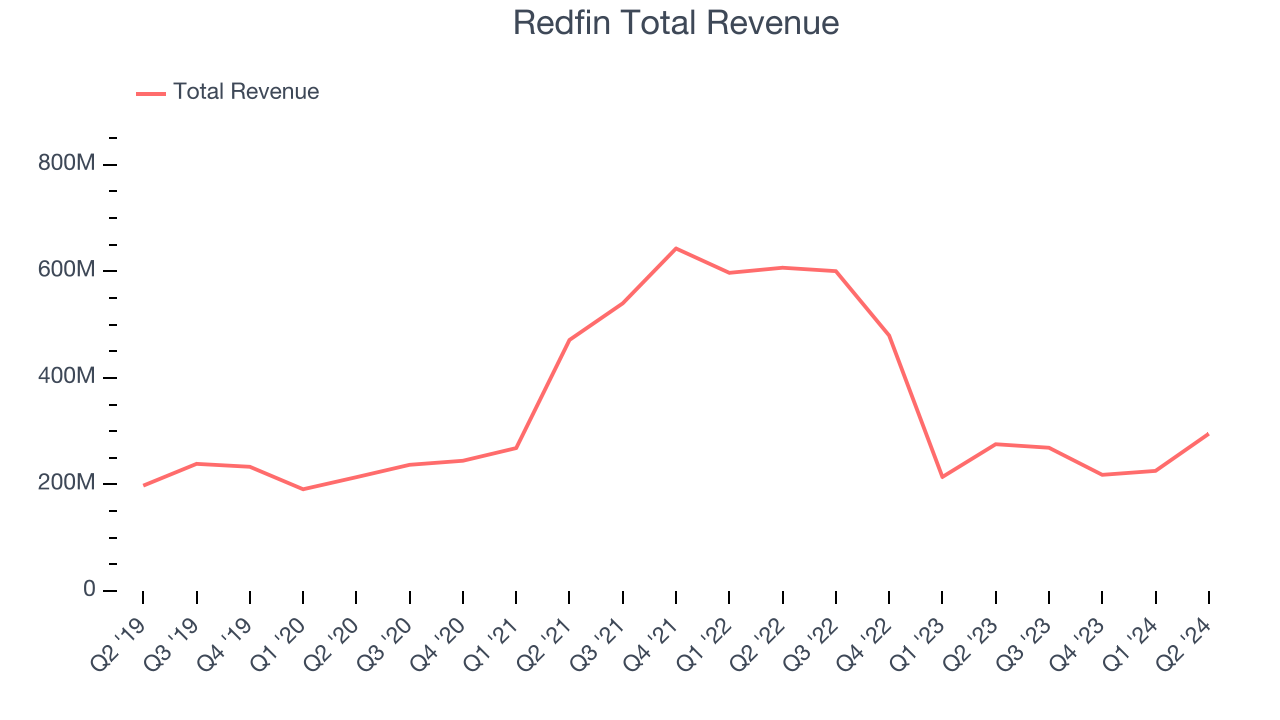

Real estate technology company Redfin (NASDAQ:RDFN) reported results ahead of analysts' expectations in Q2 CY2024, with revenue up 7.1% year on year to $295.2 million. On the other hand, next quarter's revenue guidance of $279 million was less impressive, coming in 5.7% below analysts' estimates. It made a GAAP loss of $0.23 per share, improving from its loss of $0.24 per share in the same quarter last year.

Is now the time to buy Redfin? Find out by accessing our full research report, it's free.

