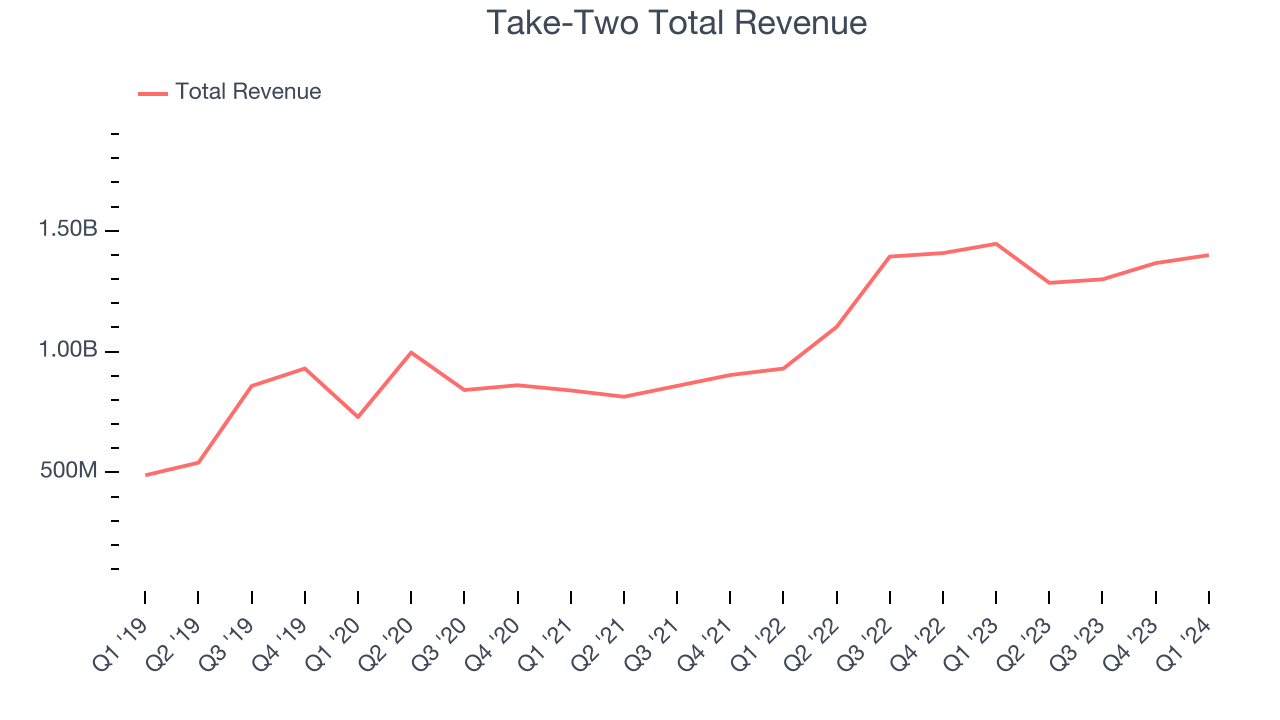

Video game publisher Take Two (NASDAQ:TTWO) beat analysts' expectations in Q1 CY2024, with revenue down 3.2% year on year to $1.40 billion. The company also expects next quarter's revenue to be around $1.33 billion, coming in 3% above analysts' estimates. It made a GAAP loss of $17.02 per share, down from its loss of $3.62 per share in the same quarter last year.

Is now the time to buy Take-Two? Find out by accessing our full research report, it's free.

Take-Two (TTWO) Q1 CY2024 Highlights:

- Revenue: $1.40 billion vs analyst estimates of $1.35 billion (3.4% beat)

- Revenue Guidance for Q2 CY2024 is $1.33 billion at the midpoint, above analyst estimates of $1.29 billion

- Management's revenue guidance for the upcoming financial year 2025 is $5.62 billion at the midpoint, missing analyst estimates by 19.8% and implying 5.1% growth (vs 0.9% in FY2024)

- Free Cash Flow was -$55.1 million compared to -$112.6 million in the previous quarter

- Market Capitalization: $25.26 billion

"We concluded Fiscal 2024 with strong fourth quarter results, including Net Bookings of $1.35 billion, which exceeded the high-end of our guidance range. Many of our key franchises outperformed, including NBA 2K24; Zynga’s in-app purchases, led by Toon Blast and our newest hit, Match Factory!; the Red Dead Redemption series and the Grand Theft Auto series," said Strauss Zelnick, Chairman and CEO of Take-Two.

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ:TTWO) is one of the world’s largest video game publishers.

Video Gaming

Since videogames were invented in the 1970s, they have gradually taken more share of entertainment time. Ubiquitous mobile devices have powered a surge in “snackable” games that can be played on the go. Over time, games have developed more social engagement features where friends can play games together over the internet. The business models of games publishers have become less volatile due to digitization of distribution, in game monetization, and like Hollywood, an increasing dependence on surefire hit franchises. Covid driven lockdowns accelerated adoption and usage of videogames – a trend that has not slowed.

Sales Growth

Take-Two's revenue growth over the last three years has been mediocre, averaging 17.7% annually. This quarter, Take-Two beat analysts' estimates but reported a year on year revenue decline of 3.2%.

Guidance for the next quarter indicates Take-Two is expecting revenue to grow 3.1% year on year to $1.33 billion, slowing from the 16.5% year-on-year increase it recorded in the comparable quarter last year. For the upcoming financial year, management expects revenue to reach $5.62 billion at the midpoint, representing 5.1% growth compared to the 0.9% increase in FY2024.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Key Takeaways from Take-Two's Q1 Results

It was great to see Take-Two's optimistic revenue guidance for next quarter, which exceeded analysts' expectations. We were also glad its revenue outperformed Wall Street's estimates. On the other hand, its full-year revenue guidance missed analysts' expectations and its revenue growth was quite weak. Overall, this was a mediocre quarter for Take-Two. The company is down 4.2% on the results and currently trades at $140 per share.

Take-Two may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.