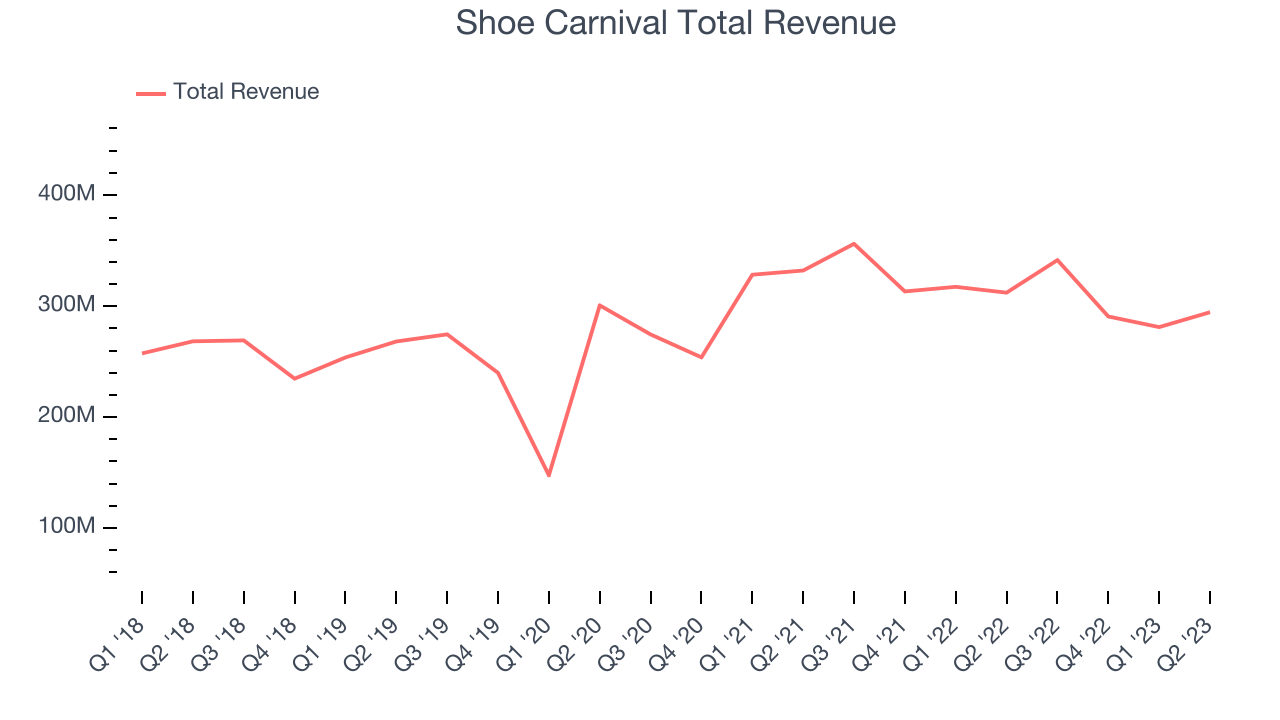

Footwear retailer Shoe Carnival (NASDAQ:SCVL) beat analysts' expectations in Q2 FY2023, with revenue down 5.65% year on year to $294.6 million. The company's outlook for the full year was also close to analysts' estimates with revenue guided to $1.2 billion at the midpoint. Shoe Carnival made a GAAP profit of $19.4 million, down from its profit of $28.9 million in the same quarter last year.

Is now the time to buy Shoe Carnival? Find out by accessing our full research report, it's free.

Shoe Carnival (SCVL) Q2 FY2023 Highlights:

- Revenue: $294.6 million vs analyst estimates of $286.3 million (2.89% beat)

- EPS: $0.71 vs analyst expectations of $0.84 (15% miss)

- The company dropped its revenue guidance for the full year from $1.24 billion to $1.2 billion at the midpoint, a 3.23% decrease

- Free Cash Flow of $4.68 million is up from -$32.1 million in the same quarter last year

