Cybersecurity software maker Rapid7 (NASDAQ:RPD) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 12% year on year to $205.1 million. On the other hand, next quarter's revenue guidance of $204 million was less impressive, coming in 2.7% below analysts' estimates. It made a non-GAAP profit of $0.55 per share, improving from its profit of $0.16 per share in the same quarter last year.

Rapid7 (RPD) Q1 CY2024 Highlights:

- Revenue: $205.1 million vs analyst estimates of $204 million (small beat)

- EPS (non-GAAP): $0.55 vs analyst estimates of $0.54 (2.2% beat)

- Revenue Guidance for Q2 CY2024 is $204 million at the midpoint, below analyst estimates of $209.6 million

- The company dropped its revenue guidance for the full year from $852 million to $833 million at the midpoint, a 2.2% decrease

- Gross Margin (GAAP): 70.3%, up from 69.4% in the same quarter last year

- Free Cash Flow of $27.53 million, down 54.3% from the previous quarter

- Annual Recurring Revenue: $807.2 million at quarter end, up 10.9% year on year

- Customers: 11,462, down from 11,526 in the previous quarter

- Market Capitalization: $2.88 billion

Founded in 2000 with the idea that network security comes before endpoint security, Rapid7 (NASDAQ:RPD) provides software as a service that helps companies understand where they are exposed to cyber security risks, quickly detect breaches and respond to them.

Rapid7's software scans all computers, servers and other devices on their customer’s network and finds vulnerabilities that can be exploited by malware or hackers, like computers that haven’t had patches installed. It then automatically alerts responsible personnel and provides them with guidance on how to patch them, reducing average time to fix a vulnerability from days to hours.

Rapid7 also provides companies with a real-time monitoring dashboard with an overview of the activity on their network and alerts them about any suspicious activity, for example a user that has logged in from two different countries. When Rapid7 detects a successful attack it alerts the IT security personnel, scans the network to identify the size of the breach and then provides suggestions on which users should have their access revoked and which parts of the network should be quarantined.

Vulnerability Management

The demand for cybersecurity is growing as more and more businesses are moving their data and processes into the cloud, which along with a major increase in employees working remotely, has increased their exposure to attacks and malware. Additionally, the growing array of corporate IT systems, applications and internet connected devices has increased the complexity of network security, all of which has substantially increased the demand for software meant to protect data breaches.

The market is highly competitive, and Rapid7 is competing with companies like Tenable (NASDAQ:TENB), Qualys (NASDAQ:QLYS) and Crowdstrike (NASDAQ:CRWD).

