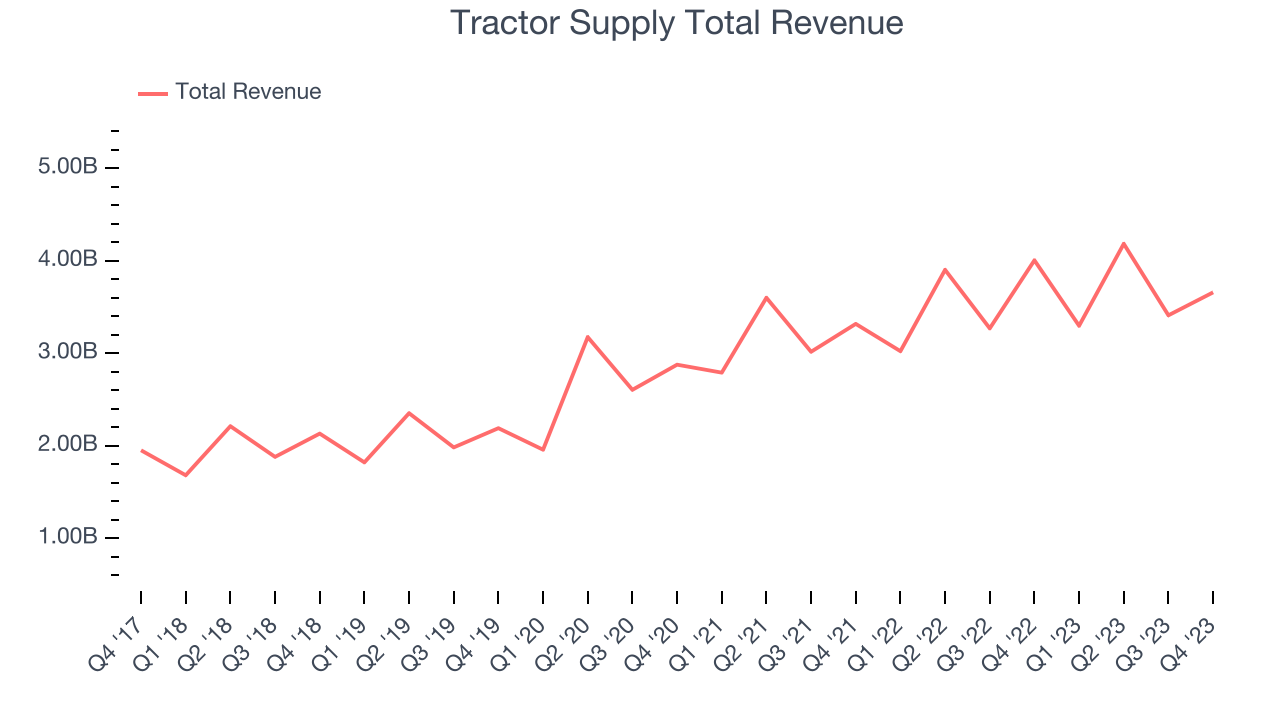

Rural goods retailer Tractor Supply (NASDAQ:TSCO) fell short of analysts' expectations in Q4 FY2023, with revenue down 8.6% year on year to $3.66 billion. The company's full-year revenue guidance of $14.9 billion at the midpoint also came in slightly below analysts' estimates. It made a GAAP profit of $2.28 per share, down from its profit of $2.43 per share in the same quarter last year.

Is now the time to buy Tractor Supply? Find out by accessing our full research report, it's free.

Tractor Supply (TSCO) Q4 FY2023 Highlights:

- Market Capitalization: $24.28 billion

- Revenue: $3.66 billion vs analyst estimates of $3.68 billion (0.5% miss)

- EPS: $2.28 vs analyst estimates of $2.22 (2.8% beat)

- Management's revenue guidance for the upcoming financial year 2024 is $14.9 billion at the midpoint, missing analyst estimates by 0.9% and implying 2.4% growth (vs 3% in FY2023)

