The end of an earnings season can be a great time to assess how companies are handling the current business environment and discover new stocks. Let’s have a look at how 2U (NASDAQ:TWOU) and the rest of the vertical software stocks fared in Q4.

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, there are industries that have very specific needs. Whether it is life-sciences, education or banking, the demand for so called vertical software, addressing industry specific workflows, is growing, fueled by the pressures on improving productivity and quality of offerings.

The 12 vertical software stocks we track reported a mixed Q4; on average, revenues beat analyst consensus estimates by 4.87%, while on average next quarter revenue guidance was 2.19% above consensus. Tech stocks have been under pressure since the end of last year and while some of the vertical software stocks have fared somewhat better, they have not been spared, with share price declining 17.1% since earnings, on average.

Weakest Q4: 2U (NASDAQ:TWOU)

Originally named 2tor after the founder's dog Tor, 2U (NASDAQ:TWOU) provides software for universities and colleges to deliver online degree programs and courses.

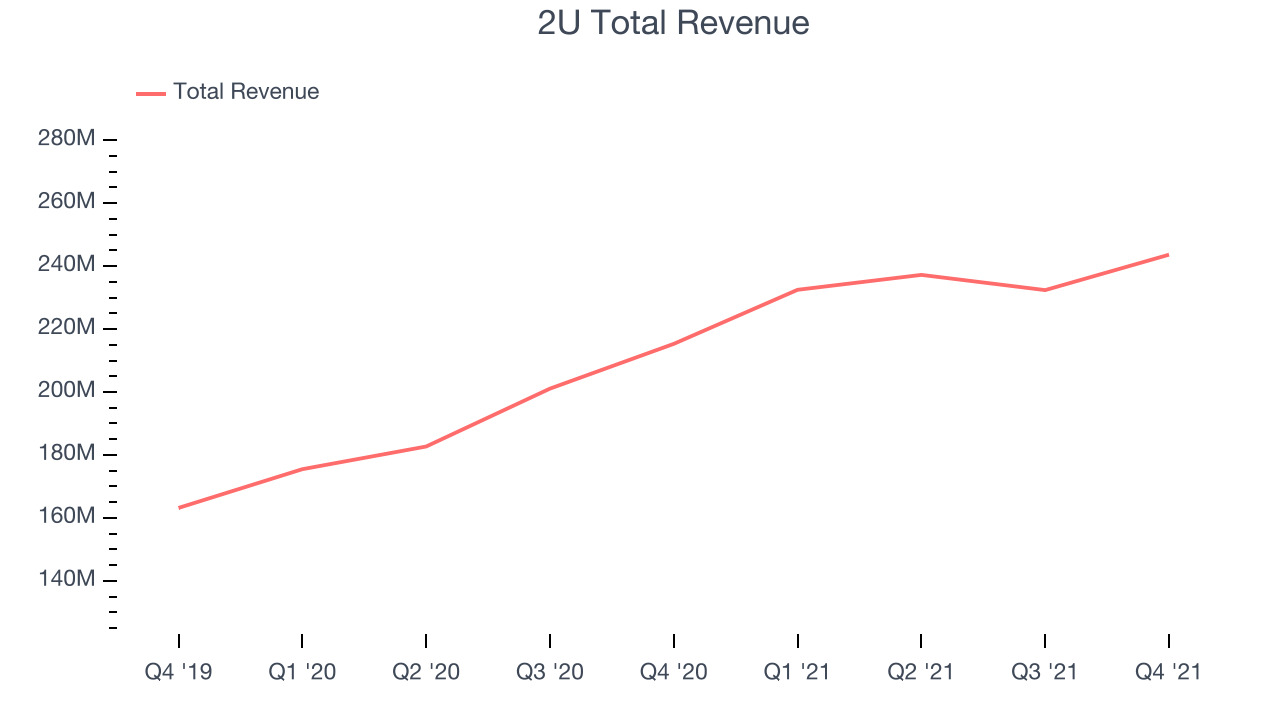

2U reported revenues of $243.6 million, up 13.1% year on year, in line with analyst expectations. It was a weak quarter for the company, with a decline in gross margin and full year revenue guidance missing analysts' expectations.

"Our strong 2021 results were led by healthy revenue growth in both our degree and alternative credential business, with demand for our undergraduate offerings particularly compelling," said Christopher "Chip" Paucek, 2U's Co-Founder and Chief Executive Officer.

2U delivered the weakest full year guidance update of the whole group. The stock is down 38.4% since the results and currently trades at $11.06.

Read our full report on 2U here, it's free.

Best Q4: Doximity (NYSE:DOCS)

Founded in 2010 and named for a combination of “docs” and “proximity”, Doximity (NYSE: DOCS) is the leading professional network for U.S. medical professionals.