Sales Growth

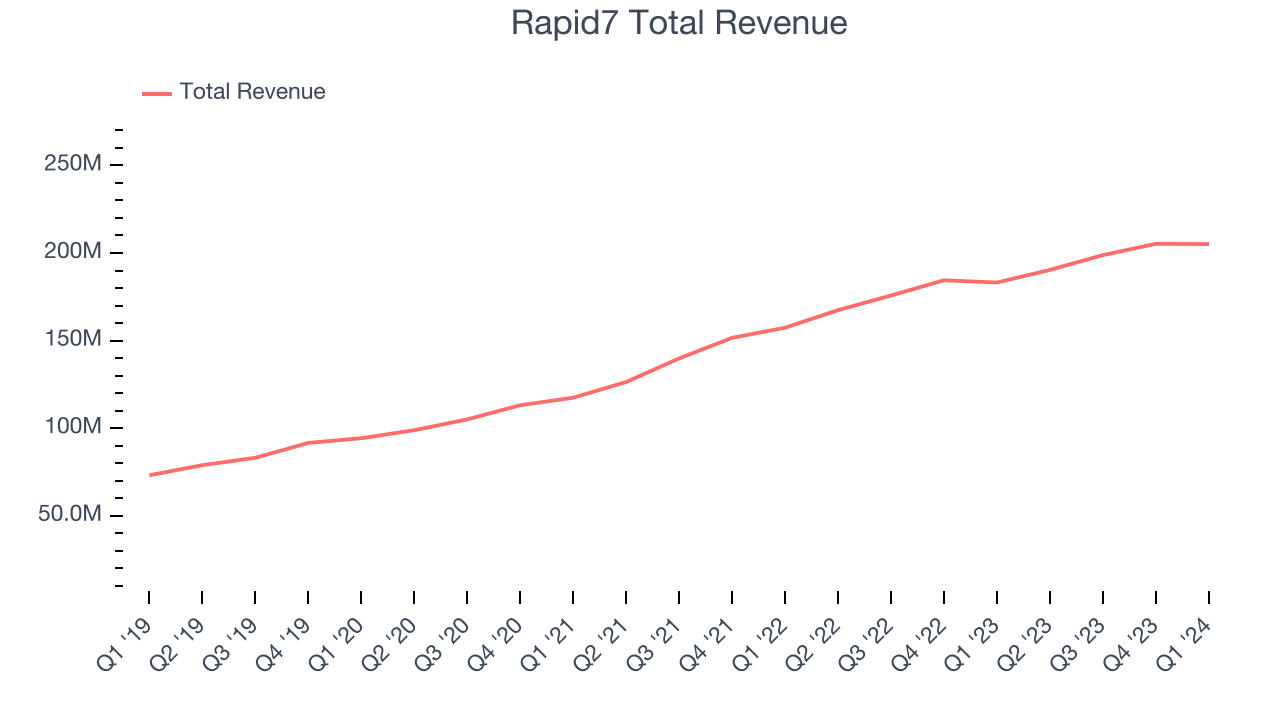

As you can see below, Rapid7's revenue growth has been strong over the last three years, growing from $117.5 million in Q1 2021 to $205.1 million this quarter.

This quarter, Rapid7's quarterly revenue was once again up 12% year on year. However, the company's revenue actually decreased by $167,000 in Q1 compared to the $6.43 million increase in Q4 CY2023. Taking a closer look we can a similar revenue decline in the same quarter last year, which could suggest that the business has seasonal elements. Regardless, this situation is worth monitoring as management is guiding for a further revenue drop in the next quarter.

Next quarter's guidance suggests that Rapid7 is expecting revenue to grow 7.1% year on year to $204 million, slowing down from the 13.7% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 9.3% over the next 12 months before the earnings results announcement.

