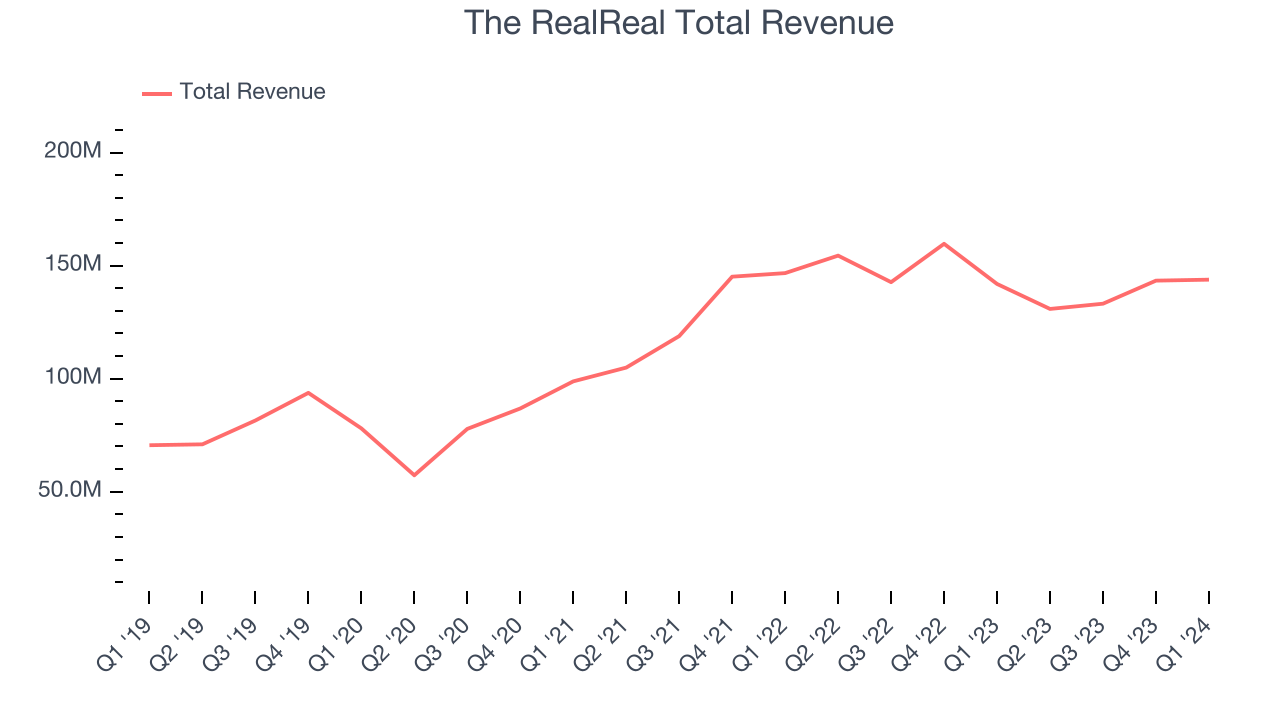

Secondhand luxury marketplace The RealReal (NASDAQ: REAL) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 1.3% year on year to $143.8 million. The company expects next quarter's revenue to be around $140 million, in line with analysts' estimates. It made a non-GAAP loss of $0.12 per share, improving from its loss of $0.83 per share in the same quarter last year.

The RealReal (REAL) Q1 CY2024 Highlights:

- Revenue: $143.8 million vs analyst estimates of $139.2 million (3.3% beat)

- EPS (non-GAAP): -$0.12 vs analyst estimates of -$0.15 ($0.03 beat)

- Revenue Guidance for Q2 CY2024 is $140 million at the midpoint, roughly in line with what analysts were expecting (adjusted EBITDA guidance for Q2 is better than expectations)

- The company reconfirmed its revenue guidance for the full year of $592.5 million at the midpoint

