Tenable (NASDAQ:TENB) Exceeds Q1 Expectations But Quarterly Guidance Underwhelms

Max Juang 2024/05/01 4:05 pm EDT

Cybersecurity software maker Tenable (NASDAQ:TENB) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 14.4% year on year to $216 million. On the other hand, the company expects next quarter's revenue to be around $218 million, slightly below analysts' estimates. It made a non-GAAP profit of $0.25 per share, improving from its profit of $0.11 per share in the same quarter last year.

Tenable (TENB) Q1 CY2024 Highlights:

- Revenue: $216 million vs analyst estimates of $213.4 million (1.2% beat)

- EPS (non-GAAP): $0.25 vs analyst estimates of $0.17 (43.4% beat)

- Revenue Guidance for Q2 CY2024 is $218 million at the midpoint, below analyst estimates of $219.3 million (operating profit guidance for the period also below)

- The company reconfirmed its revenue guidance for the full year of $904 million at the midpoint (above expectations, as was operating profit guidance for the full year)

- Gross Margin (GAAP): 77.3%, up from 75.9% in the same quarter last year

- Free Cash Flow of $47.13 million, up 31.8% from the previous quarter

- Market Capitalization: $5.34 billion

Founded in 2002 by three cybersecurity veterans, Tenable (NASDAQ:TENB) provides software as a service that helps companies understand where they are exposed to cyber security risk and how to reduce it.

Tenable’s software scans all computers, servers and other devices on their customer’s network and finds vulnerabilities that can be exploited by malware or hackers, like computers that haven’t had patches installed or unsecured wifi. It then helps companies understand how severe the vulnerabilities are, alerts them if new ones appear and guides them through removing them.

Vulnerability Management

The demand for cybersecurity is growing as more and more businesses are moving their data and processes into the cloud, which along with a major increase in employees working remotely, has increased their exposure to attacks and malware. Additionally, the growing array of corporate IT systems, applications and internet connected devices has increased the complexity of network security, all of which has substantially increased the demand for software meant to protect data breaches.

Cybersecurity is a competitive space and while Tenable is a leader in vulnerability assessment, it faces competition from companies like Qualys (NASDAQ:QLYS), Rapid7 (NASDAQ:RPD) and CrowdStrike (NASDAQ:CRWD).

