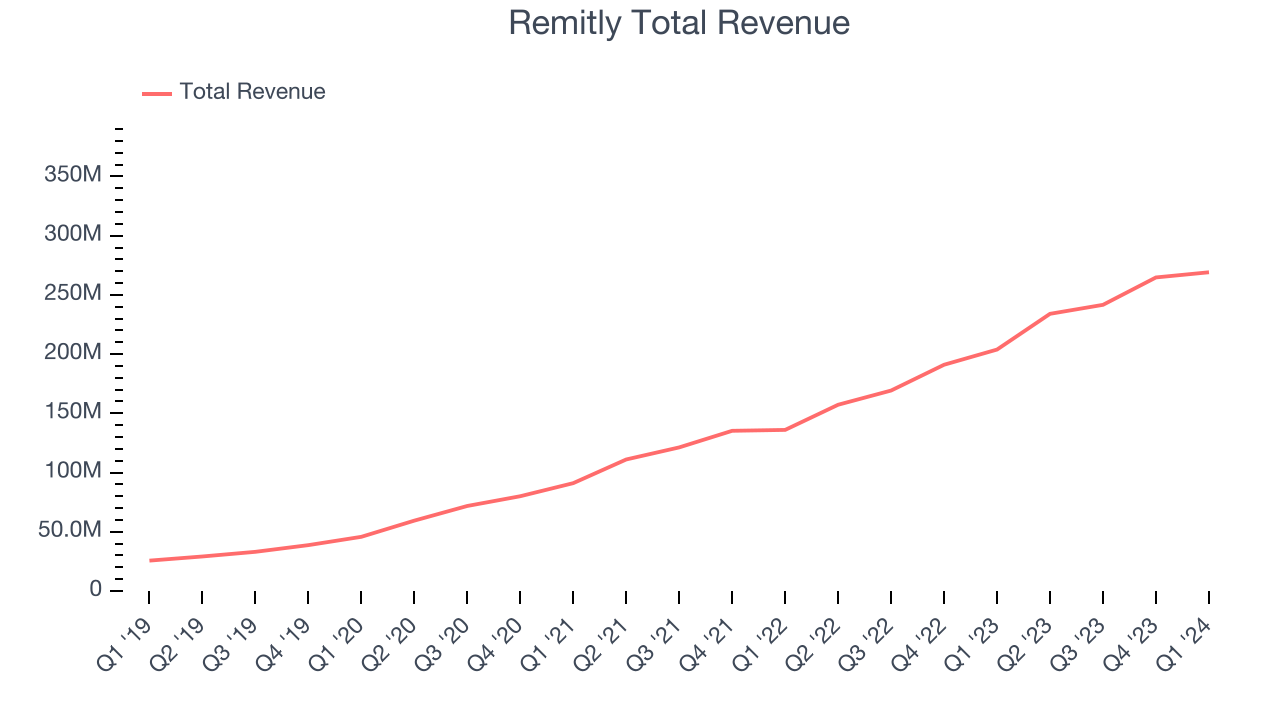

Online money transfer platform Remitly (NASDAQ:RELY) missed analysts' expectations in Q1 CY2024, with revenue up 32% year on year to $269.1 million. On the other hand, the company's outlook for the full year was close to analysts' estimates with revenue guided to $1.24 billion at the midpoint. It made a GAAP loss of $0.11 per share, improving from its loss of $0.16 per share in the same quarter last year.

Remitly (RELY) Q1 CY2024 Highlights:

- Revenue: $269.1 million vs analyst estimates of $273.9 million (1.7% miss)

- EPS: -$0.11 vs analyst estimates of -$0.15 (25.2% beat)

- The company reconfirmed its revenue guidance for the full year of $1.24 billion at the midpoint