- Gross Margin (GAAP): 35.8%, down from 36.2% in the same quarter last year

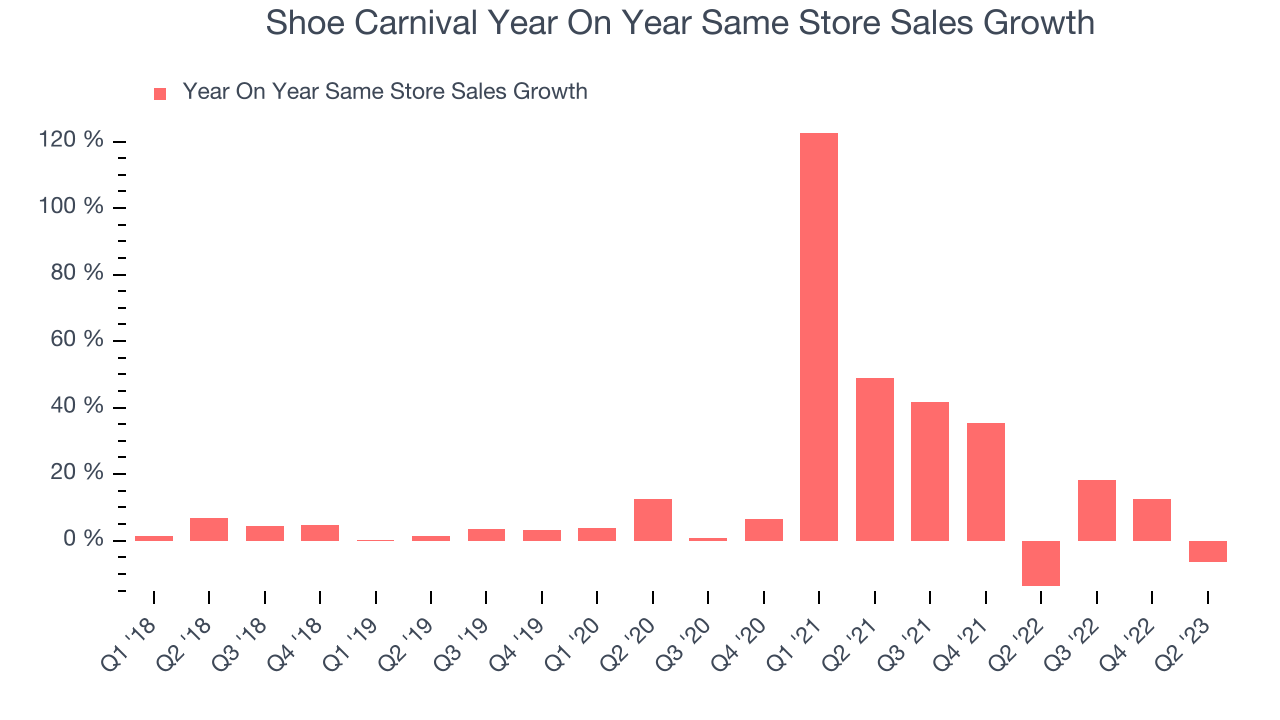

- Same-Store Sales were down 6.5% year on year (beat)

“Our second quarter results demonstrated the momentum of our strategy within the context of a challenging economic backdrop. We delivered improvement on net sales, earnings per share and market share growth versus first quarter 2023, while also increasing investment in our branding, advertising and in-store experience. In August, we opened our 400th store and surpassed over half of our stores being modernized,” said Mark Worden, President and Chief Executive Officer.

Known for its playful atmosphere that features carnival elements, Shoe Carnival (NASDAQ:SCVL) is a retailer that sells footwear from mainstream brands for the entire family.

Footwear sales–like their apparel counterparts–are driven by seasons, trends, and innovation more so than absolute need and similarly face the bigger-picture secular trend of e-commerce penetration. Footwear plays a part in societal belonging, personal expression, and occasion, and retailers selling shoes recognize this. They therefore aim to balance selection, competitive prices, and the latest trends to attract consumers. Unlike their apparel counterparts, footwear retailers most sell popular third-party brands (as opposed to their own exclusive brands), which could mean less exclusivity of product but more nimbleness to pivot to what’s hot.

Sales Growth

Shoe Carnival is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 4.18% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre despite not opening many new stores, implying that growth was driven by higher sales at existing, established stores.

This quarter, Shoe Carnival's revenue fell 5.65% year on year to $294.6 million but beat Wall Street's estimates by 2.89%.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

When a retailer like Shoe Carnival keeps its store footprint steady, it usually means that demand is stable and it's focused on improving its operational efficiency to increase profitability. At the end of this quarter, Shoe Carnival operated 400 total retail locations, in line with its store count 12 months ago.

Over the last two years, the company has only opened a few new stores, averaging 1.92% annual growth in new locations. This sluggish pace lags the broader sector. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

Shoe Carnival's demand has outpaced the broader consumer retail sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 14.6% year on year. Given its flat store count over the same period, this performance could stem from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, Shoe Carnival's same-store sales fell 6.5% year on year. This decrease was an improvement from the 13.8% year-on-year decline it posted 12 months ago. It's always great to see a business improve its prospects.

Key Takeaways from Shoe Carnival's Q2 Results

With a market capitalization of $596.2 million, Shoe Carnival is among smaller companies, but its $46.8 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

While the company beat expectations for quarterly same-store sales and revenue, EPS missed. Additionally, full year guidance was lowered, which is the major negative driving the stock down. Management said that they noticed "improving conditions related to the impact of inflation in the second quarter, but some of our urban customers remain challenged in the current economic environment." The company is down 5.92% on the results and currently trades at $20.5 per share.

So should you invest in Shoe Carnival right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.