Redfin (RDFN) Q2 CY2024 Highlights:

- Revenue: $295.2 million vs analyst estimates of $291.6 million (1.2% beat)

- EPS: -$0.23 vs analyst estimates of -$0.26 (12.4% beat)

- Revenue Guidance for Q3 CY2024 is $279 million at the midpoint, below analyst estimates of $295.7 million

- Gross Margin (GAAP): 37.1%, up from 36.4% in the same quarter last year

- Adjusted EBITDA Margin: 0%, up from -2.5% in the same quarter last year

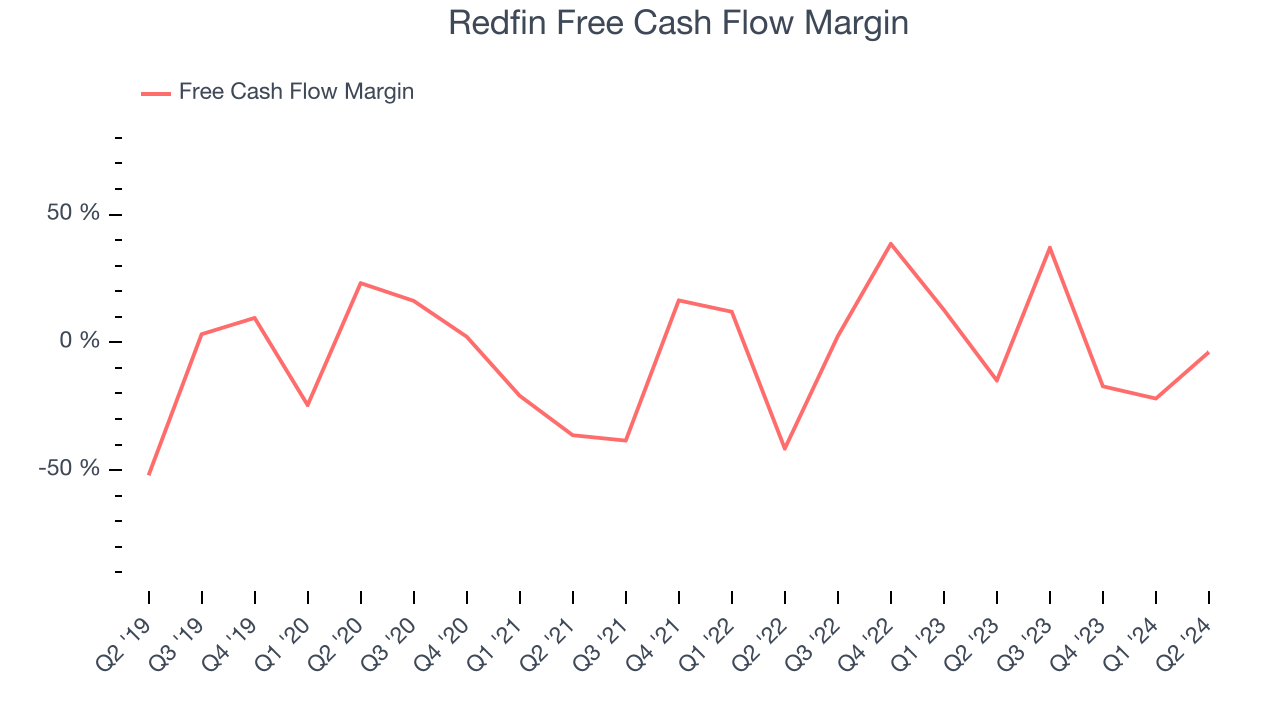

- Free Cash Flow was -$11.19 million compared to -$49.54 million in the previous quarter