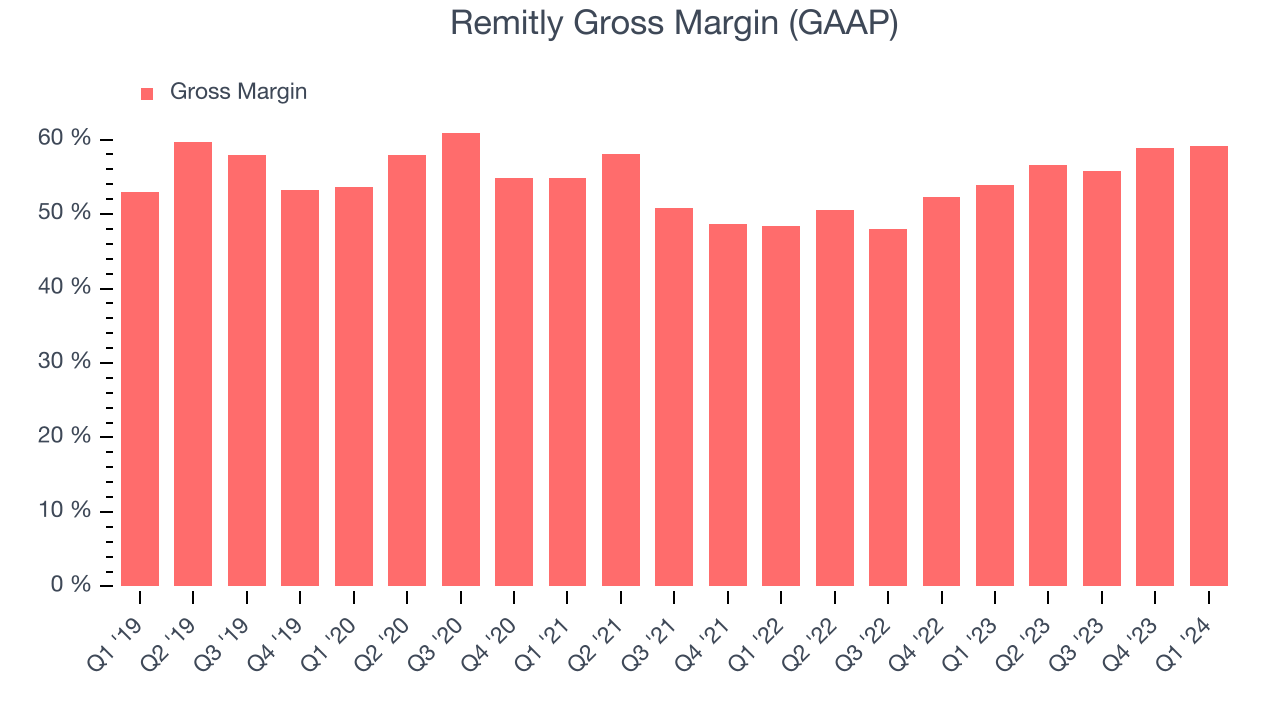

- Gross Margin (GAAP): 59.1%, up from 53.9% in the same quarter last year

