenue down 13.7% year on year to $91.69 million. Guidance for next quarter's revenue was also better than expected at $105 million at the midpoint, 1.4% above analysts' estimates. It made a non-GAAP profit of $0.18 per share, down from its profit of $0.25 per share in the same quarter last year.

Power Integrations (POWI) Q1 CY2024 Highlights:

- Revenue: $91.69 million vs analyst estimates of $89.96 million (1.9% beat)

- EPS (non-GAAP): $0.18 vs analyst estimates of $0.13 (39.5% beat)

- Revenue Guidance for Q2 CY2024 is $105 million at the midpoint, above analyst estimates of $103.5 million

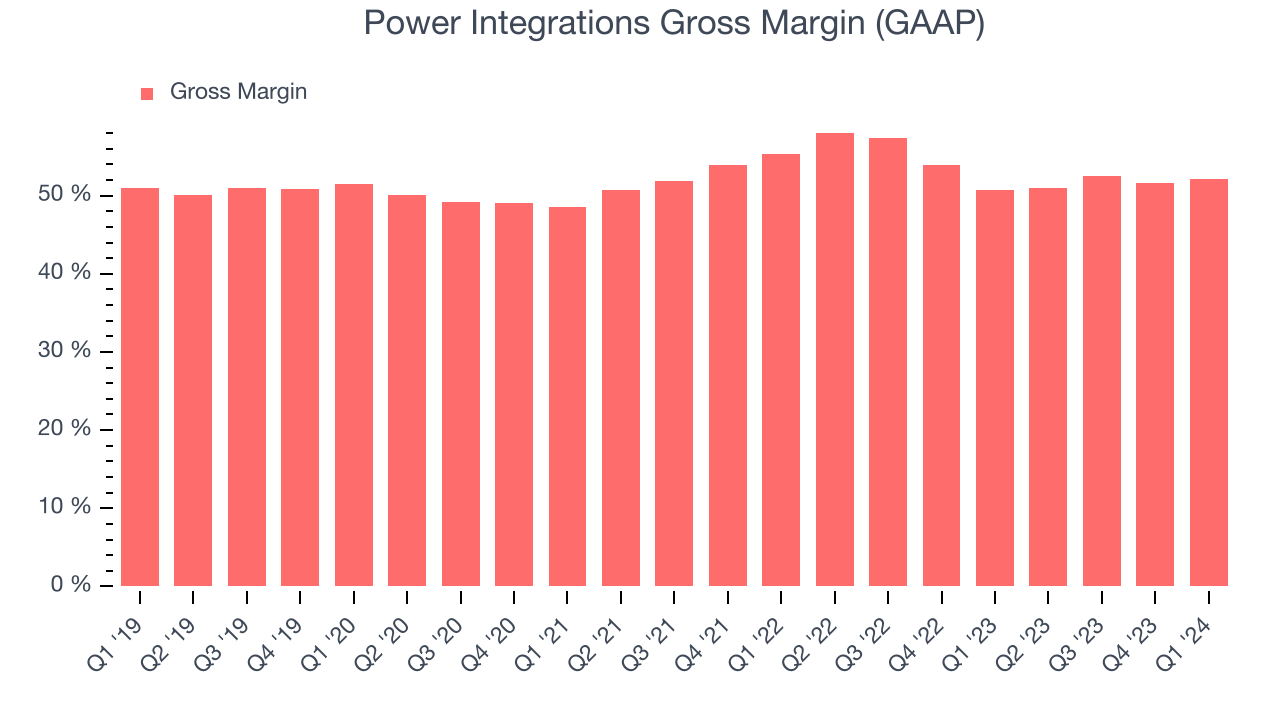

- Gross Margin (GAAP): 52.1%, up from 50.8% in the same quarter last year

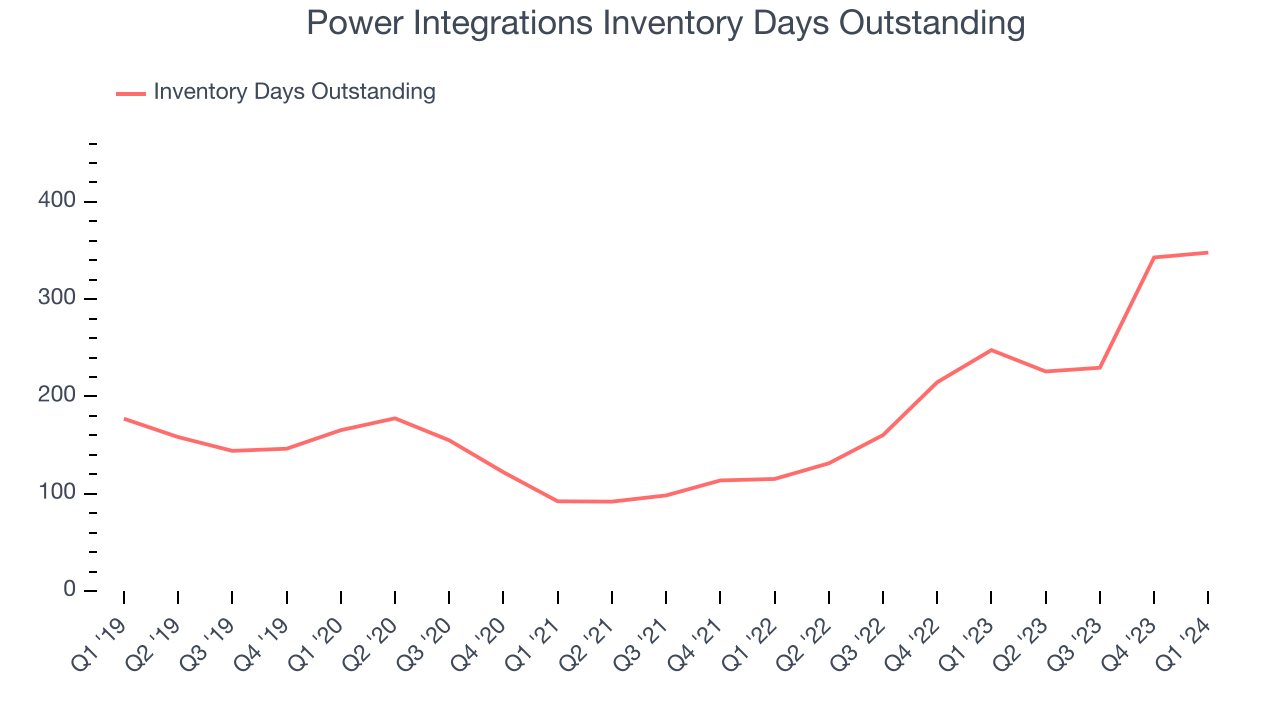

- Inventory Days Outstanding: 348, up from 343 in the previous quarter

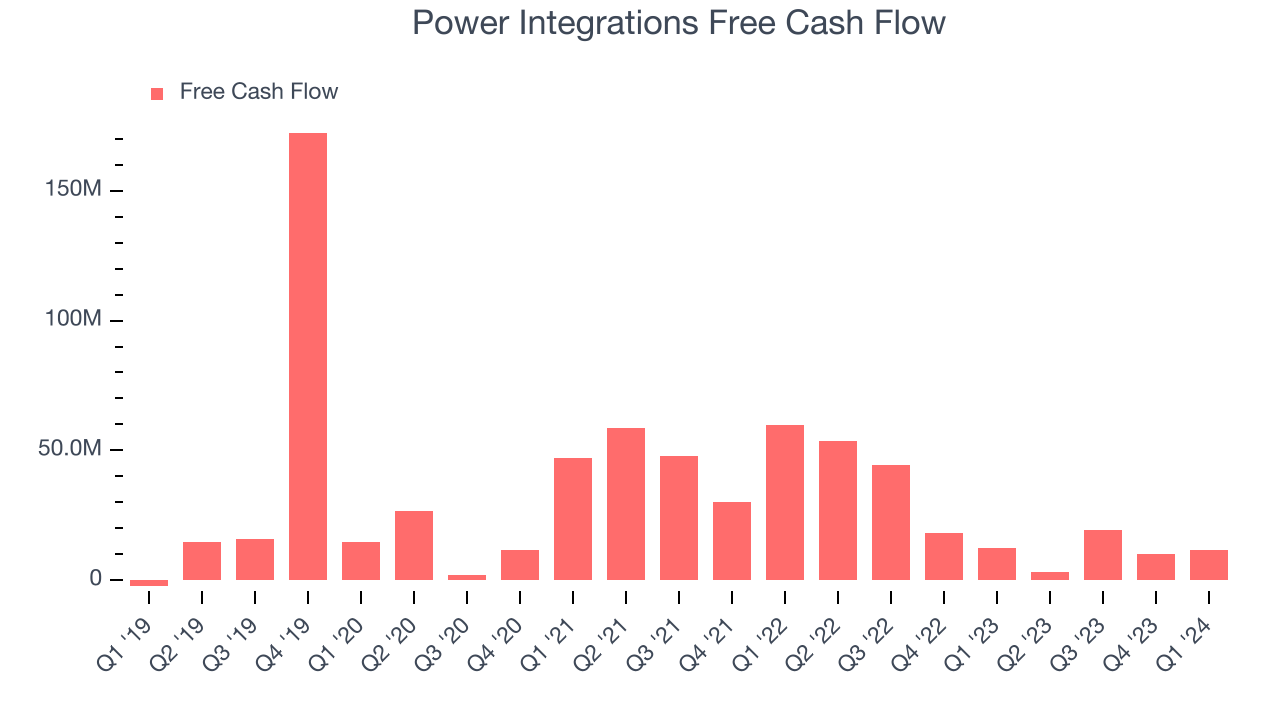

- Free Cash Flow of $11.56 million, up 14.2% from the previous quarter

- Market Capitalization: $3.96 billion

A leading supplier of parts for electronics such as home appliances, Power Integrations (NASDAQ:POWI) is a semiconductor designer and developer specializing in products used for high-voltage power conversion.

Power Integrations was founded in 1988 by Ray Orr and Steven Sharp. The company went public in December of 1997 and is currently headquartered in San Jose, California.

