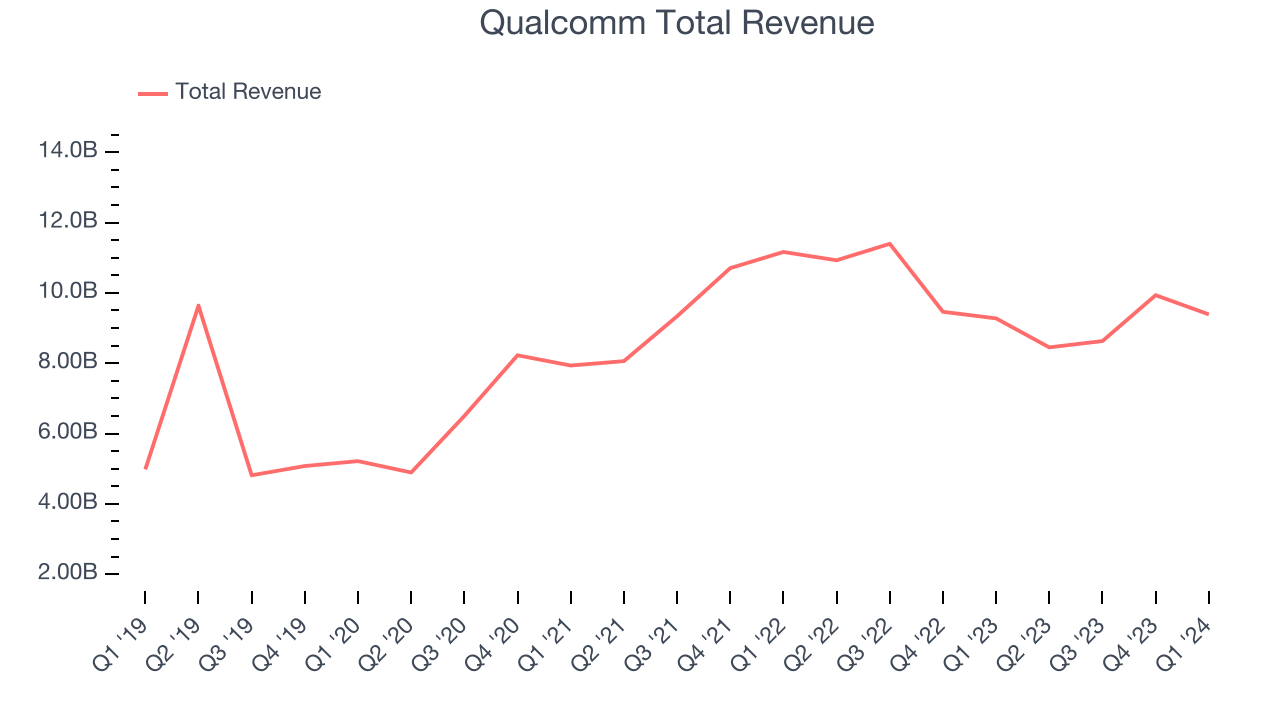

Wireless chipmaker Qualcomm (NASDAQ:QCOM) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 1.2% year on year to $9.39 billion. The company expects next quarter's revenue to be around $9.2 billion, coming in 1.6% above analysts' estimates. It made a non-GAAP profit of $2.44 per share, improving from its profit of $2.15 per share in the same quarter last year.

Qualcomm (QCOM) Q1 CY2024 Highlights:

- Revenue: $9.39 billion vs analyst estimates of $9.35 billion (small beat)

- EPS (non-GAAP): $2.44 vs analyst estimates of $2.32 (5.3% beat)

- Revenue Guidance for Q2 CY2024 is $9.2 billion at the midpoint, above analyst estimates of $9.05 billion

