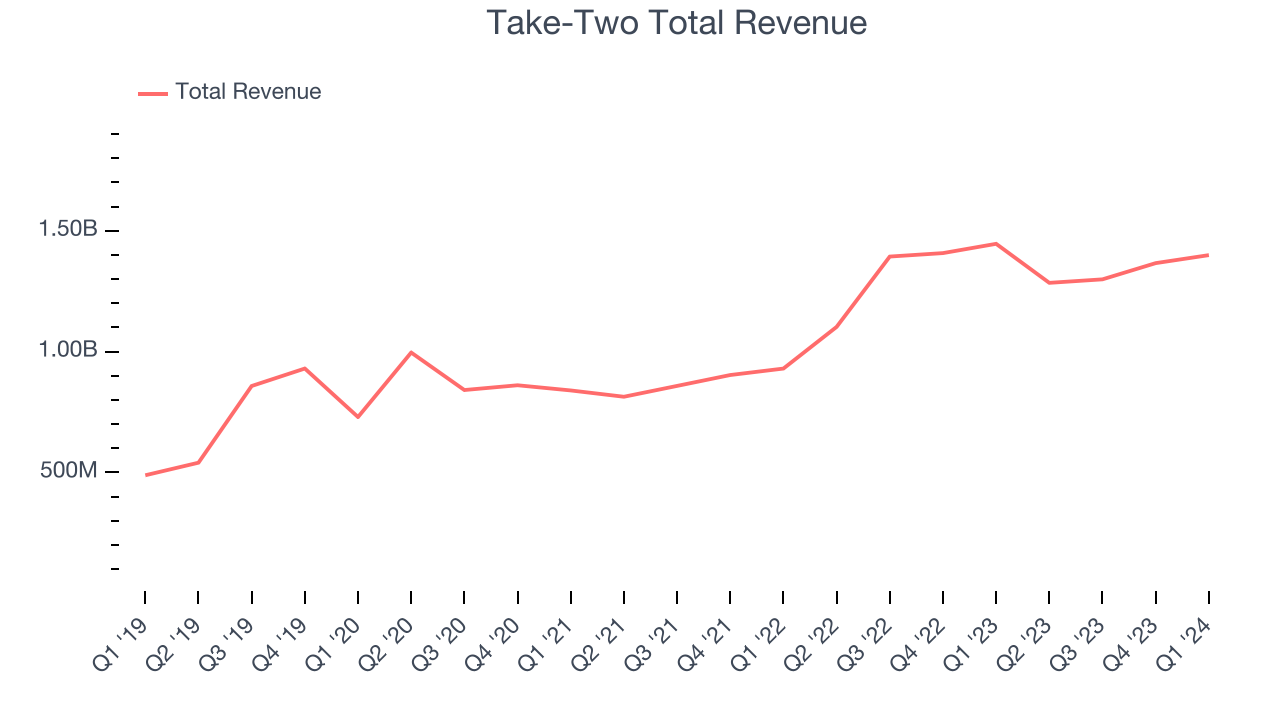

Video game publisher Take Two (NASDAQ:TTWO) reported Q1 CY2024 results topping analysts' expectations, with revenue down 3.2% year on year to $1.40 billion. The company also expects next quarter's revenue to be around $1.33 billion, coming in 3% above analysts' estimates.

Take-Two (TTWO) Q1 CY2024 Highlights:

- Revenue: $1.40 billion vs analyst estimates of $1.35 billion (3.4% beat)

- Revenue Guidance for Q2 CY2024 is $1.33 billion at the midpoint, above analyst estimates of $1.29 billion

- Management's revenue guidance for the upcoming financial year 2025 is $5.62 billion at the midpoint, missing analyst estimates by 19.8% and implying 5.1% growth (vs 0.9% in FY2024)