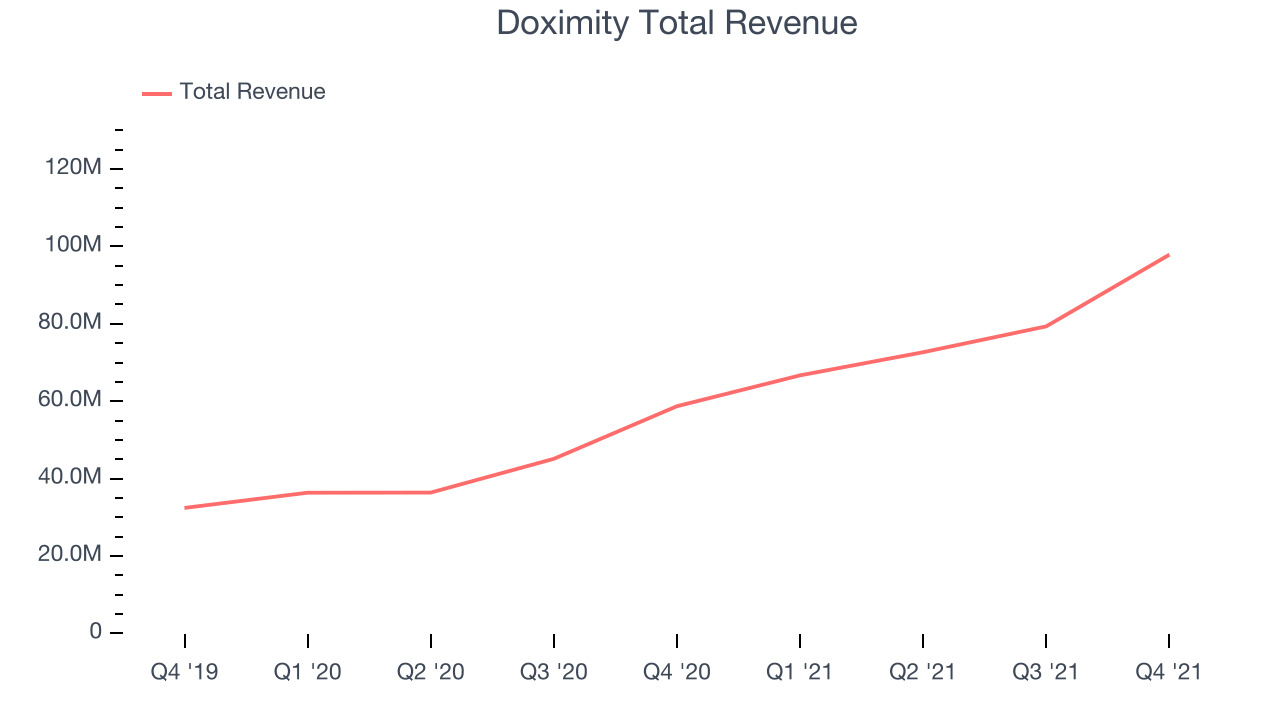

Doximity reported revenues of $97.8 million, up 66.7% year on year, beating analyst expectations by 13.4%. It was a stunning quarter for the company, with a very optimistic guidance for the next quarter and an exceptional revenue growth.

The stock is up 2.4% since the results and currently trades at $51.

Is now the time to buy Doximity? Access our full analysis of the earnings results here, it's free.

Q2 Holdings (NYSE:QTWO)

Founded in 2004 by Hank Seale, Q2 (NYSE:QTWO) offers software as a service that enables small banks provide online banking and consumer lending services to their clients.

Q2 Holdings reported revenues of $131.8 million, up 21% year on year, missing analyst expectations by 0.19%. It was a weak quarter for the company, with the guidance for both the next quarter and the full year missing analyst estimates.

Q2 Holdings had the weakest performance against analyst estimates in the group. The stock is down 11.9% since the results and currently trades at $58.31.

Read our full analysis of Q2 Holdings's results here.

Veeva Systems (NYSE:VEEV)

Built on top of Salesforce as one of the first vertical-focused cloud platforms, Veeva (NYSE:VEEV) provides data and customer relationship management (CRM) software for organizations in the life sciences industry.

Veeva Systems reported revenues of $485.4 million, up 22.3% year on year, beating analyst expectations by 1.08%. It was a weaker quarter for the company, with the guidance for both the next quarter and the full year missing analyst estimates.

The company added 205 customers to a total of 1,205. The stock is down 14.3% since the results and currently trades at $197.98.

Read our full, actionable report on Veeva Systems here, it's free.

Toast (NYSE:TOST)

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE:TOST) provides integrated point of sale (POS) hardware, software, and payments solutions for restaurants.

Toast reported revenues of $512 million, up 111% year on year, beating analyst expectations by 4.93%. It was a decent quarter for the company, with an exceptional revenue growth but an underwhelming guidance for the next year.

The stock is down 28.8% since the results and currently trades at $20.01.

Read our full, actionable report on Toast here, it's free.

The author has no position in any of the stocks mentioned