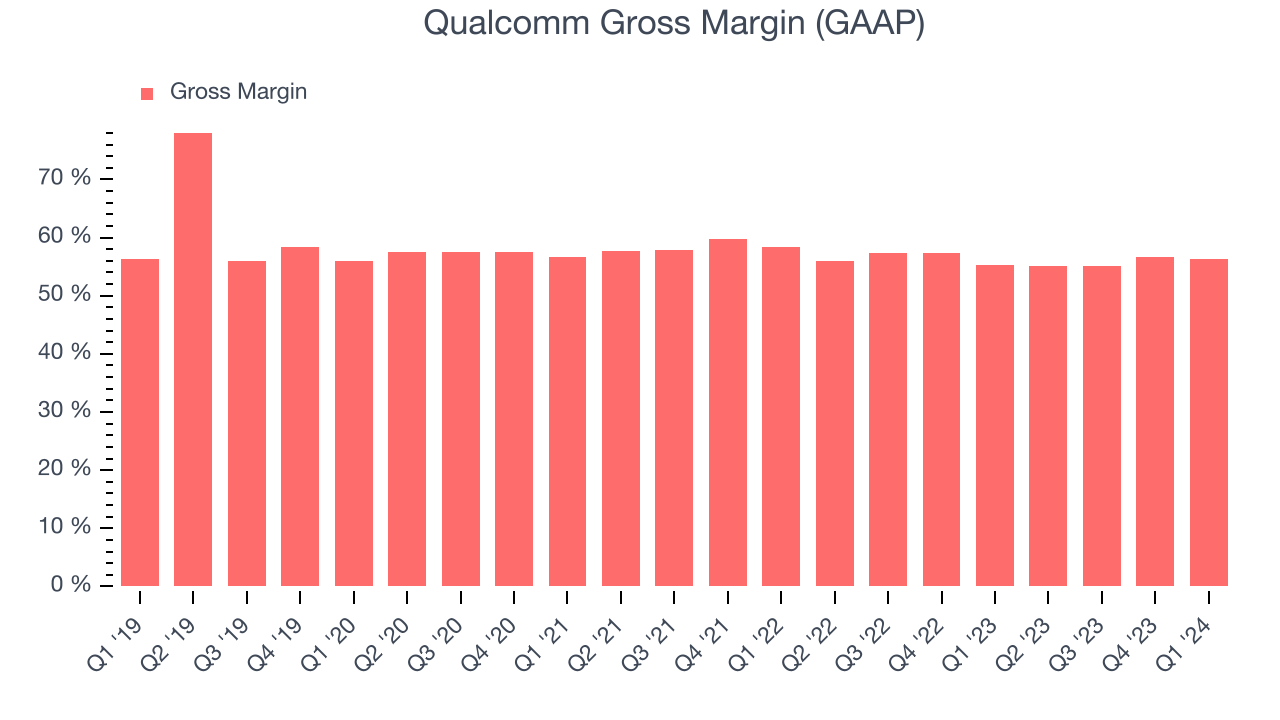

- Gross Margin (GAAP): 56.3%, up from 55.2% in the same quarter last year

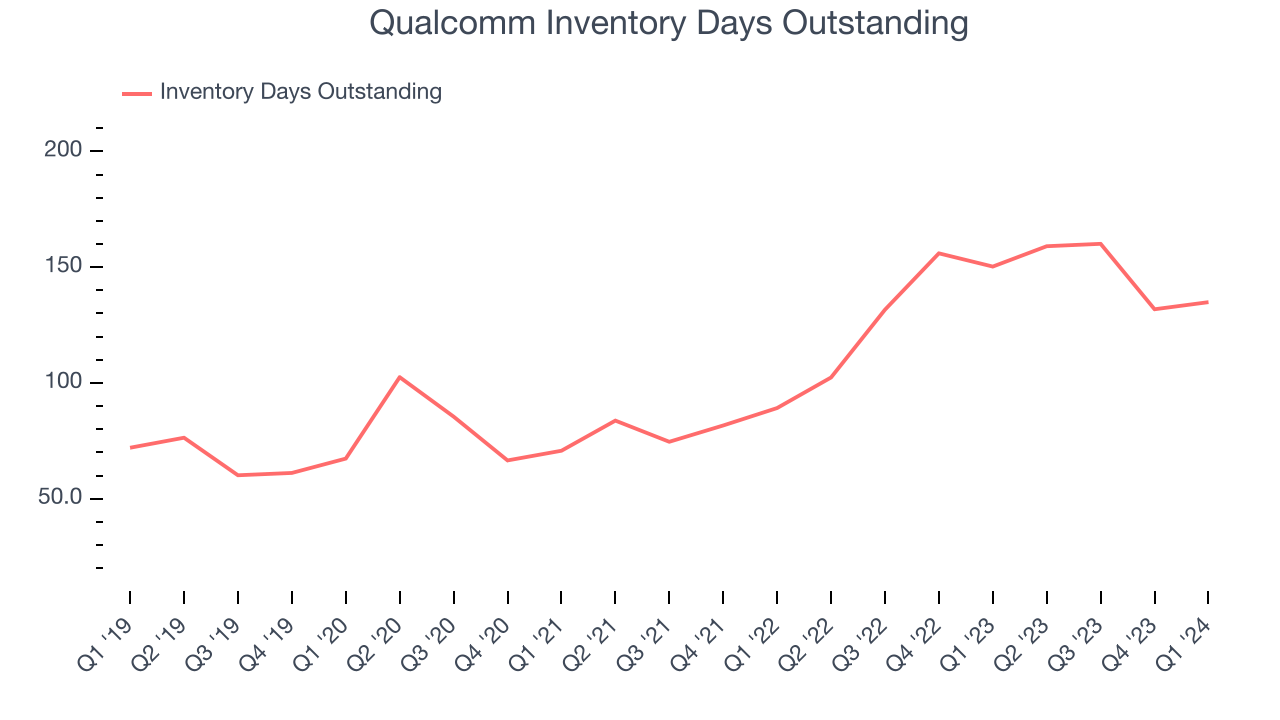

- Inventory Days Outstanding: 135, up from 132 in the previous quarter

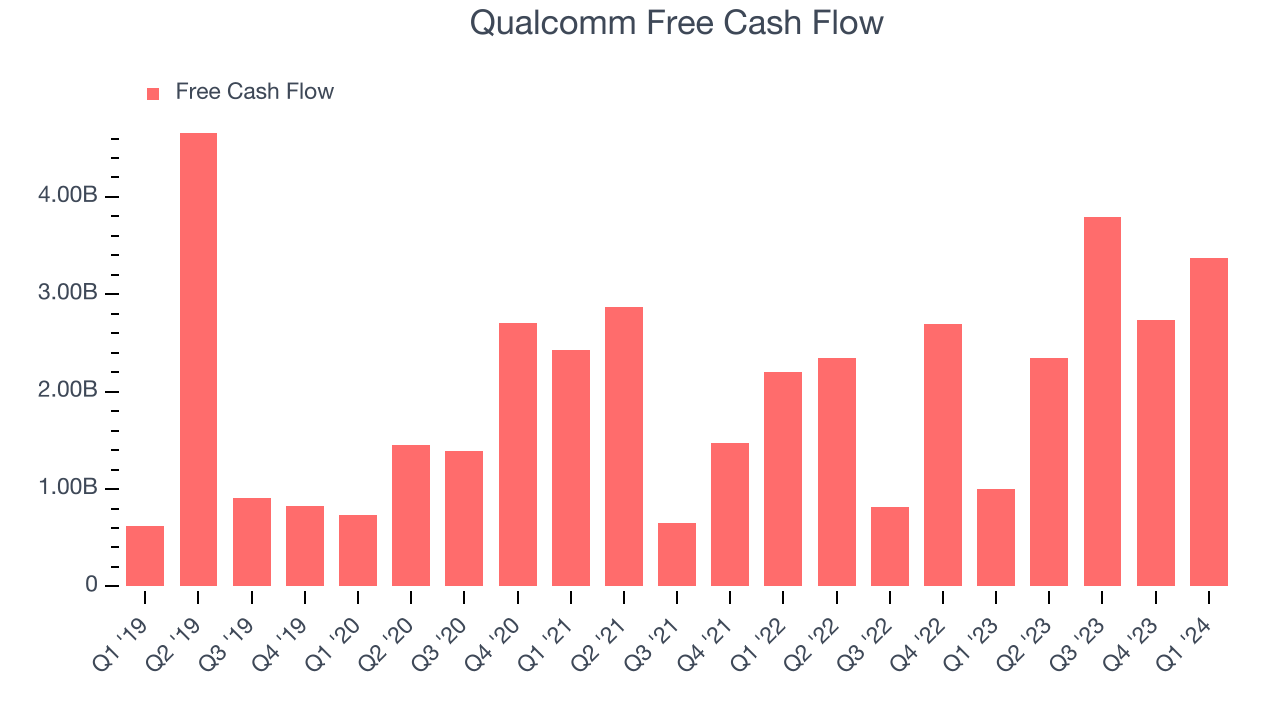

- Free Cash Flow of $3.37 billion, up 23.2% from the previous quarter

- Market Capitalization: $185.2 billion

Having been at the forefront of developing the standards for cellular connectivity for over four decades, Qualcomm (NASDAQ:QCOM) is a leading innovator and a fabless manufacturer of wireless technology chips used in smartphones, autos and internet of things appliances.