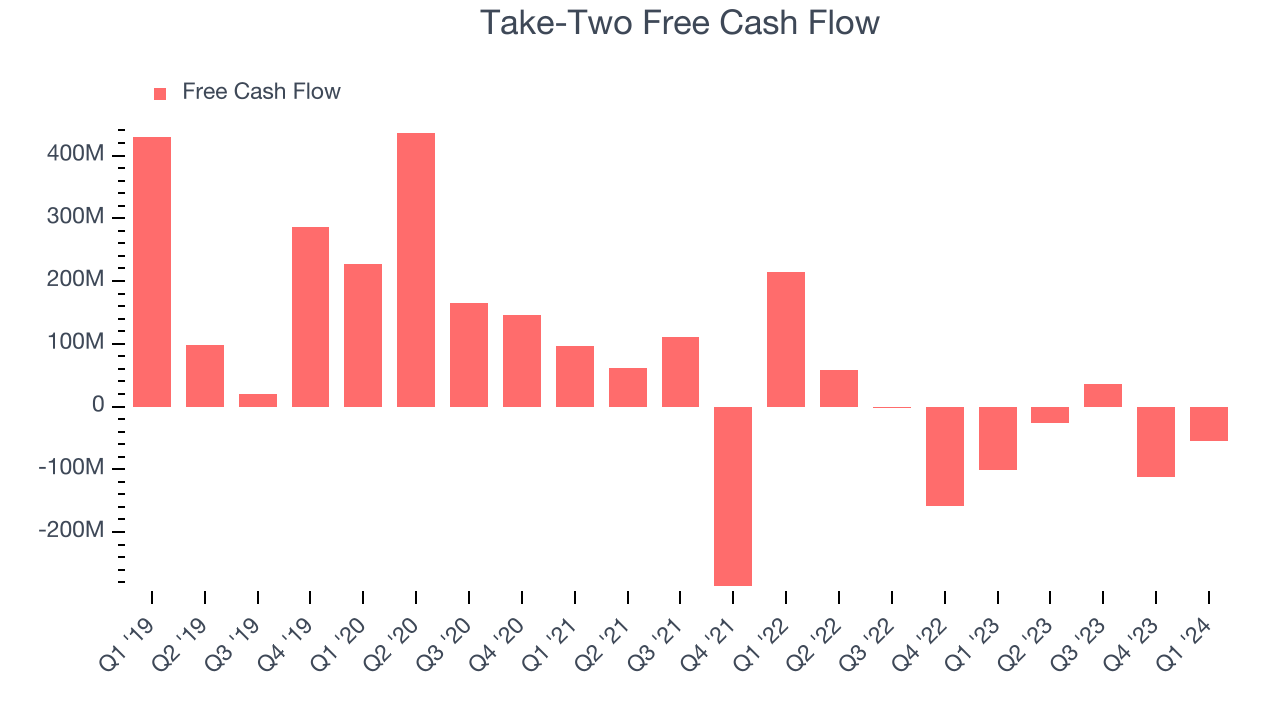

- Free Cash Flow was -$55.1 million compared to -$112.6 million in the previous quarter

- Market Capitalization: $25.26 billion

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ:TTWO) is one of the world’s largest video game publishers.

Take Two develops video games for consoles, PCs, and mobile devices through its five main development studios: Rockstar Games, 2K, Private Division, Social Point, and Playdots. Take Two’s games range across multiple genres, from first person shooter, action, role-playing, strategy, sports and family/casual entertainment. It also employs a range of business models; Take Two sells full premium games along with free to play games with in game purchase, and subscription style content.

Unlike rivals EA and Activision, whose businesses are built on big releases of annualized content like Madden or Call of Duty, some of Take Two’s biggest franchises are released less frequently, with the company often taking years to develop new versions. Its biggest franchise, Grand Theft Auto’s last release was September 2013, while the October 2018 release of Red Dead Redemption II was in development for 8 years. Its NBA 2K series is its only major title with an annual release. The company also has a collection of mid-tier franchises that have more regular releases such as Bioshock, Borderlands, Mafia, and Sid Meier’s Civilization.

Video Gaming

Since videogames were invented in the 1970s, they have gradually taken more share of entertainment time. Ubiquitous mobile devices have powered a surge in “snackable” games that can be played on the go. Over time, games have developed more social engagement features where friends can play games together over the internet. The business models of games publishers have become less volatile due to digitization of distribution, in game monetization, and like Hollywood, an increasing dependence on surefire hit franchises. Covid driven lockdowns accelerated adoption and usage of videogames – a trend that has not slowed.

Take Two competes with other large video game companies such as Electronic Arts (NASDAQ:EA), Roblox (NYSE:RBLX), and Nintendo (TSE:7974).

Sales Growth

Take-Two's revenue growth over the last three years has been mediocre, averaging 17.7% annually. This quarter, Take-Two beat analysts' estimates but reported a year on year revenue decline of 3.2%.

Guidance for the next quarter indicates Take-Two is expecting revenue to grow 3.1% year on year to $1.33 billion, slowing from the 16.5% year-on-year increase it recorded in the comparable quarter last year. For the upcoming financial year, management expects revenue to reach $5.62 billion at the midpoint, representing 5.1% growth compared to the 0.9% increase in FY2024.

User Acquisition Efficiency

Consumer internet businesses like Take-Two grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It's very expensive for Take-Two to acquire new users as the company has spent 64% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between Take-Two and its peers.