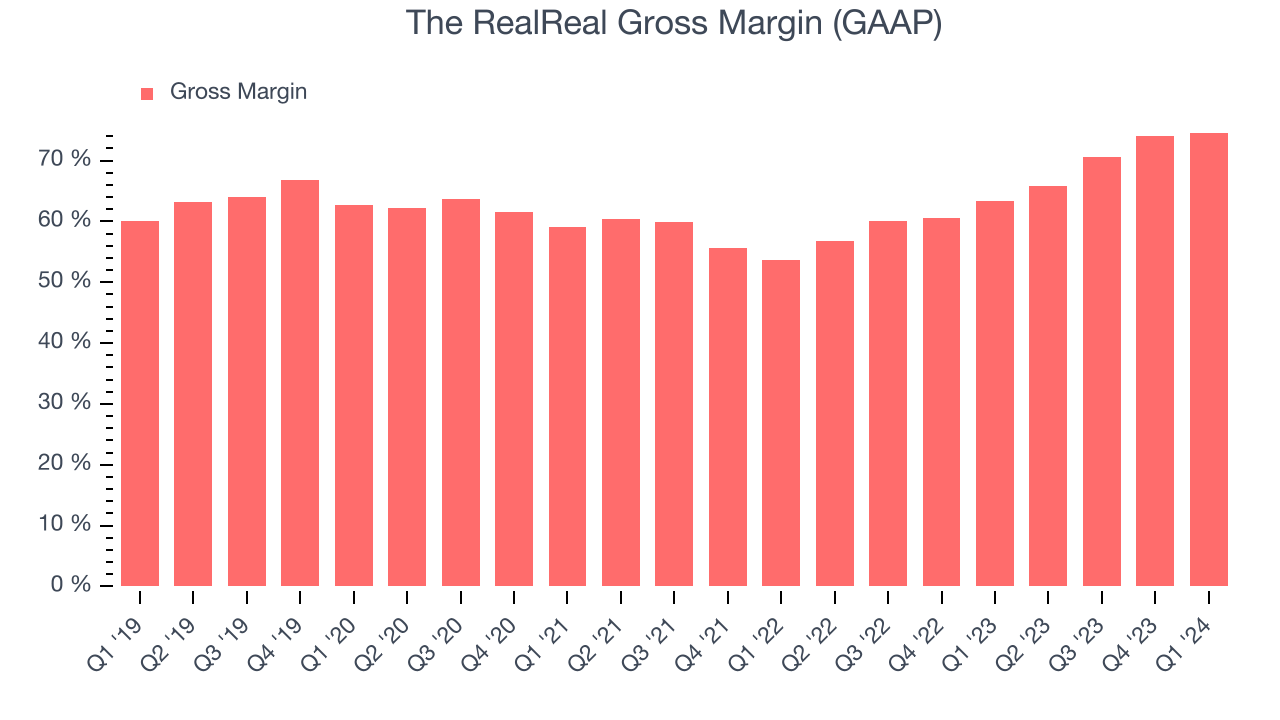

- Gross Margin (GAAP): 74.6%, up from 63.4% in the same quarter last year

