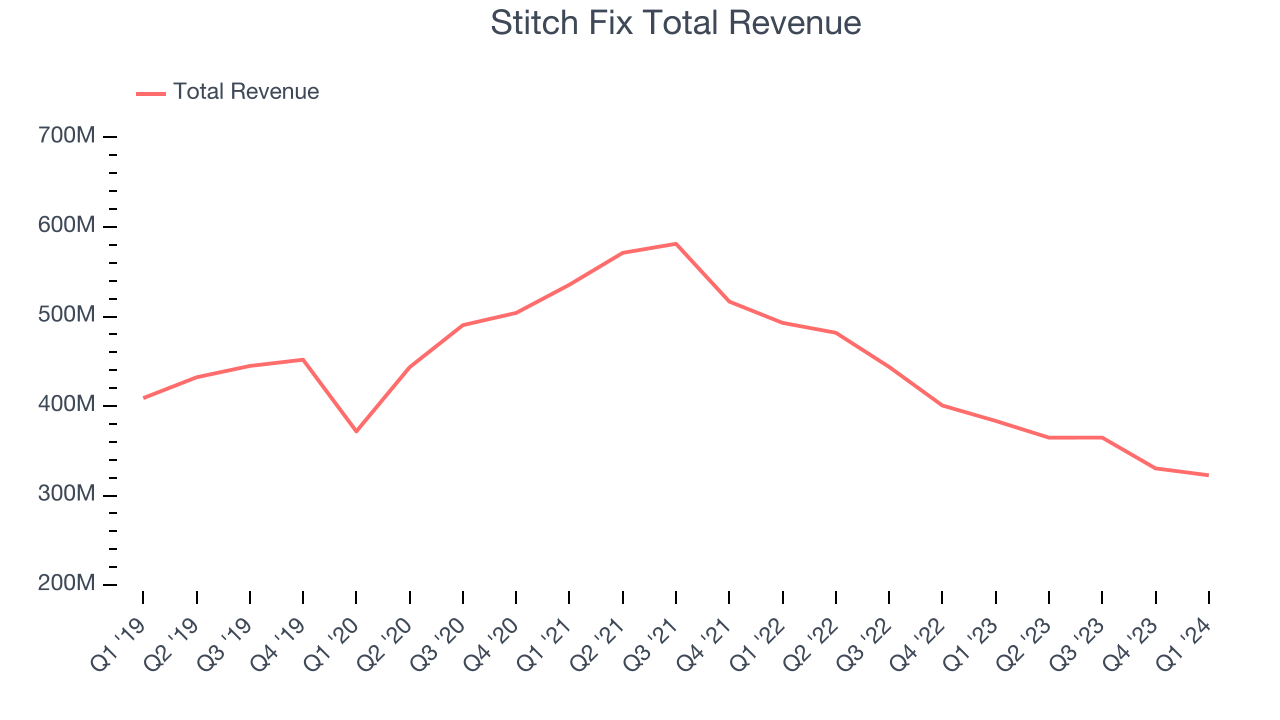

Personalized clothing company Stitch Fix (NASDAQ:SFIX) reported Q1 CY2024 results topping analysts' expectations, with revenue down 15.8% year on year to $322.7 million. On top of that, next quarter's revenue guidance ($317 million at the midpoint) was surprisingly good and 3.4% above what analysts were expecting. It made a GAAP loss of $0.18 per share, down from its loss of $0.16 per share in the same quarter last year.

Is now the time to buy Stitch Fix? Find out by accessing our full research report, it's free.

