Plant-based food and beverage company SunOpta (NASDAQGS:STKL) beat analysts' expectations in Q4 FY2023, with revenue down 17.9% year on year to $181.6 million. The company expects the full year's revenue to be around $685 million, in line with analysts' estimates. It made a non-GAAP profit of $0.05 per share, improving from its profit of $0.04 per share in the same quarter last year.

SunOpta (STKL) Q4 FY2023 Highlights:

- Revenue: $181.6 million vs analyst estimates of $172.1 million (5.5% beat)

- EPS (non-GAAP): $0.05 vs analyst estimates of $0.02 ($0.03 beat)

- Management's revenue guidance for the upcoming financial year 2024 is $685 million at the midpoint, in line with analyst expectations and implying -10.6% growth (vs -8.4% in FY2023)

- Free Cash Flow was -$4.42 million compared to -$14.05 million in the previous quarter

- Gross Margin (GAAP): 14.1%, down from 15% in the same quarter last year

- Sales Volumes were up 14.7% year on year

- Market Capitalization: $712 million

Committed to clean-label foods, SunOpta (NASDAQGS:STKL) is a sustainability-focused food and beverage company specializing in the sourcing, processing, and packaging of natural and organic products.

The company was established in the early 1970s as a small operation focused on processing and supplying organic and non-GMO soybeans. At the time, the health benefits of soy were gaining recognition, and SunOpta aimed to capitalize on its growing demand.

Over the years, SunOpta has expanded its offerings to include a diverse range of products, such as plant-based milk beverages, fruit-based snacks, organic ingredients, and specialty grains. SunOpta runs a vertically integrated model to ensure its rigorous quality standards are met, and its products are carefully sourced, processed, and distributed to meet the growing demand for natural and nutritious food options.

The company's commitment to wholesome foods resonates with health-conscious consumers, and it serves customers in North America, Europe, Asia, and beyond. Its plant-based beverage brands consist of SOWN, DREAM, and West Life and can be found at select retailers. SunOpta also partners with food manufacturers through its Sunrise Growers division to provide private-label and co-branded products.

Packaged Food

Packaged food stocks are considered resilient investments because people always need to eat. These companies therefore can enjoy consistent demand as long as they stay on top of changing consumer preferences. But consumer preferences can be a double-edged sword, as companies that aren't at the front of trends such as health and wellness and natural ingredients can fall behind. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Competitors include private companies Organic Valley and Nature’s Path along with public companies Oatly (NASDAQGS:OTLY), Conagra (NYSE:CAG), and General Mills (NYSE:GIS).Sales Growth

SunOpta is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale.