Sales Growth

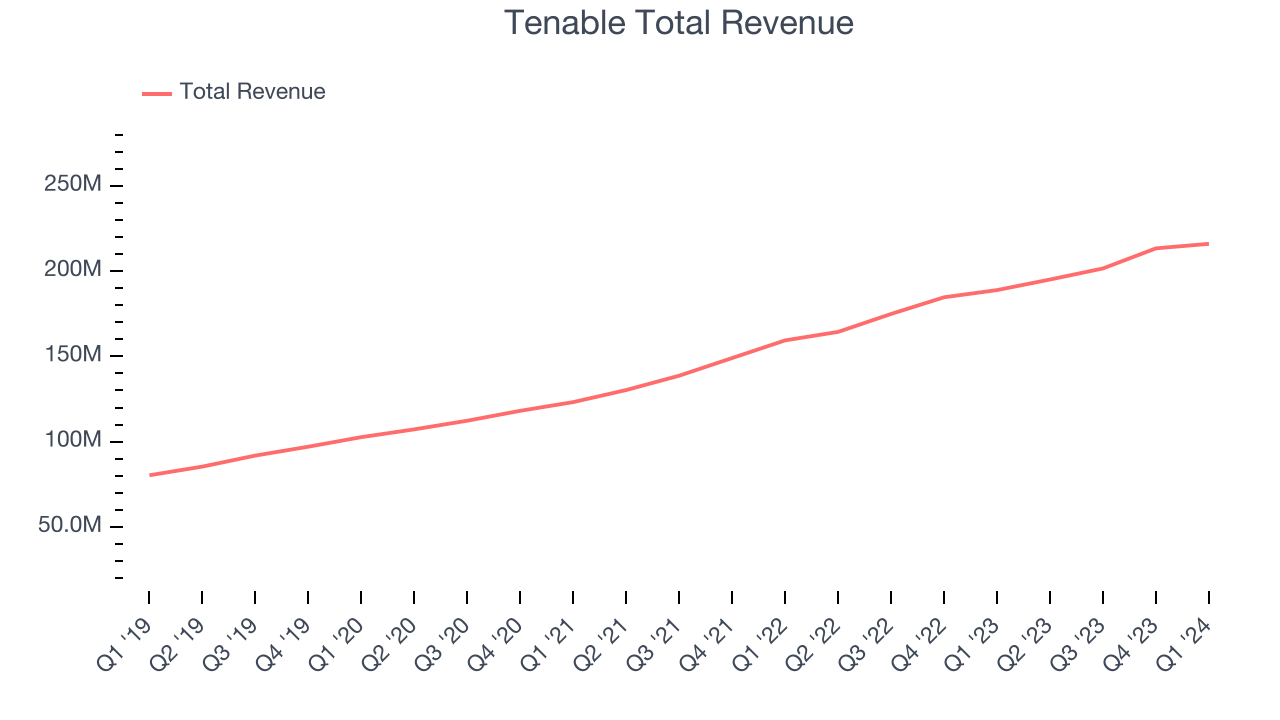

As you can see below, Tenable's revenue growth has been strong over the last three years, growing from $123.2 million in Q1 2021 to $216 million this quarter.

This quarter, Tenable's quarterly revenue was once again up 14.4% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $2.66 million in Q1 compared to $11.78 million in Q4 CY2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Tenable is expecting revenue to grow 11.8% year on year to $218 million, slowing down from the 18.7% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 12.7% over the next 12 months before the earnings results announcement.

Profitability

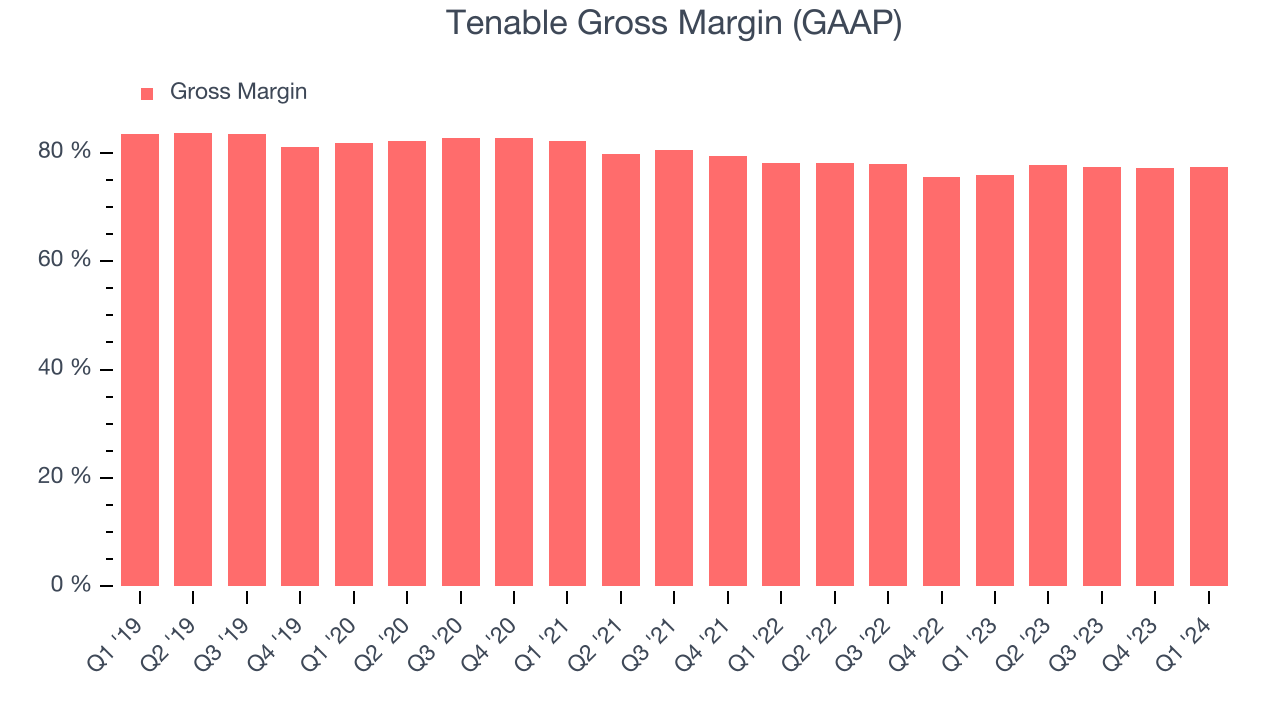

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Tenable's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 77.3% in Q1.

