Cybersecurity software maker Tenable (NASDAQ:TENB) reported Q2 FY2021 results beating Wall St's expectations, with revenue up 21.5% year on year to $130.2 million. Tenable made a GAAP loss of $11.6 million, improving on its loss of $11.9 million, in the same quarter last year.

Is now the time to buy Tenable? Get early access to our full analysis of the earnings results here, it's free

Tenable (TENB) Q2 FY2021 Highlights:

- Revenue: $130.2 million vs analyst estimates of $125.5 million (3.77% beat)

- EPS (non-GAAP): $0.09 vs analyst estimates of $0.05 ($0.04 beat)

- Revenue guidance for Q3 2021 is $134 million at the midpoint, above analyst estimates of $133.1 million

- The company lifted revenue guidance for the full year, from $522 million to $529.5 million at the midpoint, a 1.43% increase

- Free cash flow of $15 million, down 60% from previous quarter

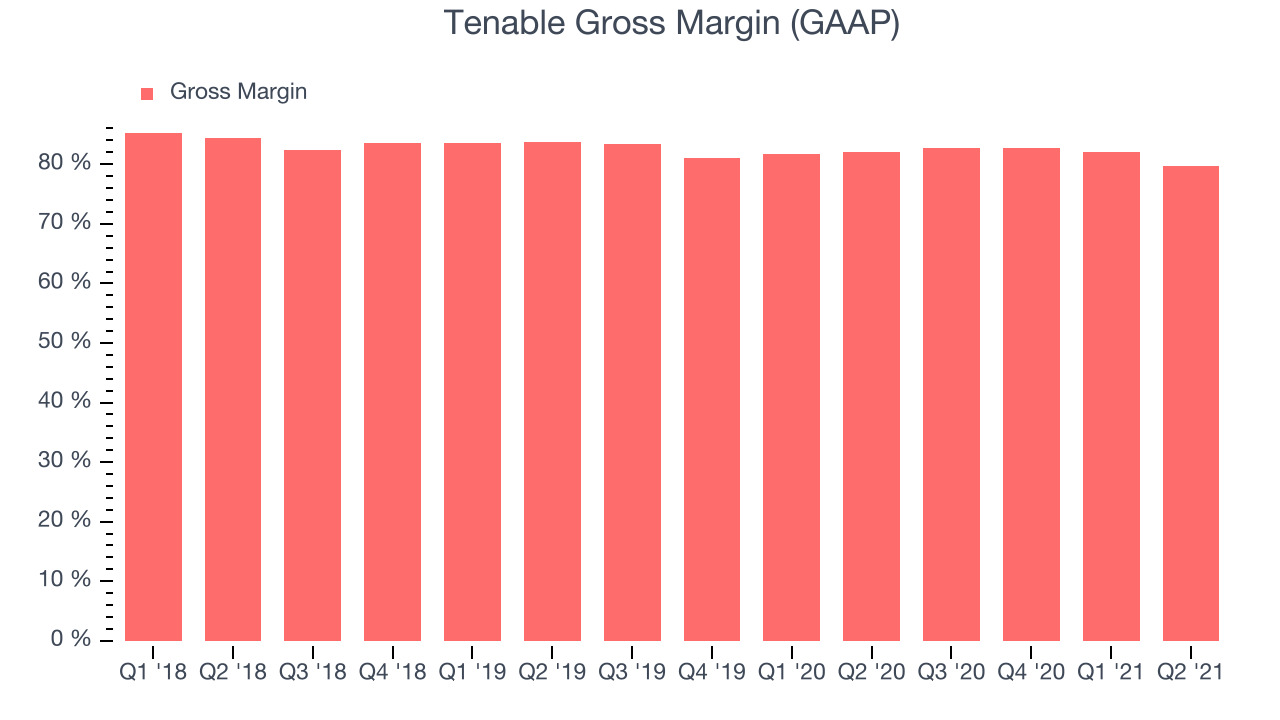

- Gross Margin (GAAP): 79.7%, down from 82% previous quarter

“We are pleased with results for the second quarter as calculated current billings and revenue growth accelerated from strong customer adds and large deals,” said Amit Yoran, Chairman and CEO of Tenable.

Founded in 2002, Tenable (NASDAQ:TENB) provides software as a service that helps companies understand where they are exposed to cyber security risk and how to reduce it.

The demand for cybersecurity is growing as more and more businesses are moving their data and processes into the cloud and are becoming exposed to attacks and malware. Employees working remotely have also made it harder for companies to keep their networks secure, thereby increasing demand for software that helps protect from breaches.

