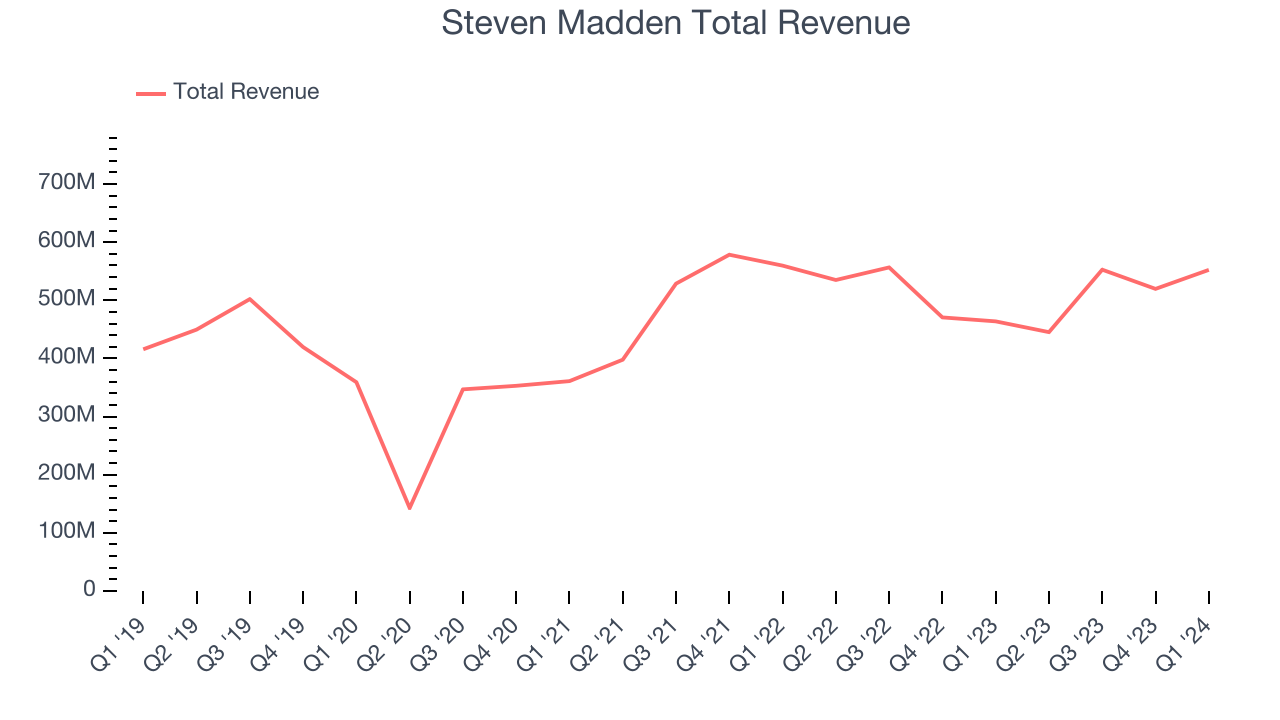

Shoe and apparel company Steven Madden (NASDAQ:SHOO) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 19.1% year on year to $552.4 million. It made a non-GAAP profit of $0.65 per share, improving from its profit of $0.50 per share in the same quarter last year.

Is now the time to buy Steven Madden? Find out by accessing our full research report, it's free.

Steven Madden (SHOO) Q1 CY2024 Highlights:

- Revenue: $552.4 million vs analyst estimates of $525.2 million (5.2% beat)

- EPS (non-GAAP): $0.65 vs analyst estimates of $0.55 (17.3% beat)