That means that for every $1 in revenue the company had $0.77 left to spend on developing new products, sales and marketing, and general administrative overhead. Tenable's impressive gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity. It's also comforting to see its gross margin remain stable, indicating that Tenable is controlling its costs and not under pressure from its competitors to lower prices.

Cash Is King

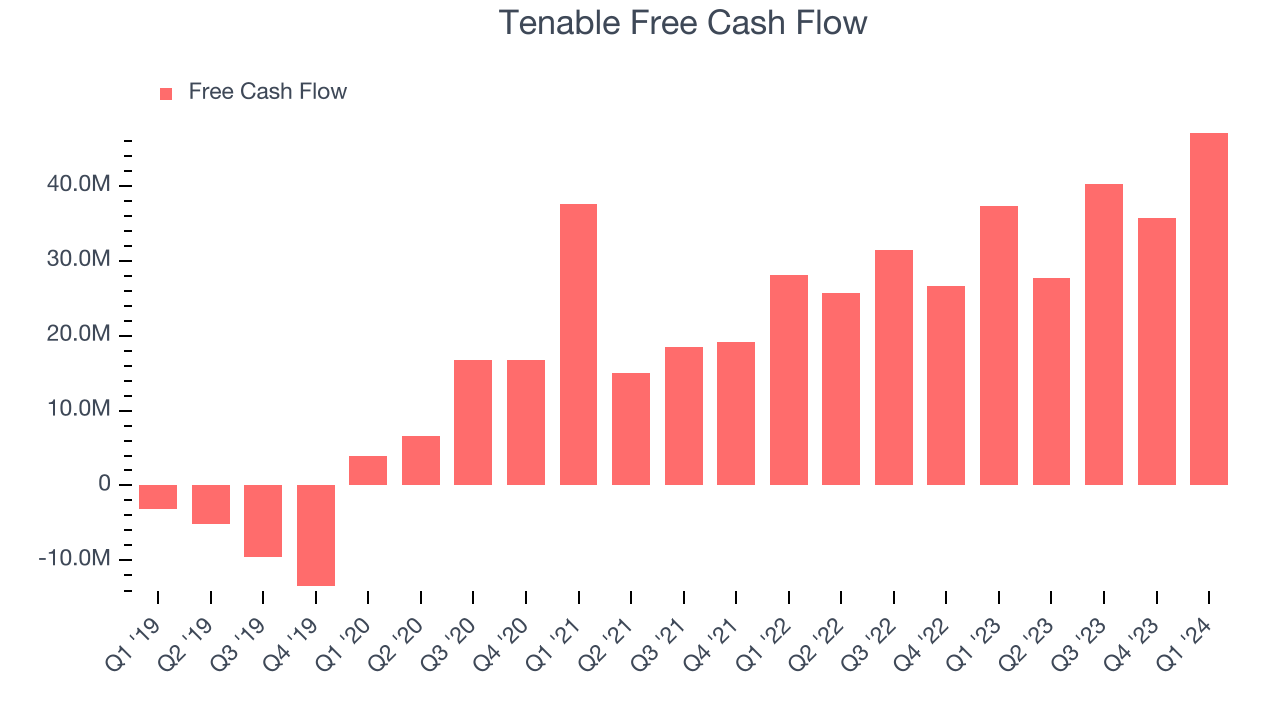

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Tenable's free cash flow came in at $47.13 million in Q1, up 26.2% year on year.

Tenable has generated $150.9 million in free cash flow over the last 12 months, a solid 18.3% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from Tenable's Q1 Results

We enjoyed seeing Tenable exceed analysts' billings expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street's estimates. Full year revenue and operating profit guidance both came in above expectations. On the other hand, its revenue guidance for next quarter missed analysts' expectations. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 2.2% after reporting and currently trades at $46 per share.

Is Now The Time?

When considering an investment in Tenable, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Tenable is a solid business. We'd expect growth rates to moderate from here, but its revenue growth has been solid over the last three years. On top of that, its strong gross margins suggest it can operate profitably and sustainably and its customers are spending noticeably more each year, which is great to see.

Given its price-to-sales ratio of 5.7x based on the next 12 months, the market is certainly expecting long-term growth from Tenable. There are definitely a lot of things to like about Tenable, and looking at the tech landscape right now, it seems to be trading at a reasonable price.

Wall Street analysts covering the company had a one-year price target of $58.19 right before these results (compared to the current share price of $46), implying they see short-term upside potential in Tenable.

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.