Qualcomm has one of the more unique semiconductor business models. Its research has created the intellectual property that is the foundation for the global wireless industry. In the 1990s they developed the original code division multiple access (CDMA) technology that became the standard for cell phone networks first in the US, then around the world. Qualcomm has had a hand in developing Wi-Fi, GPS, and Bluetooth, along with RFID (Radio Frequency ID), and 4G and 5G technology.

It monetizes its portfolio of more than 140,000 patents through designing semiconductors used in handsets, autos, and IoT and also through licensing its patents for others to incorporate in their own products. Qualcomm outsources manufacturing of its chips, its main product family is the Snapdragon chip, an all in one chip used to power mobile devices: it includes a cellular modem, integrated Wi-Fi, Bluetooth, and GPS, along with a CPU (central processing unit) and GPU (graphics processing unit). Different versions of Snapdragon are used in different types of devices (tablets, laptops, handsets) based on the different battery life or processing requirements.

Qualcomm’s stranglehold on wireless’s foundational technology has enmeshed it in disputes over royalty payments, which are highly consequential to Qualcomm’s business model as it receives a royalty of roughly 5% of the average price of every smartphone sold, and those licensing revenues are nearly pure profit. In 2017, Apple refused to continue paying the royalty which degenerated into a lawsuit with Apple switching to Intel modem chips, only to return to Qualcomm in 2019, when Intel decided not to make 5G modems. Qualcomm also ran into similar disputes with Chinese handset makers such as Huawei in the past few years, all of which have since been resolved, with Qualcomm continuing to receive its royalty payments. Because of its unique position in the semiconductor world, Qualcomm became a geopolitical football during China-US trade tensions over the past few years: China blocked Qualcomm’s attempted acquisition of NXPI over antitrust concerns, while the US blocked Broadcom proposed hostile takeover of Qualcomm over national security concerns.

Qualcomms peers and competitors include AMD (NASDAQ:AMD), Broadcom (NASDAQ:AVGO), Intel (NASDAQ:INTC), MediaTek (TWSE:2454), NXP Semiconductors NV (NASDAQ:NXPI), Nvidia (NASDAQ: NVDA), and Samsung (KOSI:005930).Processors and Graphics Chips

Chips need to keep getting smaller in order to advance on Moore’s law, and that is proving increasingly more complicated and expensive to achieve with time. That has caused most digital chip makers to become “fabless” designers, rather than manufacturers, instead relying on contracted foundries like TSMC to manufacture their designs. This has benefitted the digital chip makers’ free cash flow margins, as exiting the manufacturing business has removed large cash expenses from their business models.

Sales Growth

Qualcomm's revenue growth over the last three years has been mediocre, averaging 14% annually. As you can see below, this was a weaker quarter for the company, with revenue growing from $9.28 billion in the same quarter last year to $9.39 billion. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

This was a sluggish quarter for the company as its revenue grew 1.2% year on year, in line with analysts' estimates. Despite these results, we believe Qualcomm is still in the early days of an upcycle, as this was just the second consecutive quarter of growth and a typical upcycle tends to last 8-10 quarters.

Qualcomm's management team believes its revenue growth will accelerate, guiding to 8.9% year-on-year growth next quarter. Wall Street expects the company to grow its revenue by 9.4% over the next 12 months.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Qualcomm's DIO came in at 135, which is 33 days above its five-year average, suggesting that the company's inventory has grown to higher levels than we've seen in the past.

Pricing Power

In the semiconductor industry, a company's gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor. Qualcomm's gross profit margin, which shows how much money the company gets to keep after paying key materials, input, and manufacturing costs, came in at 56.3% in Q1, up 1 percentage points year on year.

Despite declining over the last 12 months, Qualcomm still retains reasonably high gross margins, averaging 55.8%. These margins point to its solid competitive offering, disciplined cost controls, and lack of significant pricing pressure.