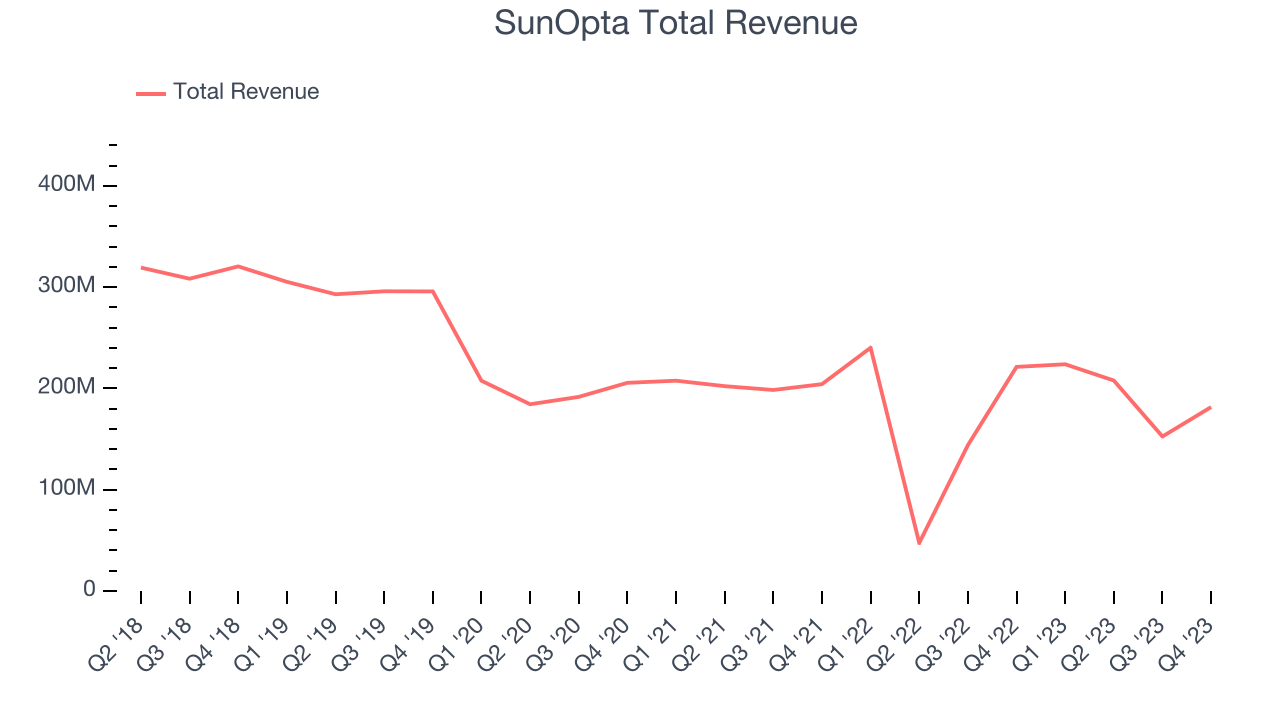

As you can see below, the company's revenue was flat over the last three years. This is poor for a consumer staples business.

This quarter, SunOpta's revenue fell 17.9% year on year to $181.6 million but beat Wall Street's estimates by 5.5%. Looking ahead, Wall Street expects revenue to decline 10.3% over the next 12 months.

Gross Margin & Pricing Power

Gross profit margins tell us how much money a company gets to keep after paying for the direct costs of the goods it sells.

