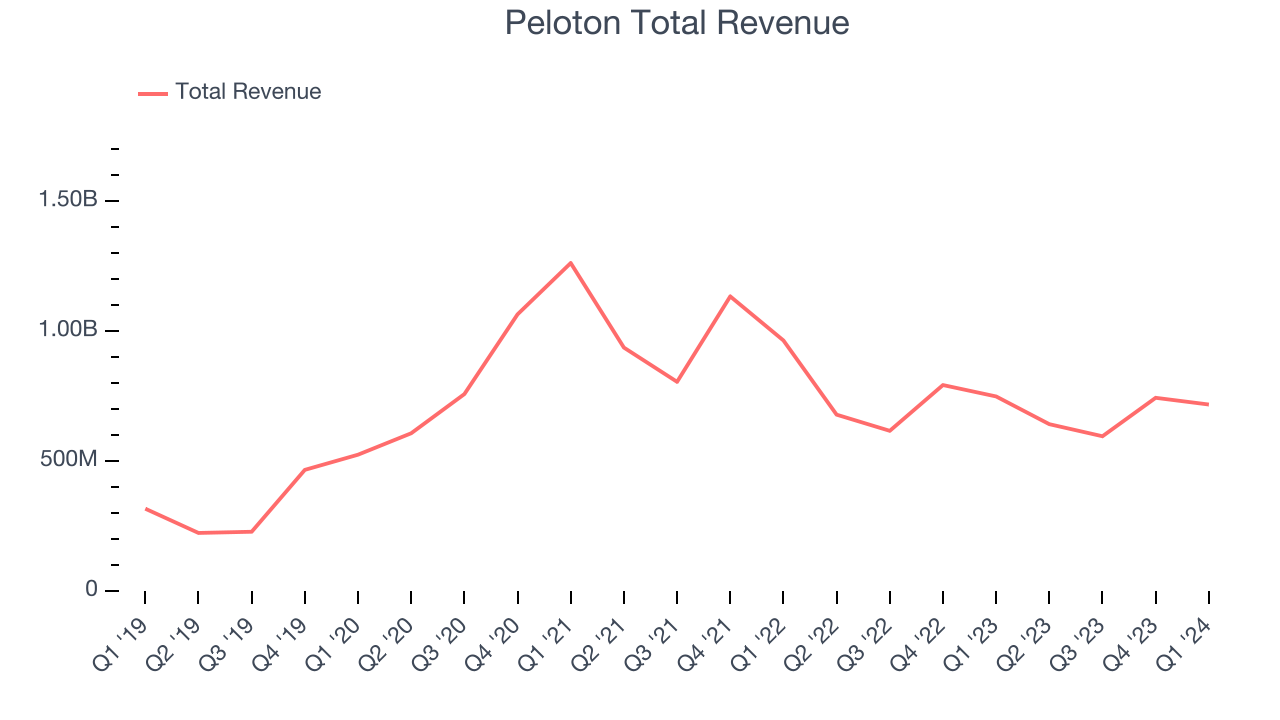

Exercise equipment company Peloton (NASDAQ:PTON) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 4.2% year on year to $717.7 million. On the other hand, the company's full-year revenue guidance of $2.69 billion at the midpoint came in slightly below analysts' estimates. It made a GAAP loss of $0.45 per share, improving from its loss of $0.79 per share in the same quarter last year.

Is now the time to buy Peloton? Find out by accessing our full research report, it's free.

Peloton (PTON) Q1 CY2024 Highlights:

- CEO Barry McCarthy to step down, company initiates restructuring program that will include layoffs of 15% of workforce

- Revenue: $717.7 million vs analyst estimates of $718.6 million (small miss)

- EPS: -$0.45 vs analyst expectations of -$0.36 (24% miss)

- The company dropped its revenue guidance for the full year from $2.71 billion to $2.69 billion at the midpoint, a 0.9% decrease

- Gross Margin (GAAP): 43.2%, up from 36.1% in the same quarter last year

- Free Cash Flow of $8.6 million is up from -$37.1 million in the previous quarter

- Connected Fitness Subscribers: 3.06 million

- Market Capitalization: $1.18 billion

Started as a Kickstarter campaign, Peloton (NASDAQ: PTON) is a fitness technology company known for its at-home exercise equipment and interactive online workout classes.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Peloton's annualized revenue growth rate of 27.6% over the last five years was exceptional for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Peloton's recent history shows a reversal from its five-year trend, as its revenue has shown annualized declines of 16.2% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Peloton's recent history shows a reversal from its five-year trend, as its revenue has shown annualized declines of 16.2% over the last two years.