Profitability

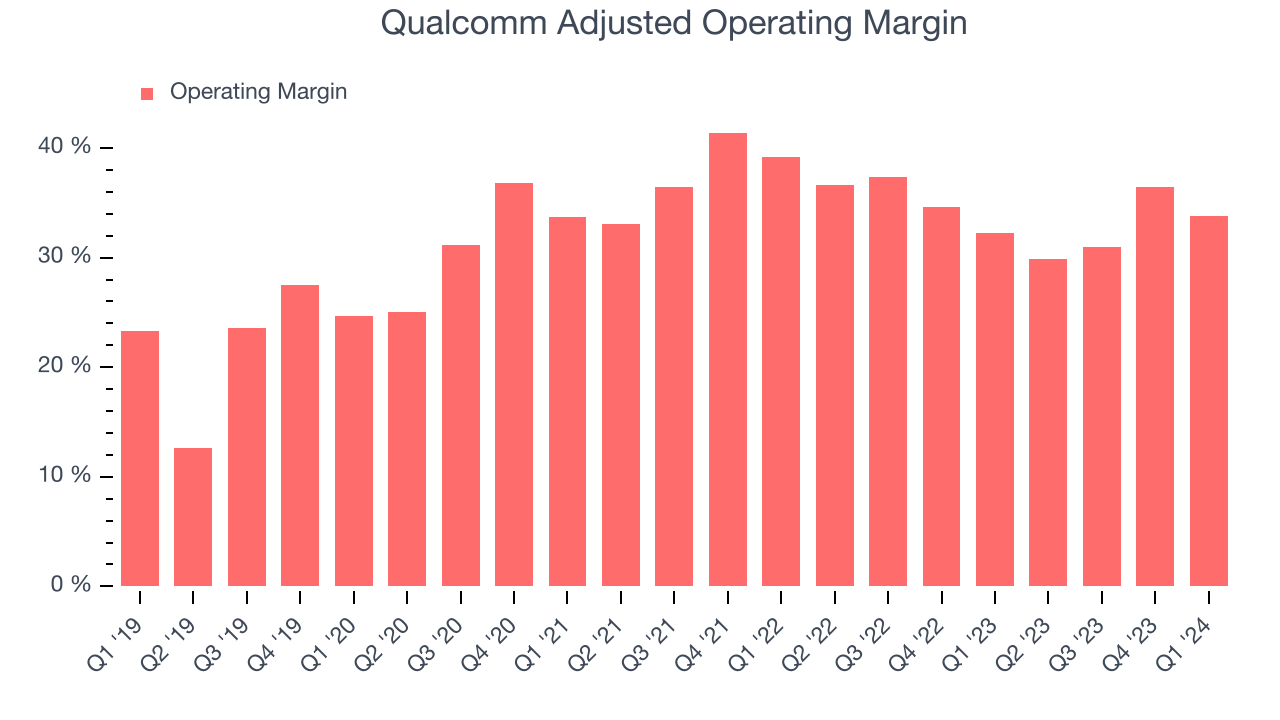

Qualcomm reported an operating margin of 33.8% in Q1, up 1.5 percentage points year on year. Operating margins are one of the best measures of profitability because they tell us how much money a company takes home after manufacturing its products, marketing and selling them, and, importantly, keeping them relevant through research and development.

Qualcomm's operating margins have been trending down over the last year, averaging 32.9%. However, the company's profitability is still above average for semiconductor companies, driven by an efficient cost structure.

Earnings, Cash & Competitive Moat

Analysts covering Qualcomm expect earnings per share to grow 12.6% over the next 12 months, although estimates will likely change after earnings.

Although earnings are important, we believe cash is king because you can't use accounting profits to pay the bills. Qualcomm's free cash flow came in at $3.37 billion in Q1, up 236% year on year.

As you can see above, Qualcomm produced $12.25 billion in free cash flow over the last 12 months, an eye-popping 33.7% of revenue. This is a great result; Qualcomm's free cash flow conversion places it among the best semiconductor companies and, if sustainable, puts the company in an advantageous position to invest in new products while remaining resilient during industry downturns.