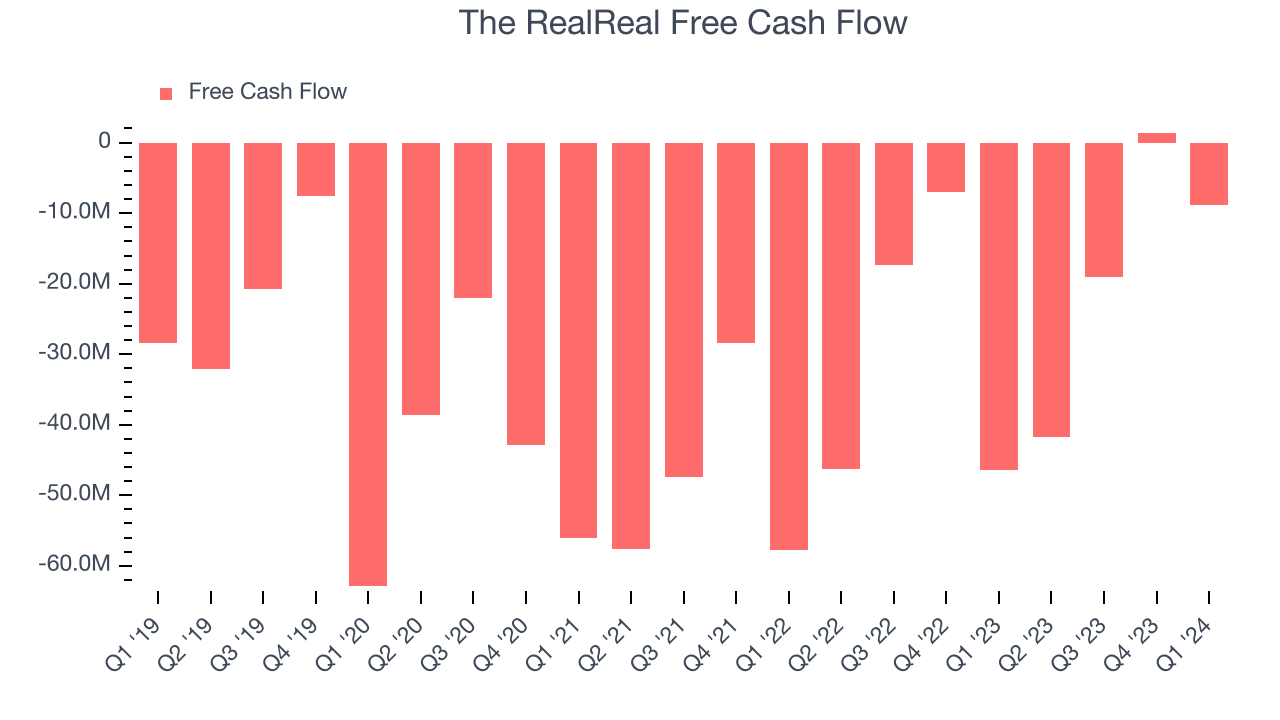

- Free Cash Flow was -$8.79 million, down from $1.45 million in the previous quarter