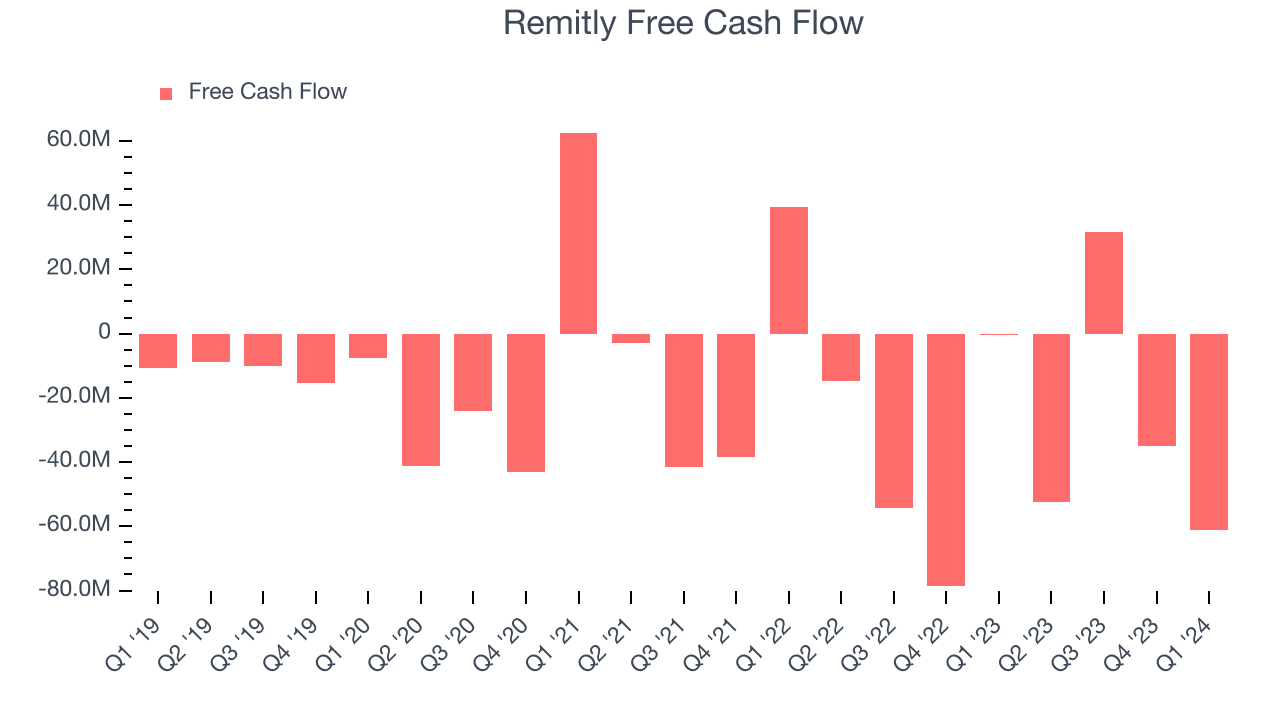

- Free Cash Flow was -$61.12 million compared to -$35.06 million in the previous quarter