Return on Invested Capital (ROIC)

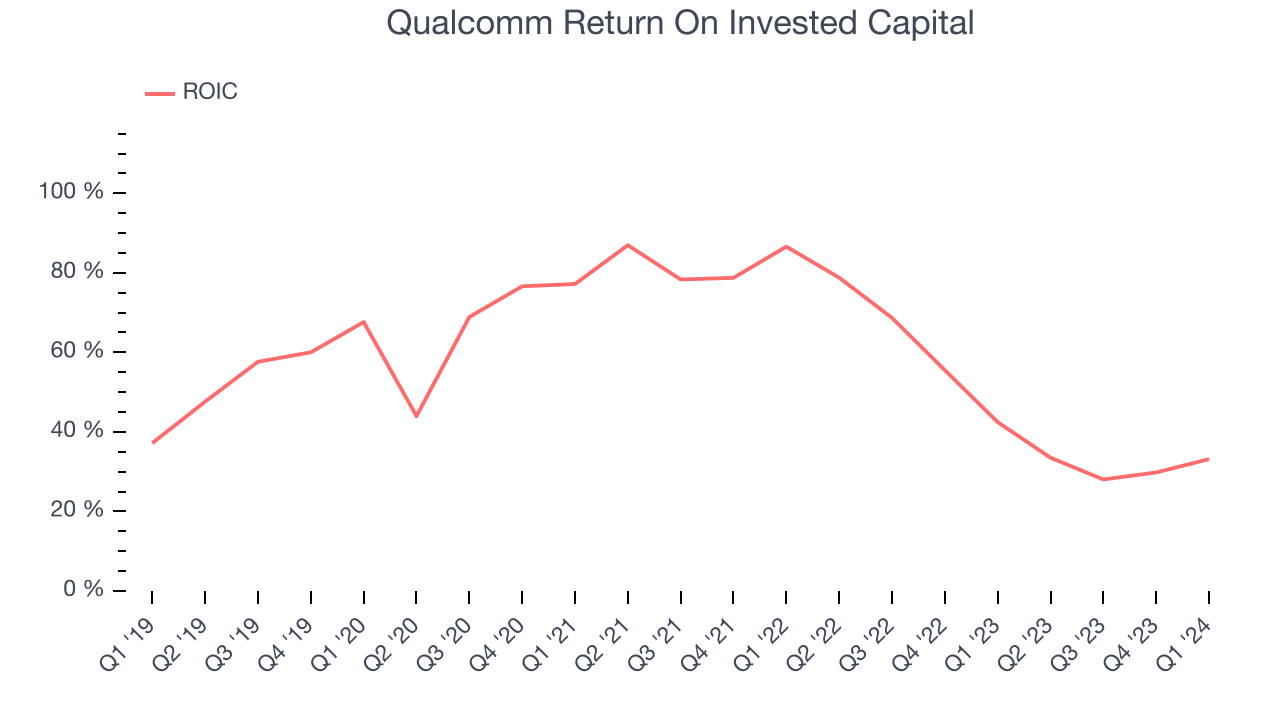

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Qualcomm's five-year average ROIC was 61.4%, placing it among the best semiconductor companies. Just as you’d like your investment dollars to generate returns, Qualcomm's invested capital has produced excellent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Qualcomm's ROIC significantly decreased over the last few years. The company has historically shown the ability to generate good returns, but they have gone the wrong way recently, making us a bit conscious.

Key Takeaways from Qualcomm's Q1 Results

We enjoyed seeing Qualcomm exceed analysts' EPS expectations this quarter. We were also glad next quarter's revenue guidance came in higher than Wall Street's estimates. On the other hand, its inventory levels increased. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 5.3% after reporting and currently trades at $172.97 per share.

Is Now The Time?

When considering an investment in Qualcomm, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

There are several reasons why we think Qualcomm is a great business. Although its revenue growth has been mediocre over the last three years with analysts expecting growth to slow from here, its powerful free cash generation enables it to sustainably invest in growth initiatives while maintaining an ample cash cushion. On top of that, its stellar ROIC suggests it has been a well-run company historically.

Qualcomm's price-to-earnings ratio based on the next 12 months is 16.2x. Looking at the semiconductors landscape today, Qualcomm's qualities really stand out, and we really like it at this price.

Wall Street analysts covering the company had a one-year price target of $175.24 per share right before these results (compared to the current share price of $172.97).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.