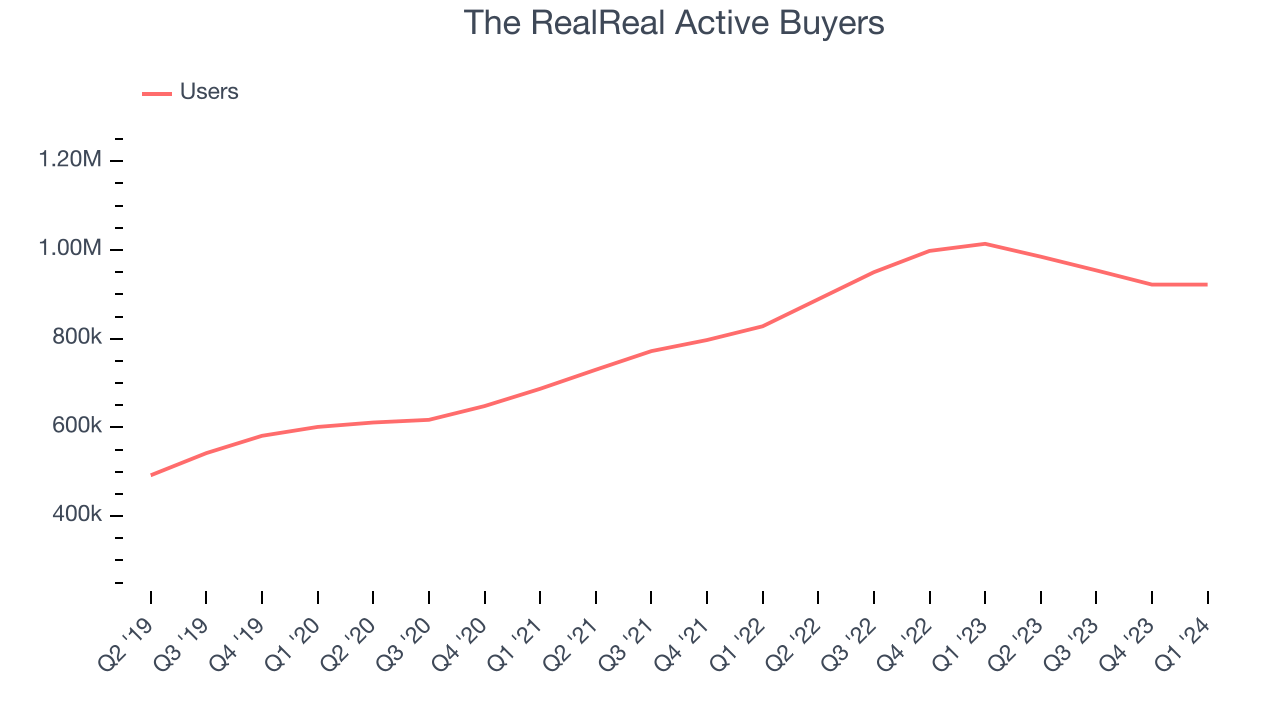

- Active Buyers : 922,000, down 92,000 year on year

- Market Capitalization: $440.8 million

Founded by consignment store aficionado Julie Wainwright, The RealReal (NASDAQ: REAL) is an online marketplace for buying and selling secondhand luxury goods.

The RealReal provides an online marketplace for consignment luxury goods with its key differentiation being that it authenticates each item sold on its platform, reducing risk for buyers of expensive secondhand goods, while also enabling it to provide fulfillment services. The top selling categories are men’s and women’s apparel, watches and jewelry, and home and art. Its authentication differentiation has enabled The RealReal to grow an audience of buyers, which in turn has attracted high net worth individuals willing to sell their used goods. The key differentiation on the seller side is that The RealReal has reduced the friction of selling by taking care of packaging, shipping, listing and photos.

This intermediary model is more expensive to operate than a traditional marketplace, which tends to be asset lite, merely connecting buyers and sellers, but necessary to unlock a previously latent supply of merchandise that was relegated to brick and mortar consignment shops. As a result, The RealReal charges one of the highest take rates (commissions) in online commerce.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

The RealReal (NASDAQ:REAL) competes with Poshmark (NASDAQ: POSH), ThredUp (NASDAQ: TDUP) and Revolve Group (NYSE: RVLV).

Sales Growth

The RealReal's revenue growth over the last three years has been strong, averaging 24.6% annually. This quarter, The RealReal beat analysts' estimates but reported lacklustre 1.3% year-on-year revenue growth.

Guidance for the next quarter indicates The RealReal is expecting revenue to grow 7% year on year to $140 million, improving from the 15.3% year-on-year decline it recorded in the comparable quarter last year. Ahead of the earnings results, analysts were projecting sales to grow 9.6% over the next 12 months.

Usage Growth

As an online marketplace, The RealReal generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, The RealReal's users, a key performance metric for the company, grew 10.9% annually to 922,000. This is decent growth for a consumer internet company.

Unfortunately, The RealReal's users decreased by 92,000 in Q1, a 9.1% drop since last year.