Almost all electronic devices that plug into a wall socket require a power supply to convert the high-voltage alternating current provided by electric utilities into the low-voltage direct current required by most electronic devices. POWI’s products address this need by converting alternating current (AC) to direct current (DC) or vice versa, reducing or increasing the voltage, and regulating the output voltage/current according to customer specifications.

POWI serves customers in four end-market groups: Consumer (e.g. manufacturers of home appliances, TVs), Communications (e.g. mobile phone chargers, adapters for routers), Industrial (e.g. motor controls, battery-powered tools), and Computer (smart home devices, wearables). POWI then contracts with three foundries for the manufacture of most of its silicon wafers.

Competitors in the market for high-voltage ICs include ON Semiconductor (NASDAQ:ON) STMicroelectronics (NYSE:STM), NXP Semiconductors (NASDAQ:NXPI), and Infineon.Sales Growth

Power Integrations's revenue has been declining over the last three years, dropping by 3.3% on average per year. This quarter, its revenue declined from $106.3 million in the same quarter last year to $91.69 million. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Even though Power Integrations surpassed analysts' revenue estimates, this was a slow quarter for the company as its revenue dropped 13.7% year on year. This could mean that the current downcycle is deepening.

Power Integrations may be headed for an upturn. Although the company is guiding for a year-on-year revenue decline of 14.8% next quarter, analysts are expecting revenue to grow 17.5% over the next 12 months.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Power Integrations's DIO came in at 348, which is 174 days above its five-year average, suggesting that the company's inventory has grown to higher levels than we've seen in the past.

Pricing Power

In the semiconductor industry, a company's gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor. Power Integrations's gross profit margin, which shows how much money the company gets to keep after paying key materials, input, and manufacturing costs, came in at 52.1% in Q1, up 1.4 percentage points year on year.

Despite declining over the past year, Power Integrations still retains industry standard gross margins, averaging 51.8%, pointing to its competitive offering, decent cost controls, and possibly modest pricing pressure.