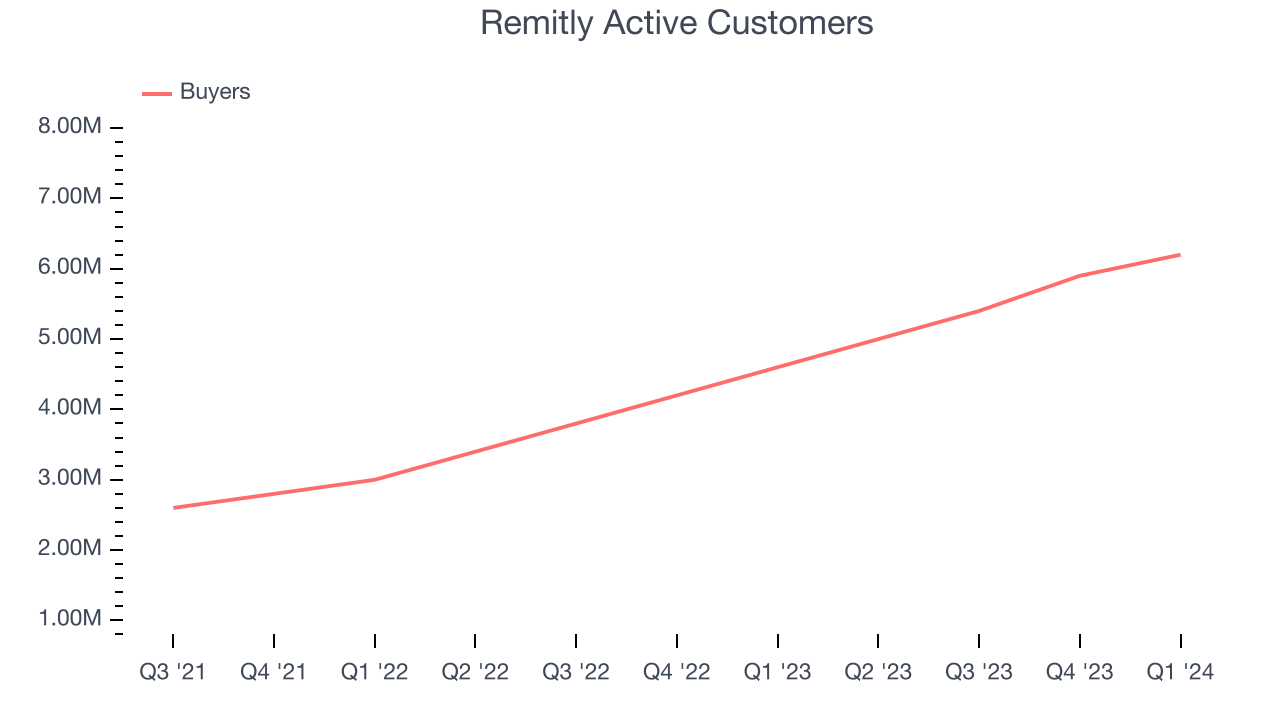

- Active Customers: 6.2 million, up 1.6 million year on year

- Market Capitalization: $3.43 billion

With Amazon founder Jeff Bezos as an early investor, Remitly (NASDAQ:RELY) is an online platform that enables consumers to safely and quickly send money globally.

The company is based in Seattle and was founded in 2011 and went public about a decade later. The product aims to give people access to financial services, especially those who are underserved by traditional banking systems.

The problem that Remitly solves is the difficulty and sometimes high cost of sending money overseas. Traditionally, people have relied on money transfer services that charge high fees and take several days to process. Remitly's platform offers a faster, more affordable option. The company's key customers tend to be people who need to send money to family and friends in other countries.

Remitly generates revenue through transaction fees, which vary depending on the amount and destination of the transfer. For example, if someone in the United States wants to send $500 to a family member in Mexico, Remitly might charge a fee of $3.99 for an economy transfer or $9.99 for an express transfer, which would arrive within minutes. Countries such as Vietnam may have higher fees. The company also makes money by offering different exchange rates for different currencies. By optimizing the exchange rate, Remitly can earn a margin on each transaction.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors offering online legal or document services include Western Union (NYSE:WU), Moneygram (NASDAQ:MGI), and private company WorldRemit.Sales Growth

Remitly's revenue growth over the last three years has been exceptional, averaging 50.7% annually. This quarter, Remitly reported solid 32% year-on-year revenue growth but fell short of Wall Street's expectations.

Ahead of the earnings results, analysts were projecting sales to grow 30.8% over the next 12 months.

Usage Growth

As an online marketplace, Remitly generates revenue growth by increasing both the number of buyers on its platform and the average order size in dollars.

Over the last two years, Remitly's active buyers, a key performance metric for the company, grew 44.8% annually to 6.2 million. This is among the fastest growth rates of any consumer internet company, indicating that users are excited about its offerings.

In Q1, Remitly added 1.6 million active buyers, translating into 34.8% year-on-year growth.