Revenue Per User

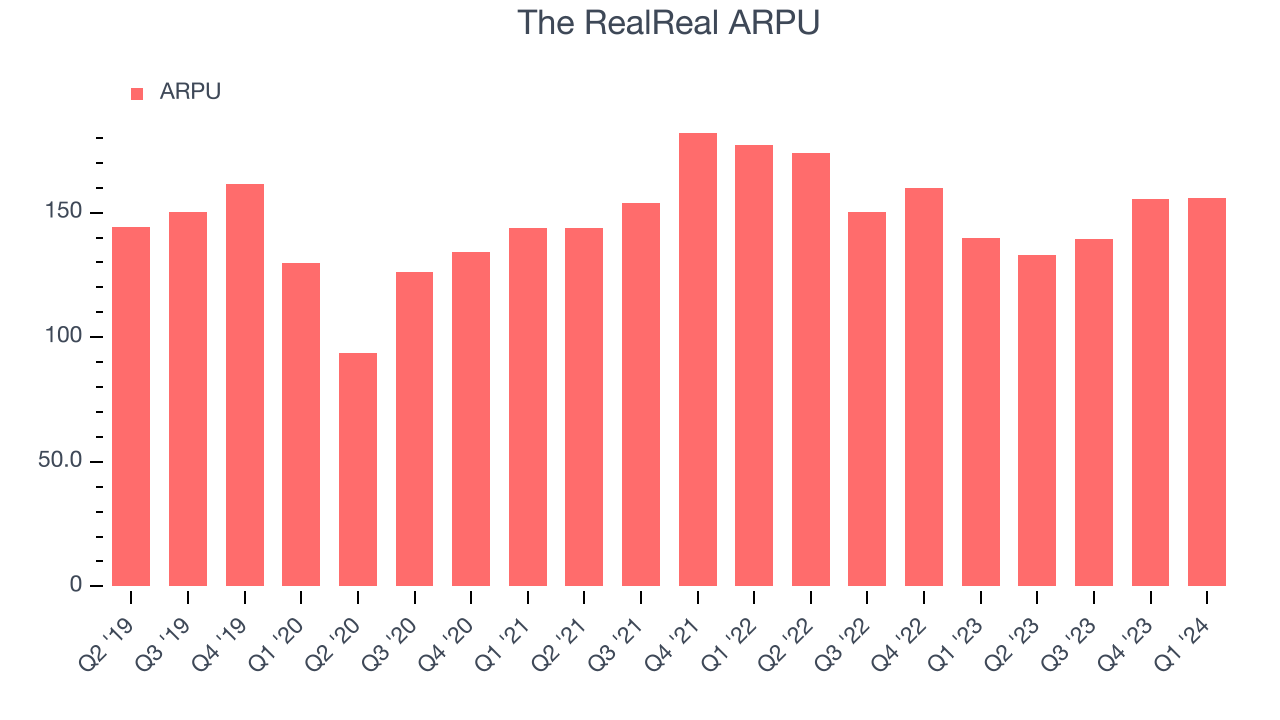

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like The RealReal because it measures how much the company earns in transaction fees from each user. Furthermore, ARPU gives us unique insights as it's a function of a user's average order size and The RealReal's take rate, or "cut", on each order.

The RealReal's ARPU has declined over the last two years, averaging 4.6%. Although the company's users have continued to grow, it's lost its pricing power and will have to make improvements soon. This quarter, ARPU grew 11.4% year on year to $155.97 per user.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor.

The RealReal's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 74.6% this quarter, up 11.2 percentage points year on year.

For online marketplaces like The RealReal, these aforementioned costs typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification. After paying for these expenses, The RealReal had $0.75 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

Over the past year, The RealReal has seen its already strong gross margins rise, averaging 71.4%. These robust unit economics, driven by the company's lucrative business model and strong pricing power, are higher than its peers and allow The RealReal to make more investments in product and marketing.

User Acquisition Efficiency

Unlike enterprise software that's typically sold by dedicated sales teams, consumer internet businesses like The RealReal grow from a combination of product virality, paid advertisement, and incentives.

The RealReal is extremely efficient at acquiring new users, spending only 14.4% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and customer acquisition advantages from scale, giving The RealReal the freedom to invest its resources into new growth initiatives while maintaining optionality.