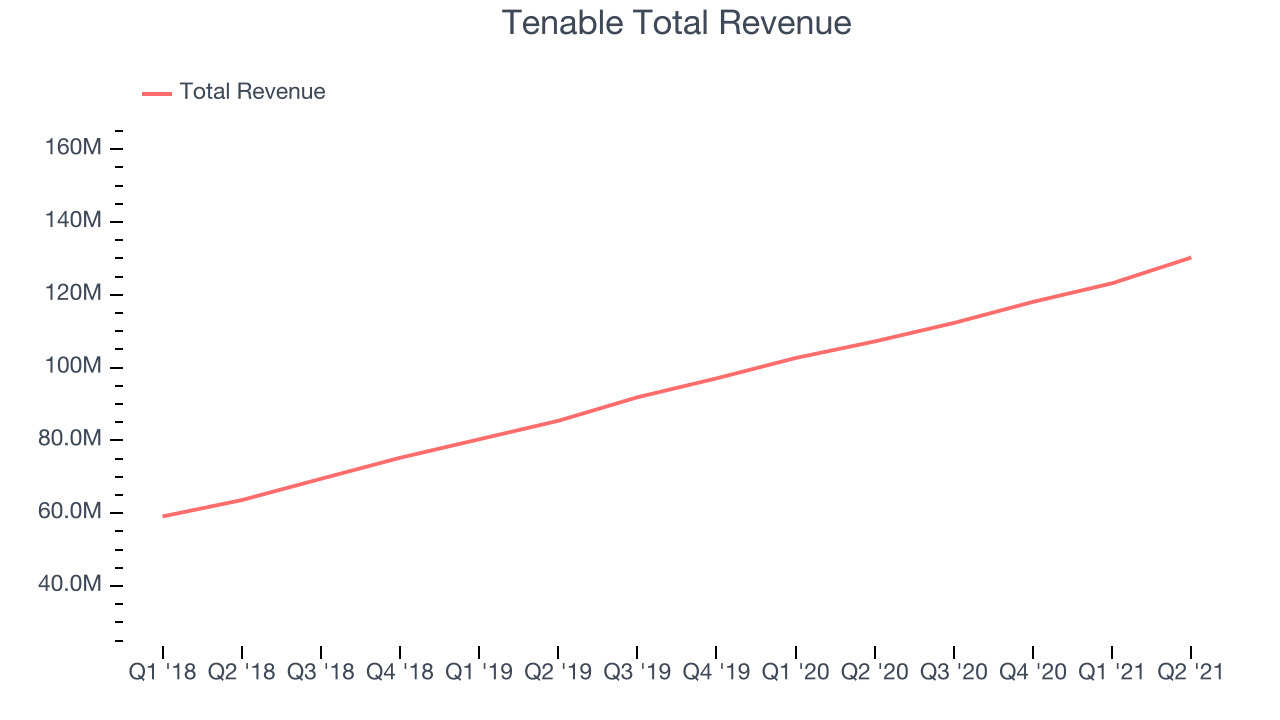

Sales Growth

As you can see below, Tenable's revenue growth has been strong over the last year, growing from quarterly revenue of $107.2 million, to $130.2 million.

This quarter, Tenable's quarterly revenue was once again up a very solid 21.5% year on year. On top of that, revenue increased $7.07 million quarter on quarter, a very strong improvement on the $5.1 million increase in Q1 2021, which shows acceleration of growth, and is great to see.

Analysts covering the company are expecting the revenues to grow 17.5% over the next twelve months, although we would expect them to review their estimates once they get to read these results.

There are others doing even better. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 400% since the IPO in December. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Tenable's gross profit margin, an important metric measuring how much money there is left after paying for servers, licences, technical support and other necessary running expenses was at 79.7% in Q2.

That means that for every $1 in revenue the company had $0.79 left to spend on developing new products, marketing & sales and the general administrative overhead. Despite the recent drop this is still, this is still a good gross margin that allows companies like Tenable to fund large investments in product and sales during periods of rapid growth and be profitable when they reach maturity.

Key Takeaways from Tenable's Q2 Results

With market capitalisation of $4.78 billion Tenable is among smaller companies, but its more than $261 million in cash and positive free cash flow over the last twelve months put it in a very strong position to invest in growth.

It was good to see Tenable outperform Wall St’s revenue expectations this quarter. And we were also glad that the revenue guidance for the rest of the year was upgraded. On the other hand, it was unfortunate to see the deterioration in gross margin. Zooming out, we think this was still a decent, albeit mixed, quarter, showing the company is staying on target. The company is flat on the results and currently trades at $44.6 per share.

When considering Tenable, investors should take into account its valuation and business qualities, as well as what happened in the latest quarter. Is now the right time to invest? Are there better opportunities? Get access to our full analysis here, it's free.

The author has no position in any of the stocks mentioned.