- Gross Margin (GAAP): 40.7%, down from 42.1% in the same quarter last year

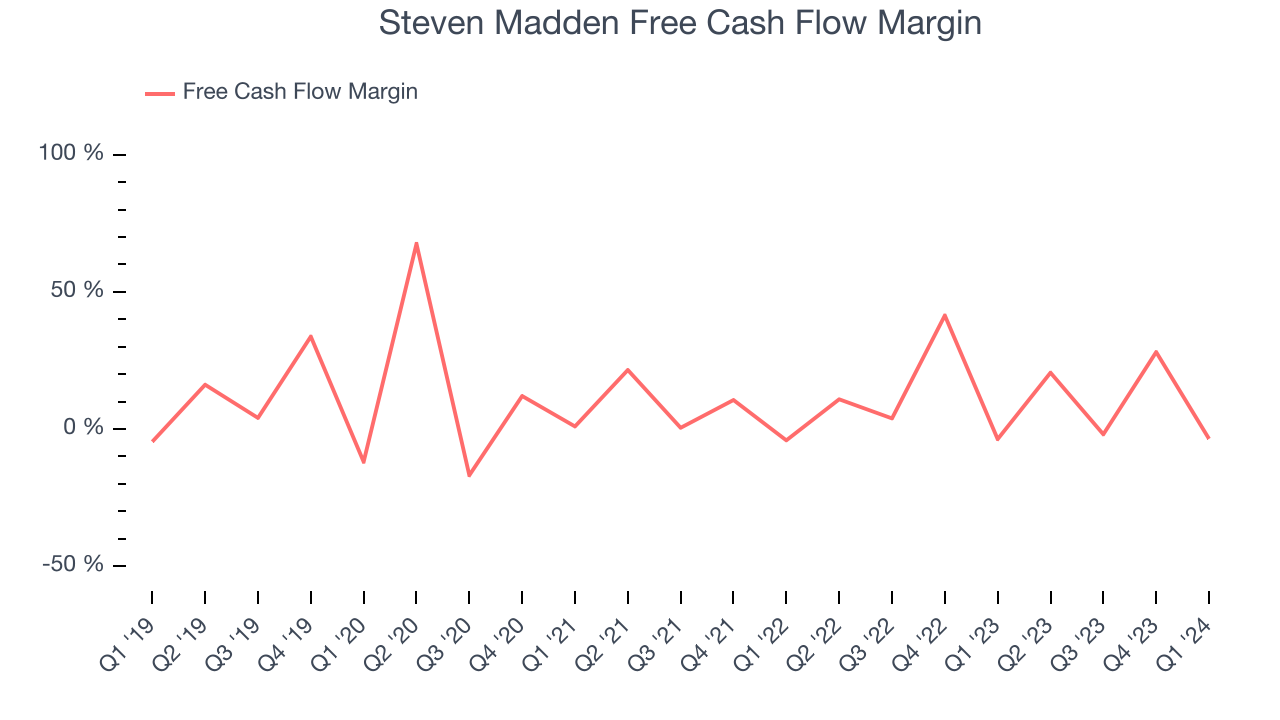

- Free Cash Flow was -$19.68 million, down from $145.9 million in the previous quarter

- Market Capitalization: $2.96 billion

Edward Rosenfeld, Chairman and Chief Executive Officer, commented, “We got off to a strong start to 2024, with first quarter revenue increasing 19% and Adjusted diluted EPS rising 30% compared to the same period in 2023. We also demonstrated tangible progress on our key strategic initiatives, with double-digit percentage revenue growth in international markets, non-footwear categories and direct-to-consumer channels as well as a return to year-over-year revenue growth in the U.S. wholesale footwear business. Looking ahead, we are confident that the continued execution of our strategy will enable us to drive sustainable revenue and earnings growth and create significant value for our stakeholders over the long term.”

As seen in the infamous Wolf of Wall Street movie, Steven Madden (NASDAQ:SHOO) is a fashion brand famous for its trendy and innovative footwear, appealing to a young and style-conscious audience.

Footwear

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Steven Madden's annualized revenue growth rate of 4% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Steven Madden's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Steven Madden's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

We can better understand the company's revenue dynamics by analyzing its most important segments, Wholesale and Retail, which are 79.3% and 20.3% of revenue. Over the last two years, Steven Madden's Wholesale revenue (sales to retailers) averaged 3.8% year-on-year growth while its Retail revenue (direct sales to consumers) was flat.

This quarter, Steven Madden reported robust year-on-year revenue growth of 19.1%, and its $552.4 million of revenue exceeded Wall Street's estimates by 5.2%. Looking ahead, Wall Street expects sales to grow 8.6% over the next 12 months, a deceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Steven Madden has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 11.3%, slightly better than the broader consumer discretionary sector.

Steven Madden burned through $19.68 million of cash in Q1, equivalent to a negative 3.6% margin, reducing its cash burn by 15.3% year on year. Over the next year, analysts predict Steven Madden's cash profitability will fall. Their consensus estimates imply its LTM free cash flow margin of 10% will decrease to 8.1%.

Key Takeaways from Steven Madden's Q1 Results

We enjoyed seeing Steven Madden exceed analysts' revenue and EPS expectations this quarter, driven by outperformance in its Wholesale segment. During the quarter, the Board approved a $0.21 quarterly dividend, payable on June 21, 2024 to stockholders as of June 10, 2024.

Looking ahead, the company's full-year revenue guidance was in line with estimates while its projected EPS was slightly below. Overall, we think this was a solid quarter. The stock is flat after reporting and currently trades at $40.41 per share.

So should you invest in Steven Madden right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.