- Free Cash Flow of $168.9 million, down 58.6% from the same quarter last year

- Gross Margin (GAAP): 35.3%, up from 34% in the same quarter last year

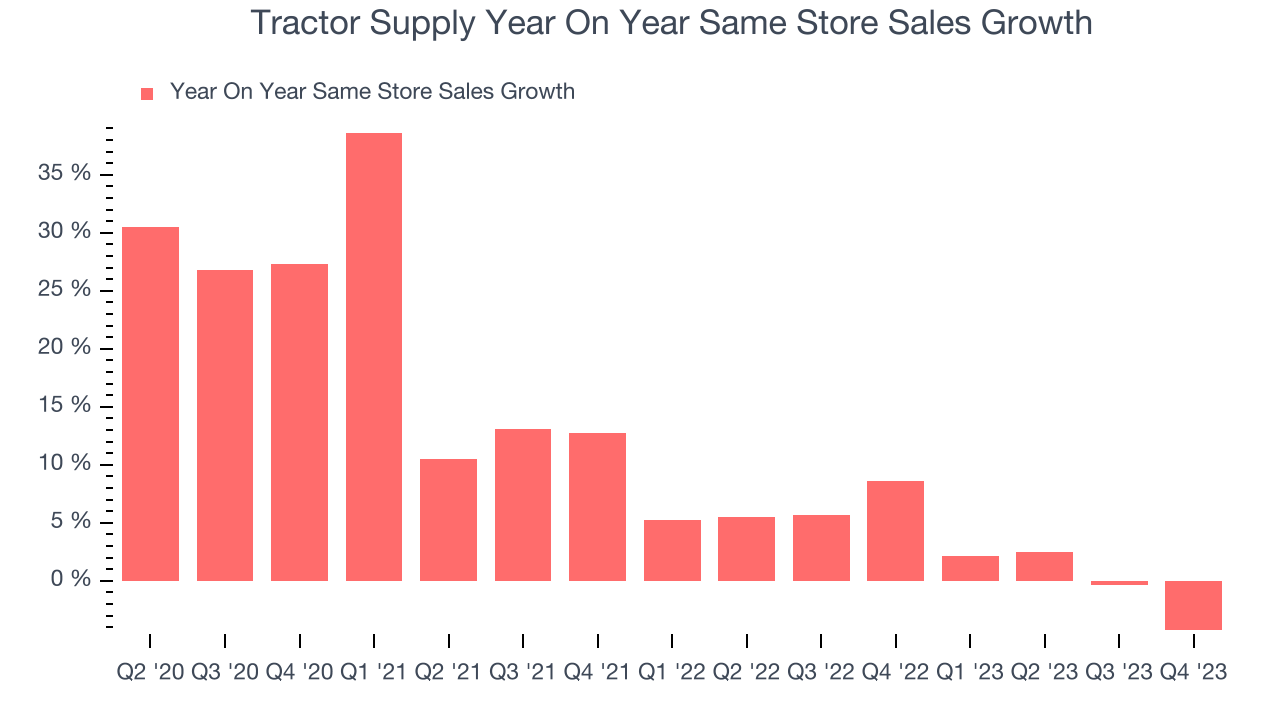

- Same-Store Sales were down 4.2% year on year

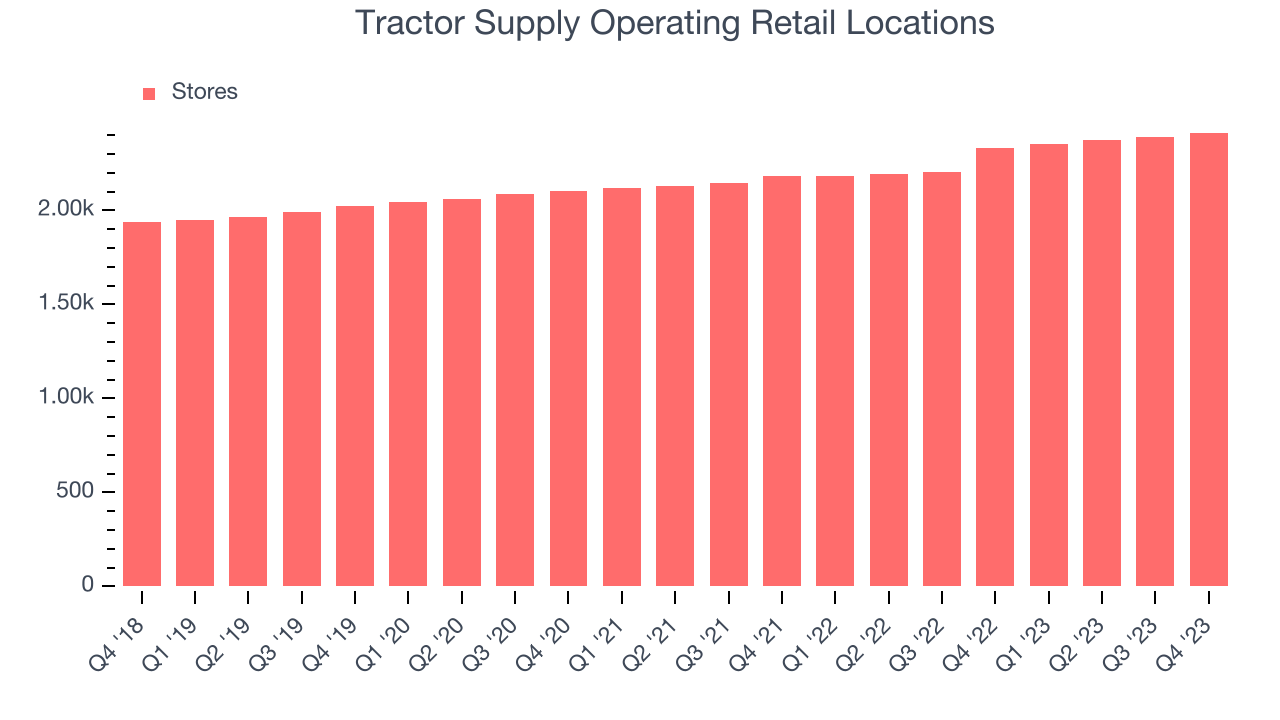

- Store Locations: 2,414 at quarter end, increasing by 81 over the last 12 months

"While our financial performance in 2023 did not meet our initial expectations, our team successfully navigated a highly dynamic environment with agility, operational resiliency and a focus on our strategic investments," said Hal Lawton, President and Chief Executive Officer of Tractor Supply.

Started as a mail-order tractor parts business, Tractor Supply (NASDAQ:TSCO) is a retailer of general goods such as agricultural supplies, hardware, and pet food for the rural consumer.

Specialty Retail

Some retailers try to sell everything under the sun, while others—appropriately called Specialty Retailers—focus on selling a narrow category and aiming to be exceptional at it. Whether it’s eyeglasses, sporting goods, or beauty and cosmetics, these stores win with depth of product in their category as well as in-store expertise and guidance for shoppers who need it. E-commerce competition exists and waning retail foot traffic impacts these retailers, but the magnitude of the headwinds depends on what they sell and what extra value they provide in their stores.

Sales Growth

Tractor Supply is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 14.9% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was solid as it added more brick-and-mortar locations and increased sales at existing, established stores.