Profitability & Free Cash Flow

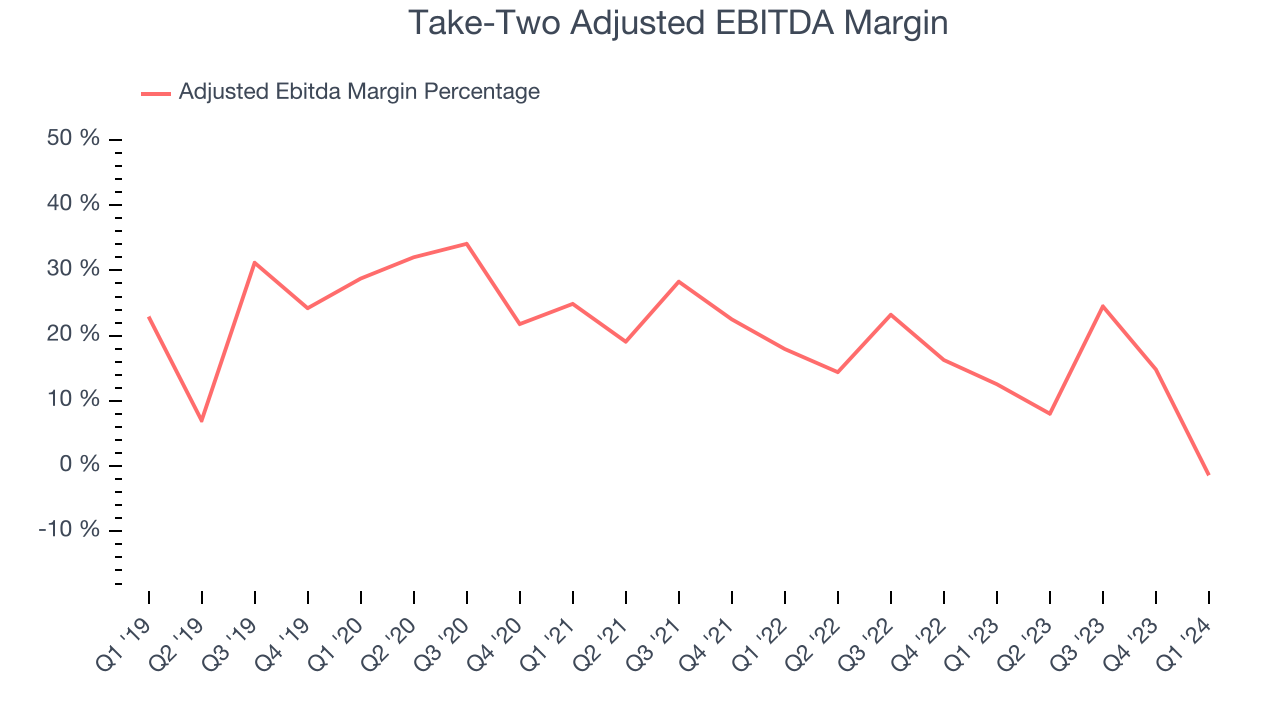

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

Take-Two's EBITDA was negative $19.6 million this quarter, translating into a negative 1.4% margin. The company has also shown above-average profitability for a consumer internet business over the last four quarters, with average EBITDA margins of 11.3%.

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Take-Two burned through $55.1 million in Q1, increasing the cash burn by 45.6% year on year.

Take-Two has burned through $157.8 million of cash over the last 12 months, resulting in a negative 2.9% free cash flow margin. This below-average FCF margin stems from Take-Two's continuous need to reinvest in its business to penetrate the market.

Key Takeaways from Take-Two's Q1 Results

It was great to see Take-Two's optimistic revenue guidance for next quarter, which exceeded analysts' expectations. We were also glad its revenue outperformed Wall Street's estimates. On the other hand, its full-year revenue guidance missed analysts' expectations and its revenue growth was quite weak. Overall, the results could have been better. The company is down 4.2% on the results and currently trades at $139.91 per share.

Is Now The Time?

When considering an investment in Take-Two, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although we have other favorites, we understand the arguments that Take-Two isn't a bad business. We'd expect growth rates to moderate from here, but its revenue growth has been decent over the last three years. However, its sales and marketing spend is very high compared to other consumer internet businesses and gross margins indicate a disadvantaged starting point for the overall profitability of the business.

At the moment, Take-Two trades at 17.2x next 12 months EV-to-EBITDA. There are things to like about Take-Two and there's no doubt it's a bit of a market darling, at least for some. But it seems there's a lot of optimism already priced in and we wonder whether there might be better opportunities elsewhere.

Wall Street analysts covering the company had a one-year price target of $177.75 per share right before these results (compared to the current share price of $139.91).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.