Stitch Fix (SFIX) Q1 CY2024 Highlights:

- Revenue: $322.7 million vs analyst estimates of $306.2 million (5.4% beat)

- Adjusted EBITDA: $6.7 million vs analyst estimates of ($2.3) million (big beat)

- Revenue Guidance for Q2 CY2024 is $317 million at the midpoint, above analyst estimates of $306.5 million (adjusted EBITDA guidance also comfortably ahead)

- Gross Margin (GAAP): 45.5%, up from 40.8% in the same quarter last year

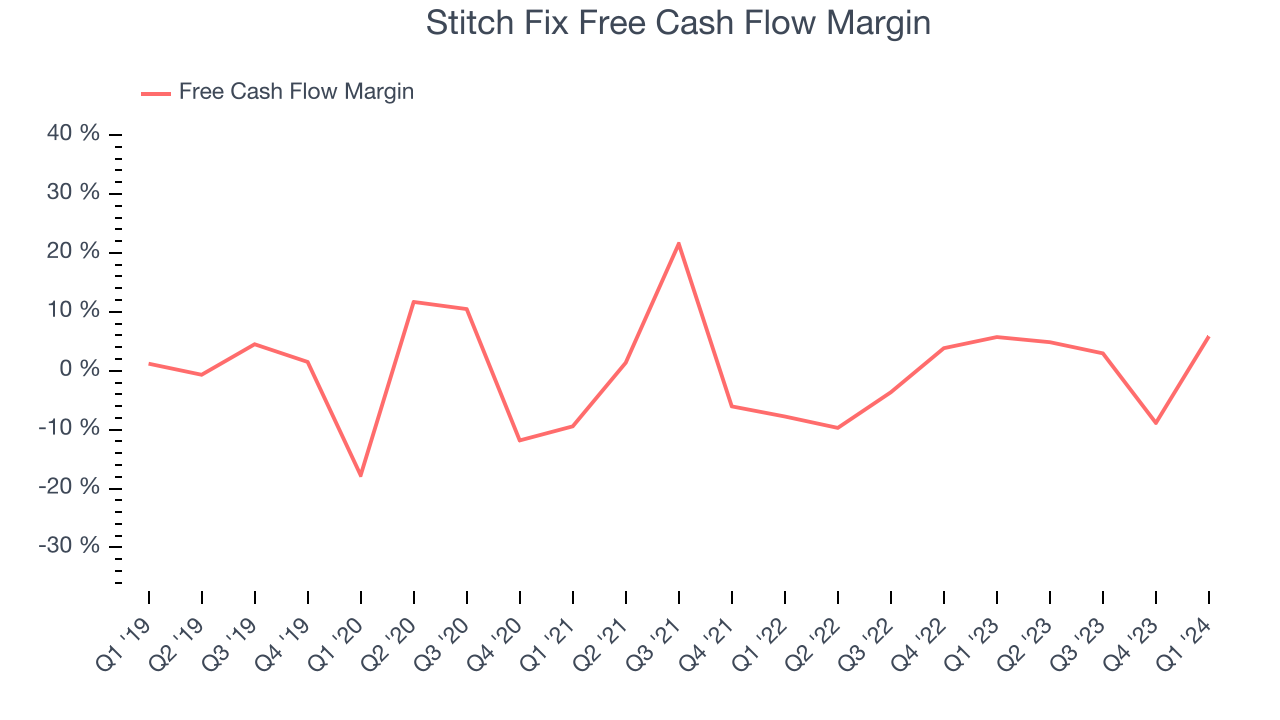

- Free Cash Flow of $18.91 million is up from -$29.26 million in the previous quarter