Profitability

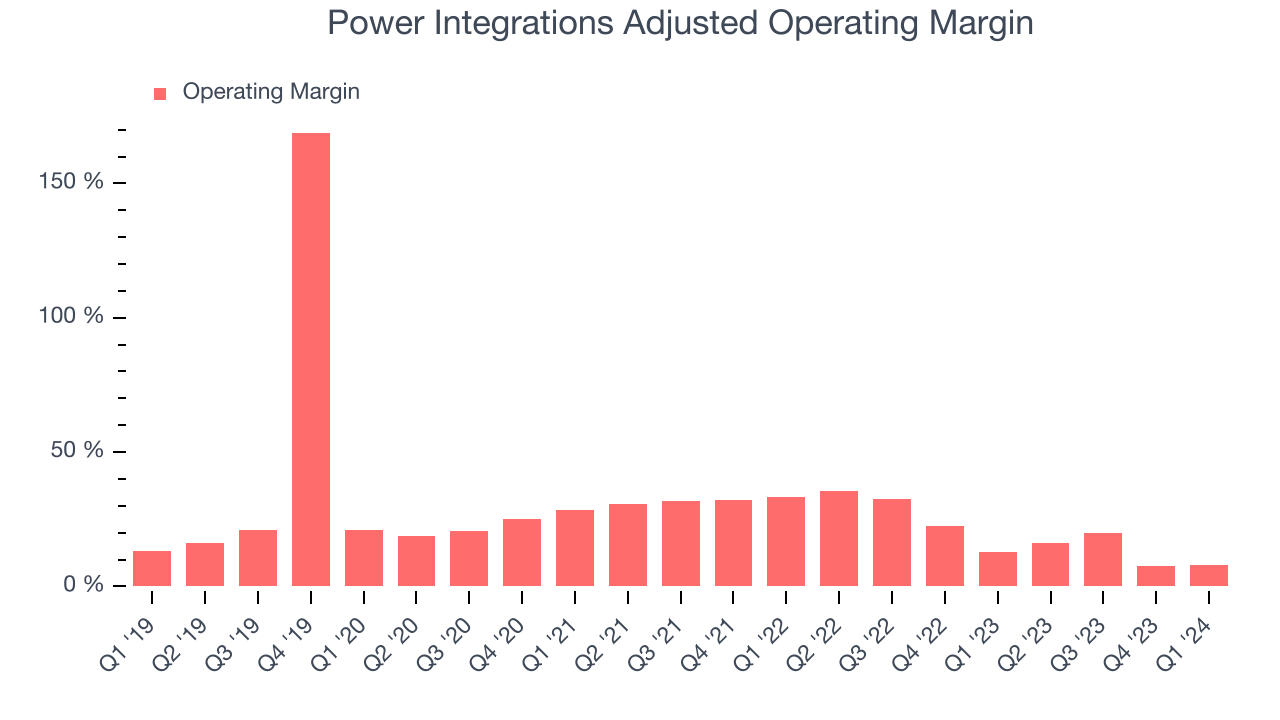

Power Integrations reported an operating margin of 8% in Q1, down 4.8 percentage points year on year. Operating margins are one of the best measures of profitability because they tell us how much money a company takes home after manufacturing its products, marketing and selling them, and, importantly, keeping them relevant through research and development.

Power Integrations's operating margins have been trending down over the last year, averaging 13.8%. This is a bad sign for Power Integrations, whose margins are already below average for semiconductor companies. To its credit, however, the company's margins suggest modest pricing power and cost controls.

Earnings, Cash & Competitive Moat

Analysts covering Power Integrations expect earnings per share to grow 45.6% over the next 12 months, although estimates will likely change after earnings.

Although earnings are important, we believe cash is king because you can't use accounting profits to pay the bills. Power Integrations's free cash flow came in at $11.56 million in Q1, down 7.5% year on year.

Power Integrations has generated $43.93 million in free cash flow over the last 12 months, or 10.2% of revenue. This FCF margin enables it to reinvest in its business without depending on the capital markets.