Revenue Per Buyer

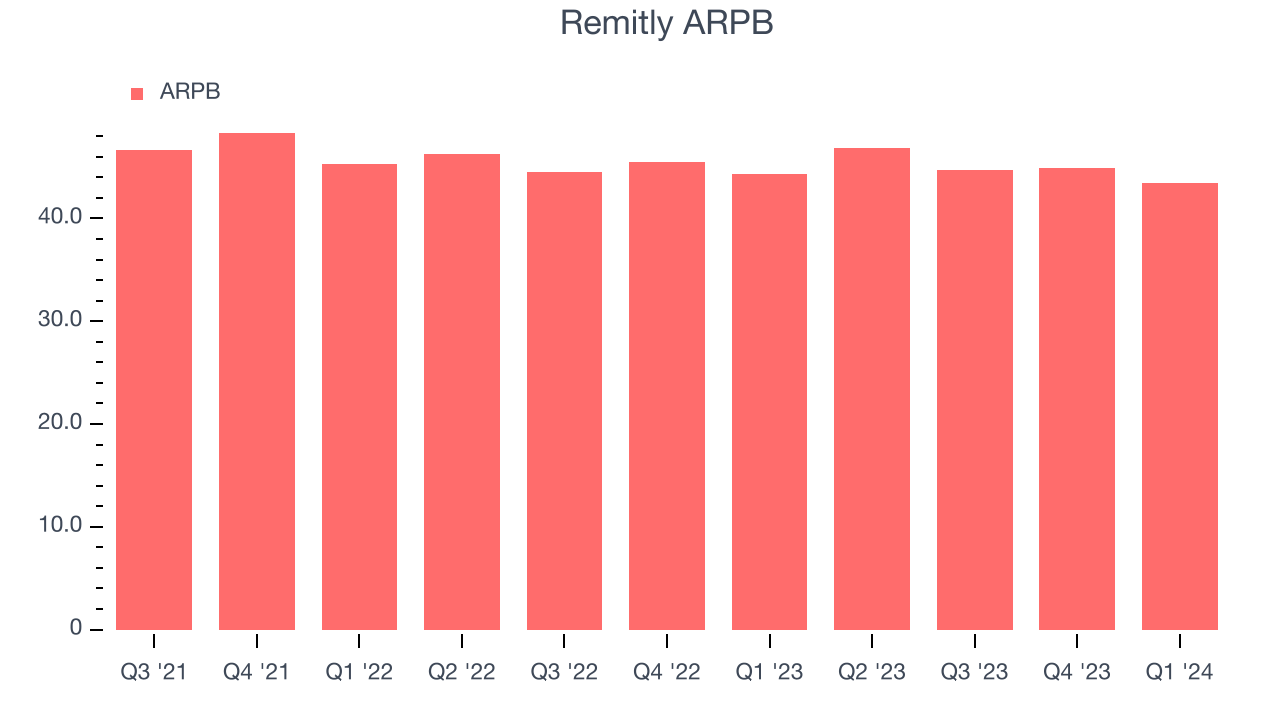

Average revenue per buyer (ARPB) is a critical metric to track for consumer internet businesses like Remitly because it measures how much the company earns in transaction fees from each buyer. Furthermore, ARPB gives us unique insights as it's a function of a user's average order size and Remitly's take rate, or "cut", on each order.

Remitly's ARPB has declined over the last two years, averaging 2%. Although it's unfortunate to see the company lose its pricing power, it was still able to achieve strong buyer growth. This quarter, ARPB declined 2.1% year on year to $43.41 per buyer.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor.

Remitly's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 59.1% this quarter, up 5.2 percentage points year on year.

For online marketplaces like Remitly, these aforementioned costs typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification. After paying for these expenses, Remitly had $0.59 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

Remitly's gross margins have been trending up over the last year, averaging 57.6%. These margins are around that of a typical consumer internet business, but Remitly's rising margins may indicate improving pricing power or scale advantages over costs.

User Acquisition Efficiency

Unlike enterprise software that's typically sold by dedicated sales teams, consumer internet businesses like Remitly grow from a combination of product virality, paid advertisement, and incentives.

Remitly is efficient at acquiring new users, spending 44.3% of its gross profit on sales and marketing expenses over the last year. This level of efficiency indicates relatively solid competitive positioning, giving Remitly the freedom to invest its resources into new growth initiatives.