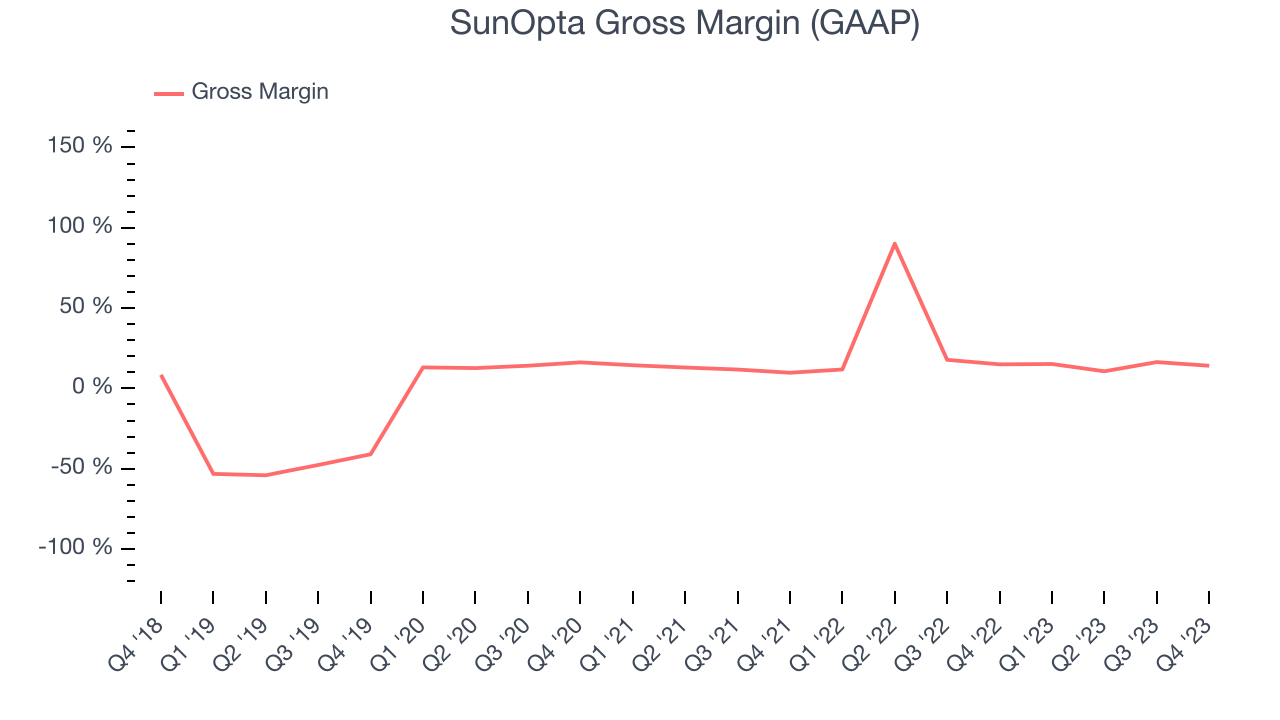

This quarter, SunOpta's gross profit margin was 14.1%, in line with the same quarter last year. That means for every $1 in revenue, a chunky $0.86 went towards paying for raw materials, production of goods, and distribution expenses.

SunOpta has weak unit economics for a consumer staples company, making it difficult to reinvest in the business. As you can see above, it's averaged a 25.6% gross margin over the last eight quarters. Its margin has also been trending down over the last year, averaging 18.3% year-on-year decreases each quarter. If this trend continues, it could suggest a more competitive environment where SunOpta has diminishing pricing power and less favorable input costs (such as raw materials).

Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

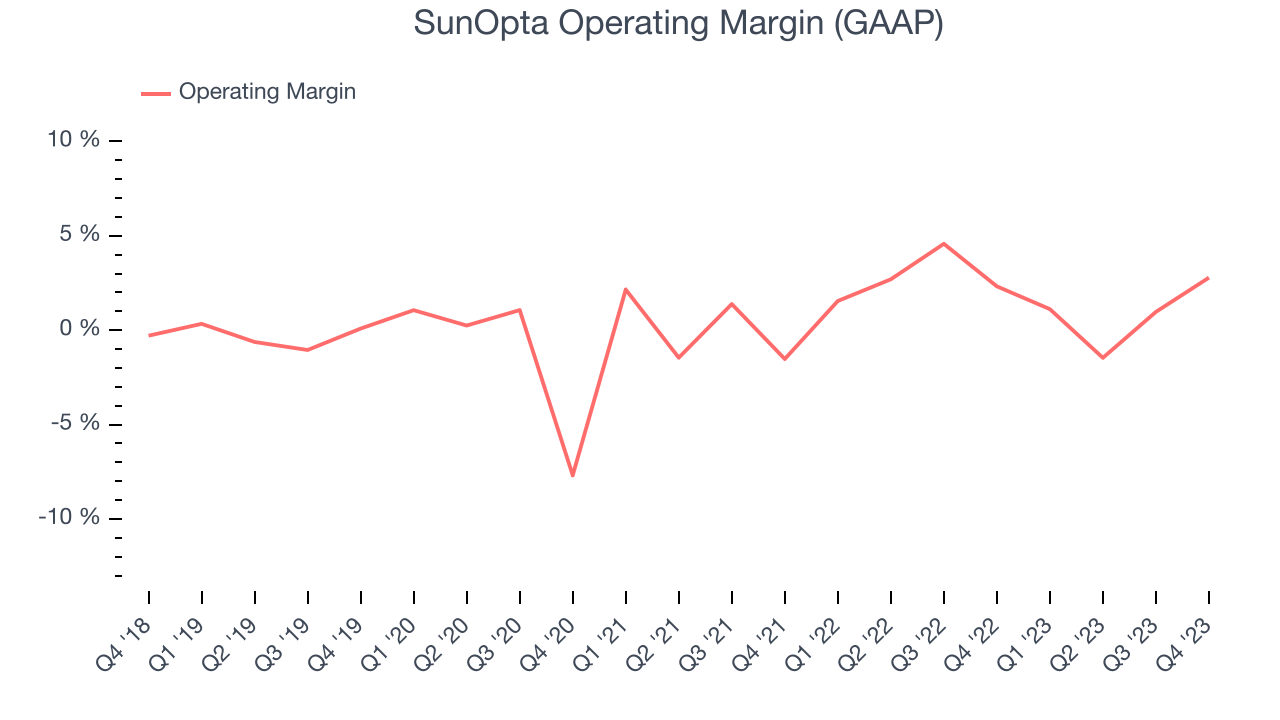

This quarter, SunOpta generated an operating profit margin of 2.8%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

Zooming out, SunOpta was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 1.7%. On top of that, SunOpta's margin has declined by 1.8 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.