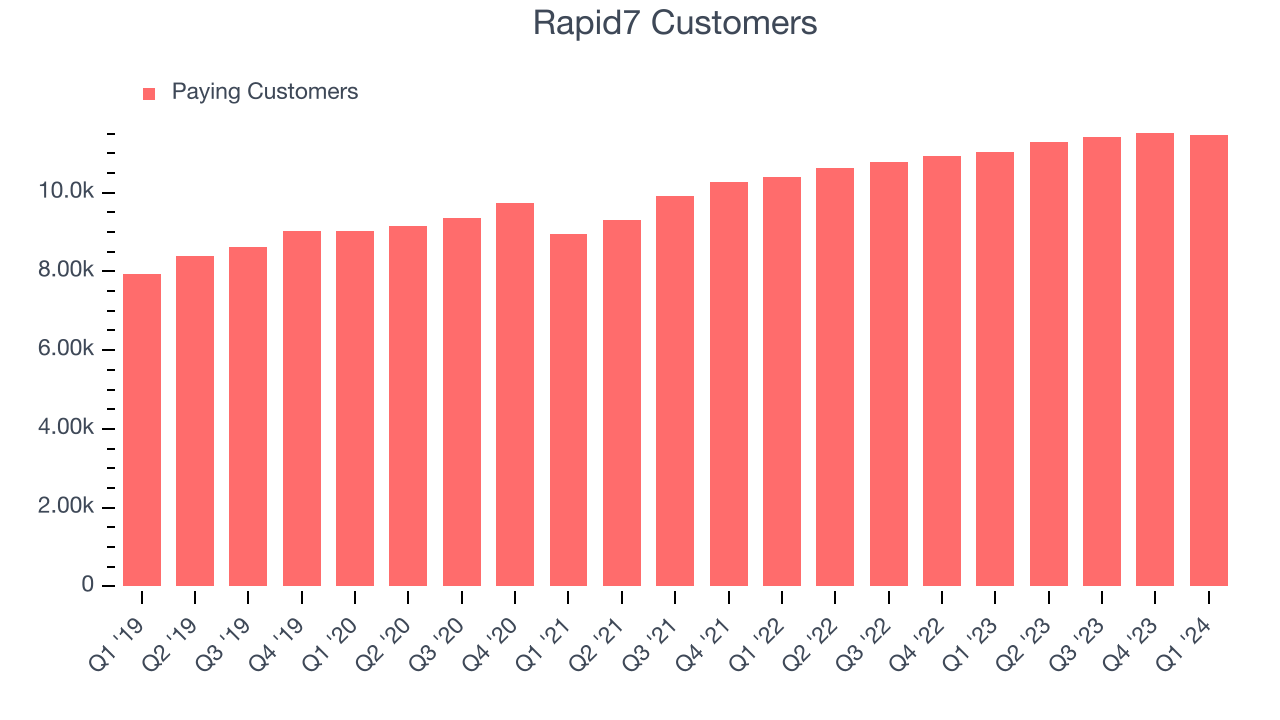

Customer Growth

Rapid7 reported 11,462 customers at the end of the quarter, a decrease of 64 from the previous quarter, suggesting that the company's customer acquisition momentum is slowing. Rapid7 updated its customer count methodology in Q1 2021, which is the reason for the related drop in the number of customers.

Profitability

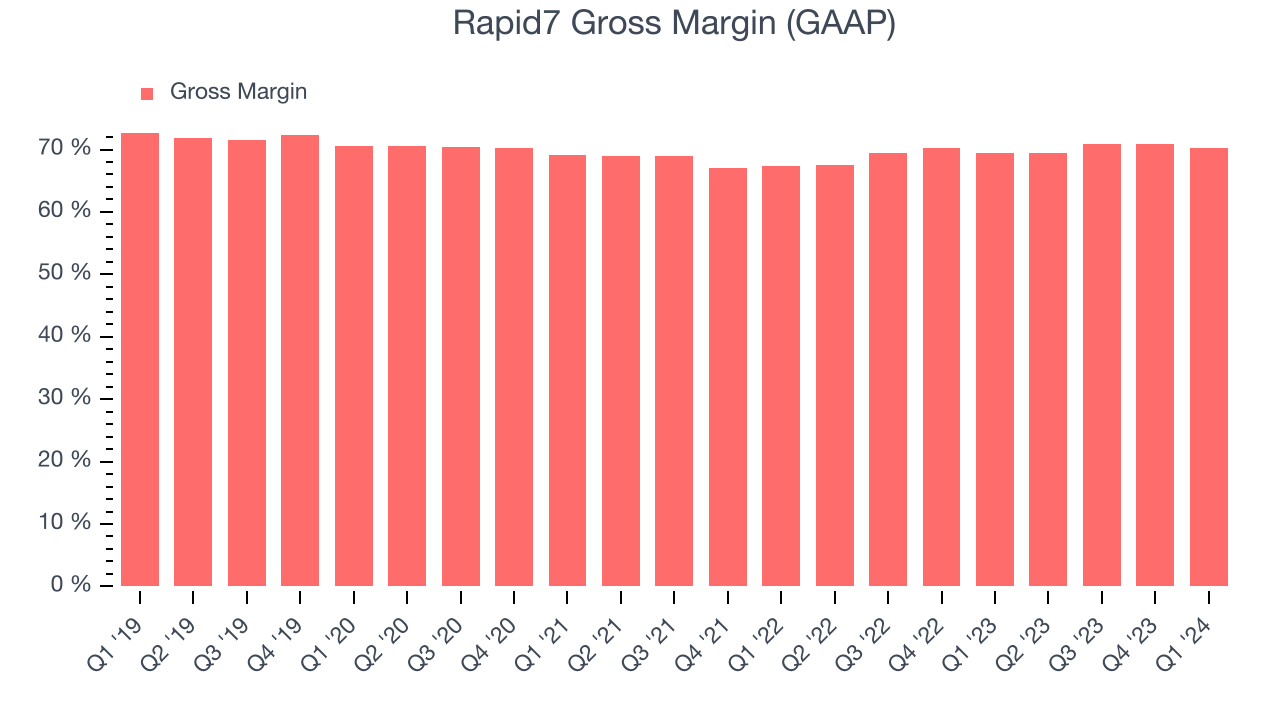

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Rapid7's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 70.3% in Q1.

That means that for every $1 in revenue the company had $0.70 left to spend on developing new products, sales and marketing, and general administrative overhead. Rapid7's gross margin is lower than that of a typical SaaS businesses. Gross margin has a major impact on a company’s ability to develop new products and invest in marketing, which may ultimately determine the winner in a competitive market. This makes it a critical metric to track for the long-term investor.