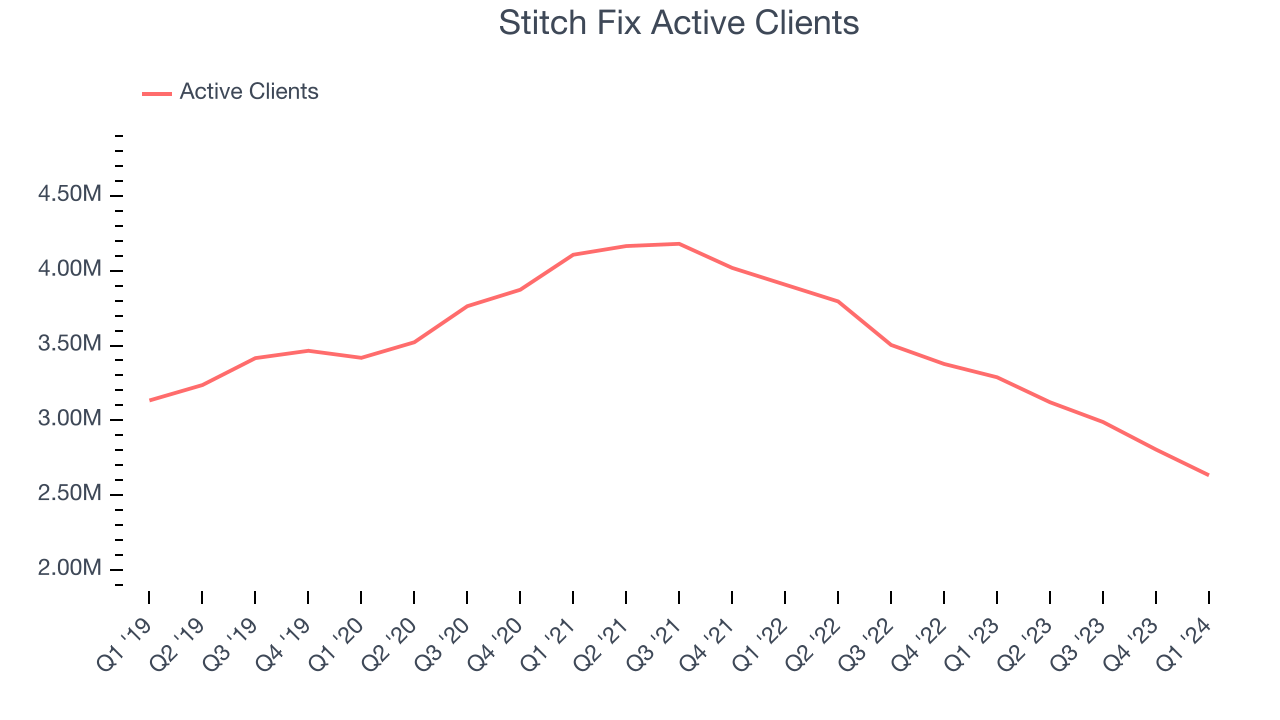

- Active Clients: 2.63 million, down 655,000 year on year

- Market Capitalization: $310 million

“At Stitch Fix, we are on a mission to help people discover the styles they will love that fit perfectly so they always look and feel their best, and this commitment is at the heart of our transformation,” said Matt Baer, Chief Executive Officer, Stitch Fix.

One of the original subscription box companies, Stitch Fix (NASDAQ:SFIX) is an online personal styling and fashion service that curates personalized clothing selections for customers.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Stitch Fix had weak demand over the last five years as its sales fell by 1.1% annually, a rough starting point in our assessment of quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Stitch Fix's annualized revenue declines of 20% over the last two years suggest its recent demand was even weaker than before.

We can dig further into the company's revenue dynamics by analyzing its number of active clients, which reached 2.63 million in the latest quarter. Over the last two years, Stitch Fix's active clients averaged 15.8% year-on-year declines. Because this number is higher than its revenue growth during the same period, we can see the company's monetization has fallen.

This quarter, Stitch Fix's revenue fell 15.8% year on year to $322.7 million but beat Wall Street's estimates by 5.4%. The company is guiding for a 13.1% year-on-year revenue decline next quarter to $317 million, an improvement from the 24.3% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects revenue to decline 6% over the next 12 months.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Stitch Fix broke even from a free cash flow perspective over the last two years, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders.

Stitch Fix's free cash flow clocked in at $18.91 million in Q1, equivalent to a 5.9% margin. This quarter's margin was in line with the comparable period last year.

Key Takeaways from Stitch Fix's Q1 Results

We were impressed by how significantly Stitch Fix blew past analysts' adjusted EBITDA expectations this quarter. We were also glad its full-year revenue and adjusted EBITDA guidance came in higher than Wall Street's estimates. On the other hand, its number of active clients unfortunately missed. Zooming out, we think this was an impressive quarter that should delight shareholders. The stock is up 20.7% after reporting and currently trades at $3.21 per share.

Stitch Fix may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.