This quarter, Tractor Supply missed Wall Street's estimates and reported a rather uninspiring 8.6% year-on-year revenue decline, generating $3.66 billion in revenue. Looking ahead, Wall Street expects sales to grow 3% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Number of Stores

When a retailer like Tractor Supply is opening new stores, it usually means it's investing for growth because demand is greater than supply. Tractor Supply's store count increased by 81 locations, or 3.5%, over the last 12 months to 2,414 total retail locations in the most recently reported quarter.

Taking a step back, the company has opened new stores quickly over the last eight quarters, averaging 5.5% annual growth in new locations. This store growth outpaces the broader consumer retail sector. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Tractor Supply's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 3.1% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Tractor Supply is reaching more customers and growing sales.

In the latest quarter, Tractor Supply's same-store sales fell 4.2% year on year. This decline was a reversal from the 8.6% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Tractor Supply's Q4 Results

It was good to see Tractor Supply beat analysts' gross margin and EPS expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue slightly missed estimates as its sales volumes fell 2.7% and prices fell 1.5%. Furthermore, its full-year 2024 revenue and earnings guidance was underwhelming as it projected flattish same-store sales. Overall, the results could have been better. The stock is up 1% after reporting and currently trades at $227 per share.

So should you invest in Tractor Supply right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.