Zooming out, SunOpta was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 1.7%. On top of that, SunOpta's margin has declined by 1.8 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.EPS

Earnings growth is a critical metric to track, but for long-term shareholders, earnings per share (EPS) is more telling because it accounts for dilution and share repurchases.

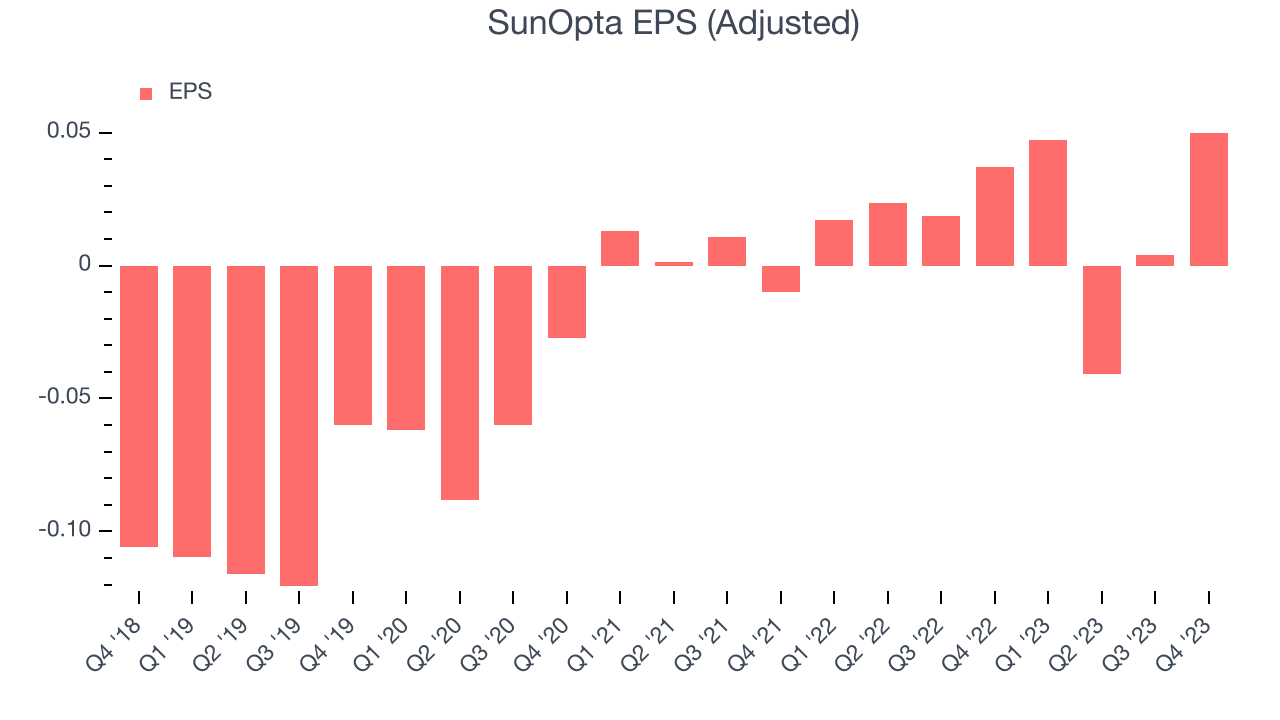

In Q4, SunOpta reported EPS at $0.05, up from $0.04 in the same quarter a year ago. This print easily cleared Wall Street's estimates, and shareholders should be content with the results.

Between FY2020 and FY2023, SunOpta cut its earnings losses. Its EPS has improved by 31.1% on average each year.