Cash Is King

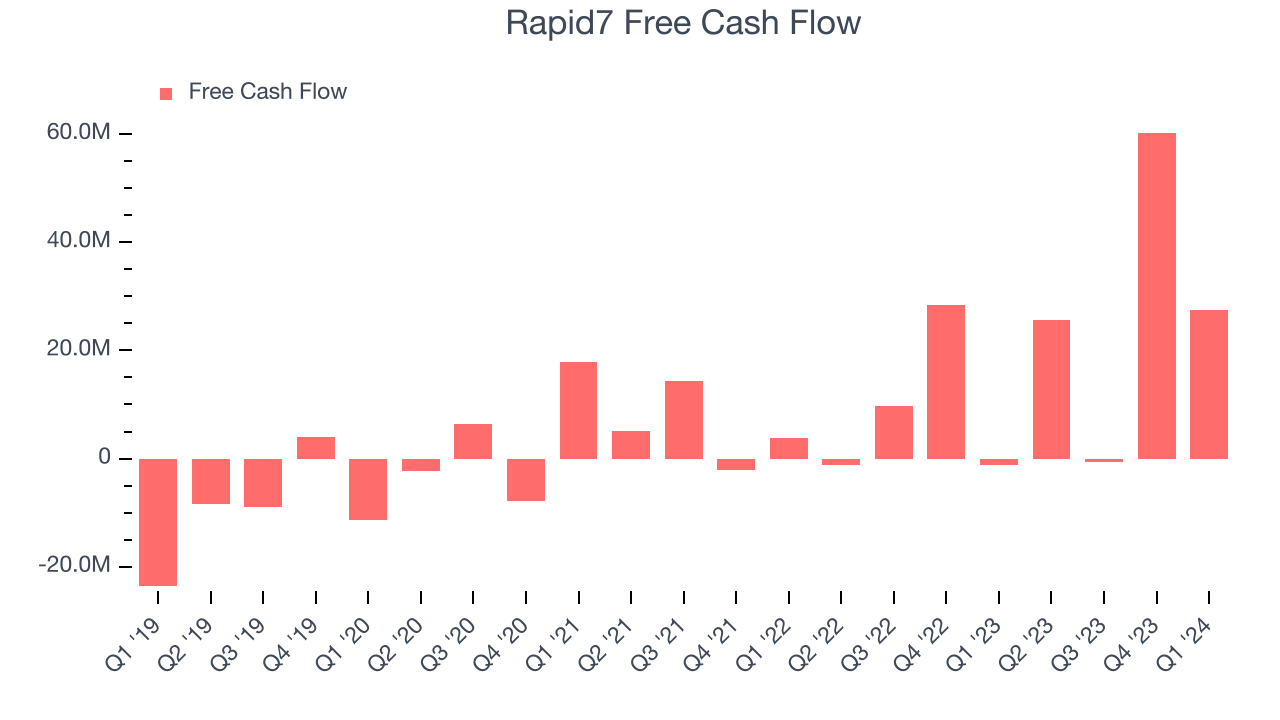

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Rapid7's free cash flow came in at $27.53 million in Q1, turning positive over the last year.

Rapid7 has generated $112.8 million in free cash flow over the last 12 months, a decent 14.1% of revenue. This FCF margin stems from its asset-lite business model and gives it a decent amount of cash to reinvest in its business.

Key Takeaways from Rapid7's Q1 Results

We struggled to find many strong positives in these results. While this quarter's revenue and EPS narrowly topped Wall Street's estimates, its full-year revenue guidance fell short and its free cash flow was down 54.3% from the previous quarter. Overall, this was a subpar quarter for Rapid7. The company is down 4% on the results and currently trades at $44 per share.

Is Now The Time?

Rapid7 may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Although Rapid7 isn't a bad business, it probably wouldn't be one of our picks. Although its revenue growth has been solid over the last three years, Wall Street expects growth to deteriorate from here. On top of that, its customer acquisition is less efficient than many comparable companies.

Rapid7's price-to-sales ratio based on the next 12 months is 3.9x, suggesting the market has lower expectations for the business relative to the hottest tech stocks. We don't really see a big opportunity in the stock at the moment, but in the end, beauty is in the eye of the beholder. If you like Rapid7, it seems to be trading at a reasonable price.

Wall Street analysts covering the company had a one-year price target of $59.66 right before these results (compared to the current share price of $44).

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.