Profitability & Free Cash Flow

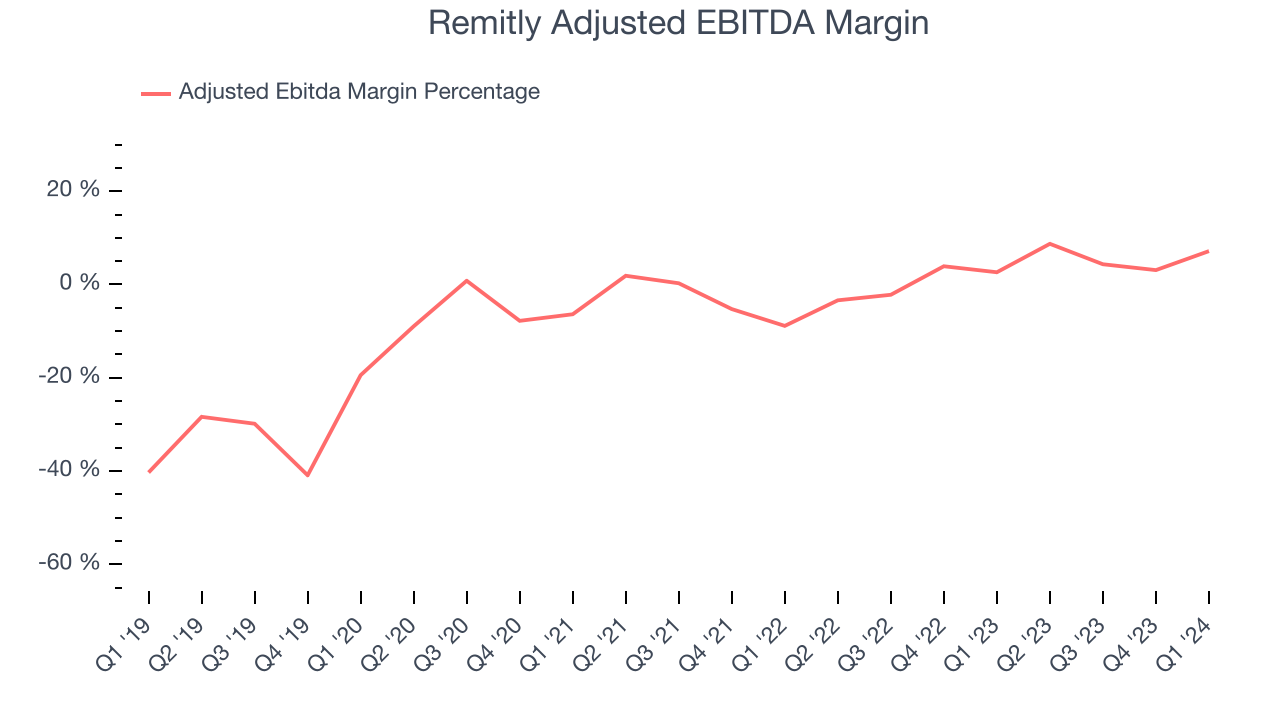

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

Remitly reported EBITDA of $19.26 million this quarter, resulting in a 7.2% margin. The company has also shown above-average profitability for a consumer internet business over the last four quarters, with average EBITDA margins of 5.8%.

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Remitly burned through $61.12 million in Q1,

Remitly has burned through $117.1 million of cash over the last 12 months, resulting in a negative 11.6% free cash flow margin. This low FCF margin stems from Remitly's need to reinvest in its business to fuel revenue growth.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Remitly is a well-capitalized company with $286 million of cash and $163.5 million of debt, meaning it could pay back all its debt tomorrow and still have $122.5 million of cash on its balance sheet. This net cash position gives Remitly the freedom to raise more debt, return capital to shareholders, or invest in growth initiatives.

Key Takeaways from Remitly's Q1 Results

It was unfortunate to see Remitly miss analysts' revenue estimates this quarter as its active customer count fell short. On the bright side, its adjusted EBITDA and EPS beat.

Looking ahead, the company's full-year revenue guidance slightly missed Wall Street's forecast. Overall, the results could have been better, especially considering Remitly's premium valuation. The company is down 20.7% on the results and currently trades at $13.89 per share.

Is Now The Time?

When considering an investment in Remitly, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Remitly is a good business. Its revenue growth has been exceptional over the last three years. And while its ARPU has declined over the last two years, the good news is its growth in active buyers has been strong. On top of that, its gross margins indicate a healthy starting point for the overall profitability of the business.

At the moment, Remitly trades at 31.5x next 12 months EV-to-EBITDA. There's definitely a lot of things to like about Remitly and looking at the consumer internet landscape right now, it seems that it doesn't trade at an unreasonable price.

Wall Street analysts covering the company had a one-year price target of $27.89 per share right before these results (compared to the current share price of $13.89), implying they saw upside in buying Remitly in the short term.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.