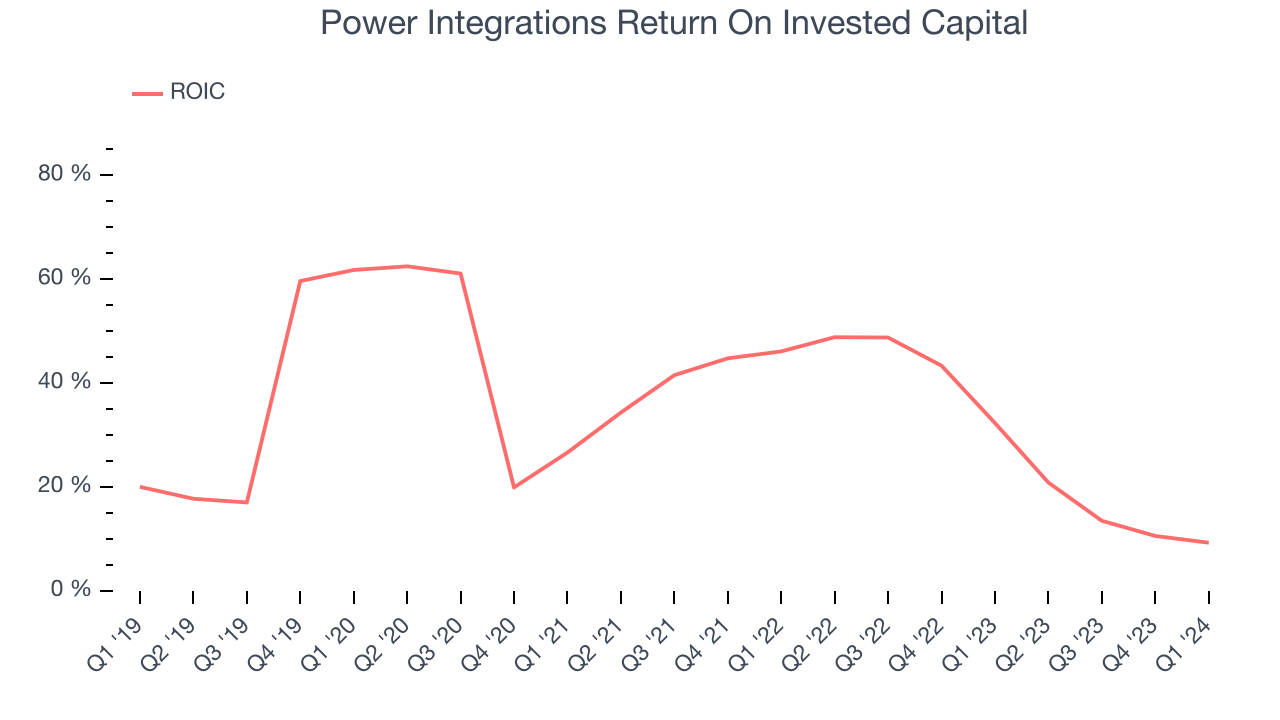

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Power Integrations's five-year average ROIC was 35.2%, placing it among the best semiconductor companies. Just as you’d like your investment dollars to generate returns, Power Integrations's invested capital has produced excellent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Power Integrations's ROIC significantly decreased over the last few years. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Key Takeaways from Power Integrations's Q1 Results

We were impressed by how significantly Power Integrations blew past analysts' EPS expectations this quarter. We were also glad its revenue outperformed Wall Street's estimates. On the other hand, its operating margin regrettably fell. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is flat after reporting and currently trades at $70.17 per share.

Is Now The Time?

When considering an investment in Power Integrations, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although we have other favorites, we understand the arguments that Power Integrations isn't a bad business. Although its revenue has declined over the last three years with analysts expecting growth to slow from here, its stellar ROIC suggests it has been a well-run company historically. Investors should still be cautious, however, as its operating margins reveal subpar cost controls compared to other semiconductor businesses.

The market is certainly expecting long-term growth from Power Integrations given its price-to-earnings ratio based on the next 12 months is 47.4x. There are things to like about Power Integrations and there's no doubt it's a bit of a market darling, at least for some. But it seems that there's a lot of optimism already priced in and we are wondering whether there might be better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $87.60 per share right before these results (compared to the current share price of $70.17).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.