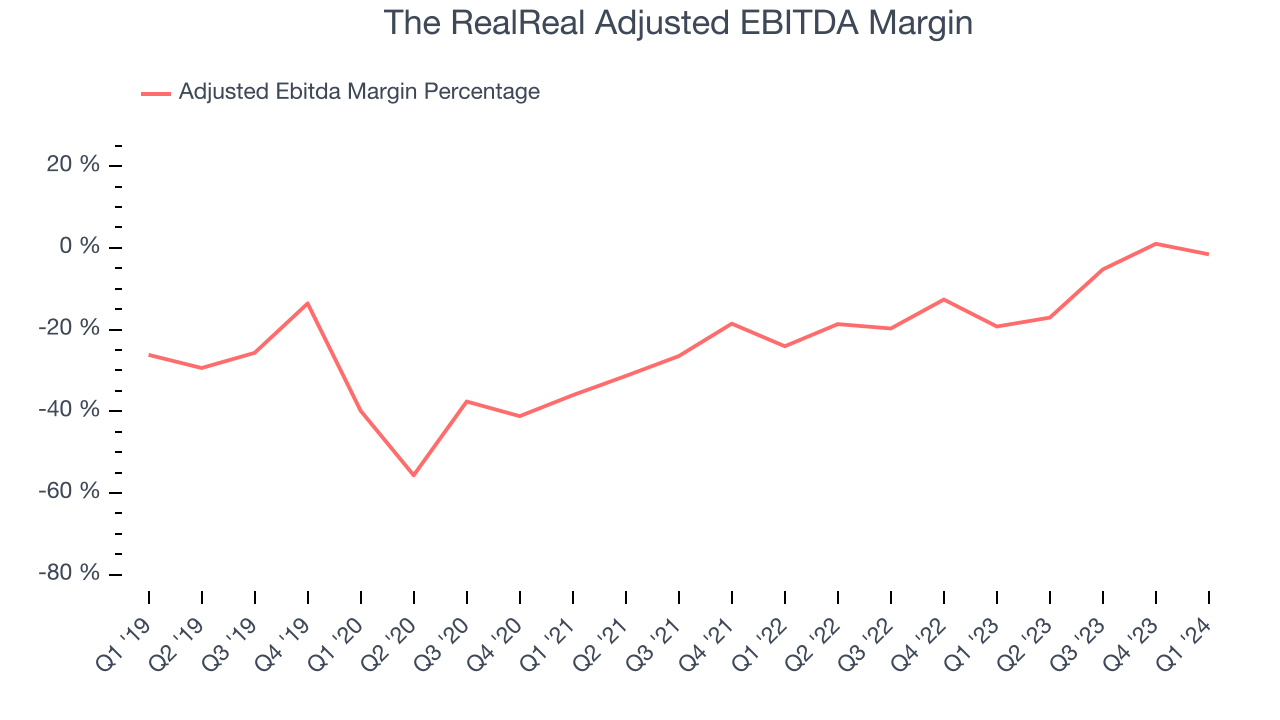

Profitability & Free Cash Flow

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

This quarter, The RealReal's EBITDA came in at negative $2.26 million, resulting in a negative 1.6% margin. The company's performance has been rather mediocre for a consumer internet business over the last four quarters, with average EBITDA margins of negative 5.5%.

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. The RealReal burned through $8.79 million in Q1, increasing the cash burn by 81% year on year.

The RealReal has burned through $68.18 million of cash over the last 12 months, resulting in an uninspiring negative 12.4% free cash flow margin. This low FCF margin stems from The RealReal's capital-intensive business model and desire to stay competitive.

Key Takeaways from The RealReal's Q1 Results

It was great to see The RealReal beat analysts' revenue expectations this quarter. We were also glad next quarter's revenue and adjusted EBITDA guidance both came in higher than Wall Street's estimates. On the other hand, its number of users declined and its revenue growth was quite weak. Overall, this was a mediocre quarter for The RealReal. The stock is up 3.3% after reporting and currently trades at $3.9 per share.

Is Now The Time?

The RealReal may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Although The RealReal isn't a bad business, it probably wouldn't be one of our picks. Although its revenue growth has been good over the last three years, Wall Street expects growth to deteriorate from here. And while its user acquisition efficiency is best in class, the downside is its ARPU has declined over the last two years. On top of that, its cash burn raises the question if it can sustainably maintain its growth.

The RealReal's price/gross profit ratio based on the next 12 months is 0.9x. In the end, beauty is in the eye of the beholder. While The RealReal wouldn't be our first pick, if you like the business, the shares are trading at a pretty interesting price right now.

Wall Street analysts covering the company had a one-year price target of $3.39 per share right before these results (compared to the current share price of $3.90).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.