Wall Street expects the company to continue growing earnings over the next 12 months, with analysts projecting an average 124% year-on-year increase in EPS.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

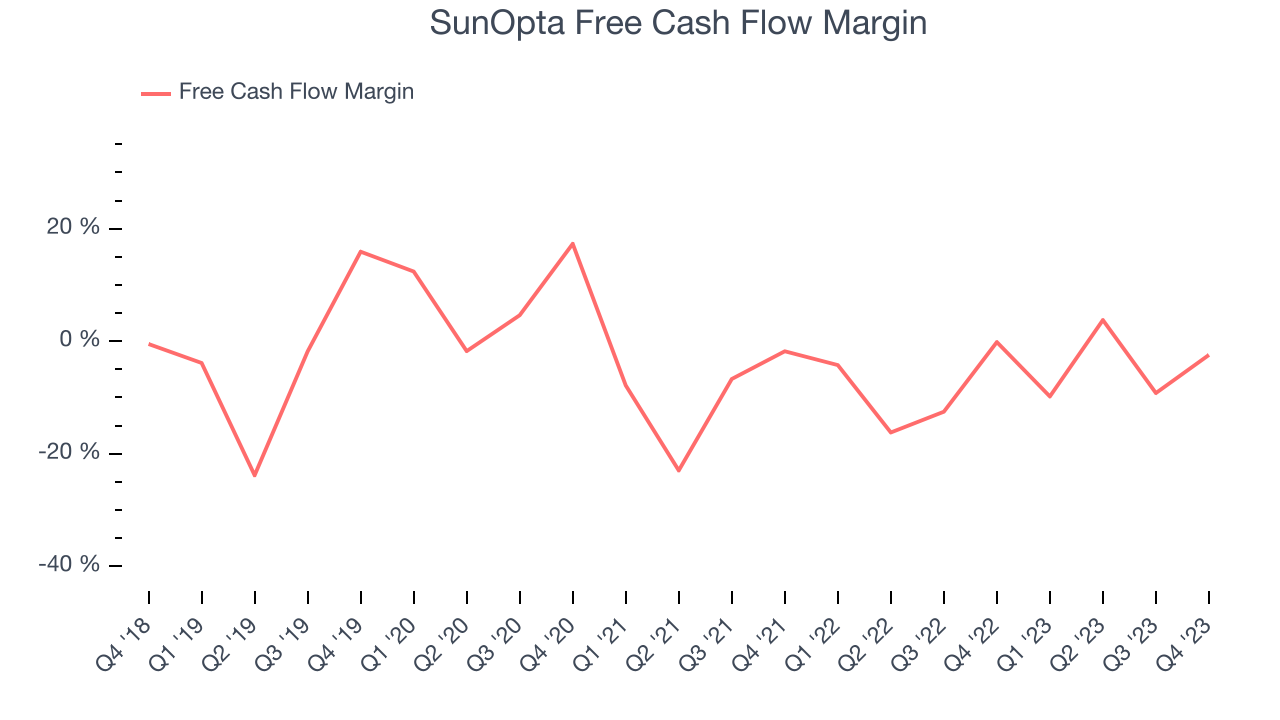

SunOpta burned through $4.42 million of cash in Q4, representing a negative 2.4% free cash flow margin. The company reduced its cash burn by 1,224% year on year.

Over the last two years, SunOpta's demanding reinvestments to stay relevant with consumers have drained company resources. Its free cash flow margin has been among the worst in the consumer staples sector, averaging negative 6.2%. However, its margin has averaged year-on-year increases of 3.8 percentage points over the last 12 months, showing the company is at least improving.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

SunOpta's five-year average ROIC was 0.5%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last two years, SunOpta's ROIC averaged 3.6 percentage point increases each year. This is a good sign and we hope the company can continue to improving.

Key Takeaways from SunOpta's Q4 Results

We were impressed that both revenue and EPS beat expectations pretty meaningfully this quarter. Revenue guidance was in line with expectations, showing that the company is staying on track. Overall, this was a fine quarter for SunOpta. The stock is up 5% after reporting and currently trades at $6.31 per share.

Is Now The Time?

When considering an investment in SunOpta, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for all companies serving consumers, but in the case of SunOpta, we'll be cheering from the sidelines. Its revenue has declined over the last three years, and analysts expect growth to deteriorate from here. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its cash burn raises the question of whether it can sustainably maintain growth. On top of that, its relatively low ROIC suggests it has struggled to grow profits historically.

SunOpta's price-to-earnings ratio based on the next 12 months is 44.5x. While we've no doubt one can find things to like about SunOpta, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $8.86 per share right before these results (compared to the current share price of $6.31).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.