This quarter, Peloton reported a rather uninspiring 4.2% year-on-year revenue decline to $717.7 million of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2.5% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

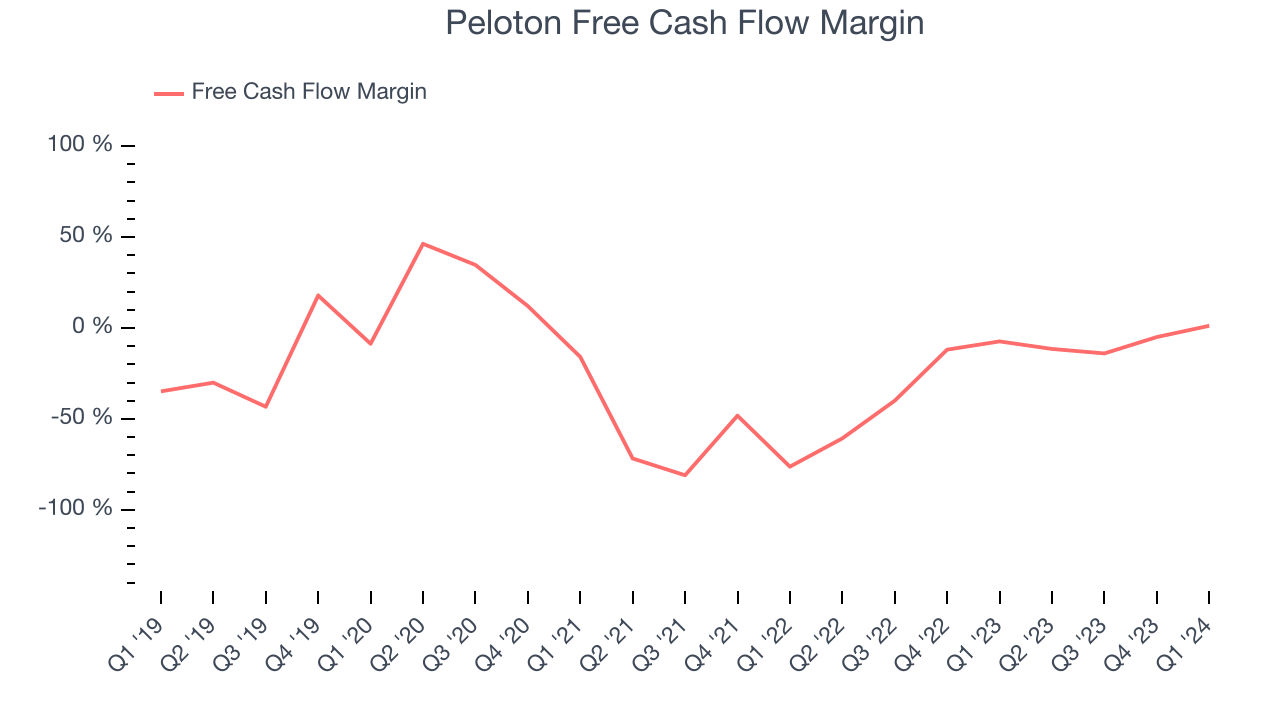

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

While Peloton posted positive free cash flow this quarter, the broader story hasn't been so clean. Over the last two years, Peloton's demanding reinvestments to stay relevant with consumers have drained company resources. Its free cash flow margin has been among the worst in the consumer discretionary sector, averaging negative 18%.

Peloton's free cash flow came in at $8.6 million in Q1, equivalent to a 1.2% margin. This result was great for the business as it flipped from cash flow negative in the same quarter last year to cash flow positive this quarter.

Key Takeaways from Peloton's Q1 Results

The big news here isn't related to the quarter's financials. Peloton that CEO Barry McCarthy (formerly of Netflix and Spotify) will be stepping down just over two years after he took over from founder John Foley. The company also announced a restructuring program to cut costs, and this will include laying off 15% of its workforce or roughly 400 employees. With regards to the numbers, they weren't good. EPS missed and its operating margin fell short of Wall Street's estimates. The company lowered full year revenue guidance. Overall, the results could have been better. The stock is up 13.8% after reporting and currently trades at $3.68 per share.

So should you invest in Peloton right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.