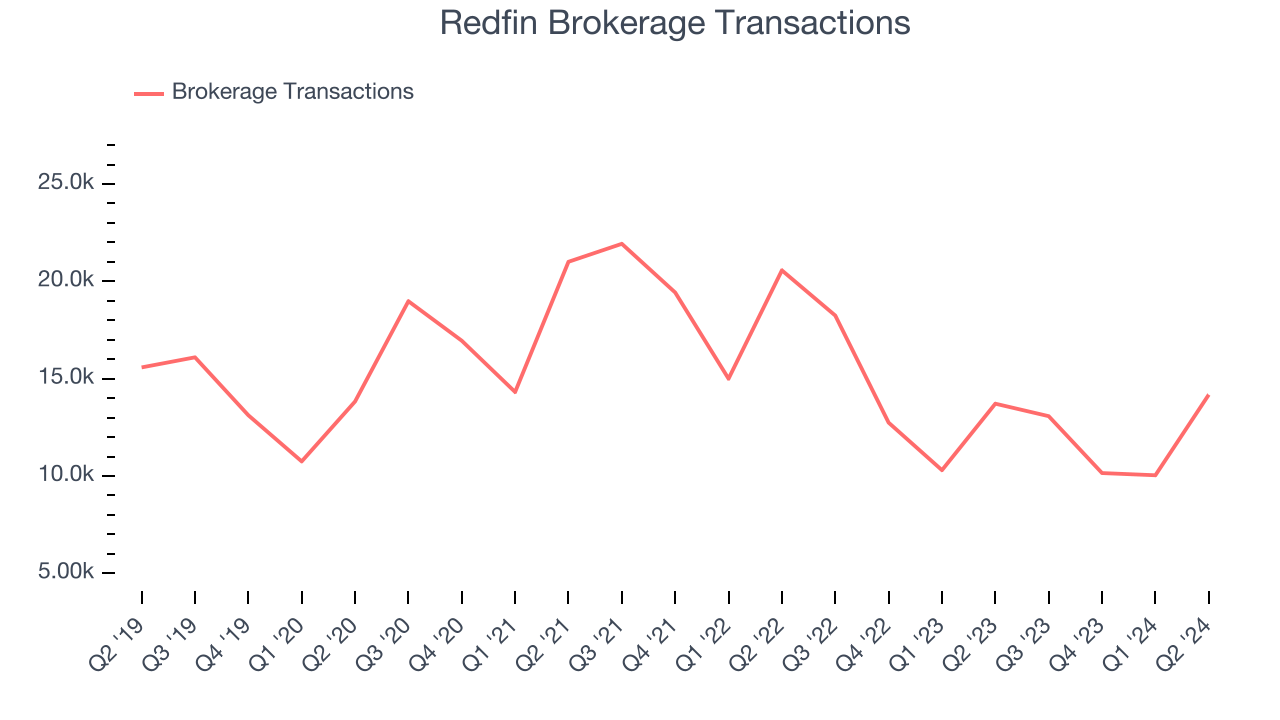

- Brokerage Transactions: 14,178, up 462 year on year

- Market Capitalization: $870.9 million

“In a still-declining market, Redfin grew revenues, profits and market share,” said Redfin CEO Glenn Kelman.

Founded by a former medical school student, electrical engineer, and Amazon data engineer, Redfin (NASDAQ:RDFN) is a real estate company offering brokerage services through an online platform.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Regrettably, Redfin's sales grew at a weak 12% compounded annual growth rate over the last five years. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Redfin's history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 35% annually.

We can better understand the company's revenue dynamics by analyzing its number of brokerage transactions and partner transactions, which clocked in at 14,178 and 3,395 in the latest quarter. Over the last two years, Redfin's brokerage transactions averaged 20.5% year-on-year declines while its partner transactions averaged 7.9% year-on-year declines.

This quarter, Redfin reported solid year-on-year revenue growth of 7.1%, and its $295.2 million of revenue outperformed Wall Street's estimates by 1.2%. The company is guiding for revenue to rise 3.7% year on year to $279 million next quarter, improving from the 55.2% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 11.9% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Redfin has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.3%, subpar for a consumer discretionary business.

Redfin burned through $11.19 million of cash in Q2, equivalent to a negative 3.8% margin. The company's cash burn decreased meaningfully year on year but still deviates from its longer-term margin, raising some eyebrows.

Key Takeaways from Redfin's Q2 Results

It was good to see Redfin beat analysts' revenue and EPS expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its number of brokerage transactions fell short of Wall Street's estimates. Overall, this was a bad quarter for Redfin. The stock traded down 3.5% to $6.80 immediately following the results.

Redfin may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.