Online education platform, 2U (NASDAQ:TWOU) will be reporting results tomorrow after market close. Here's what investors should know.

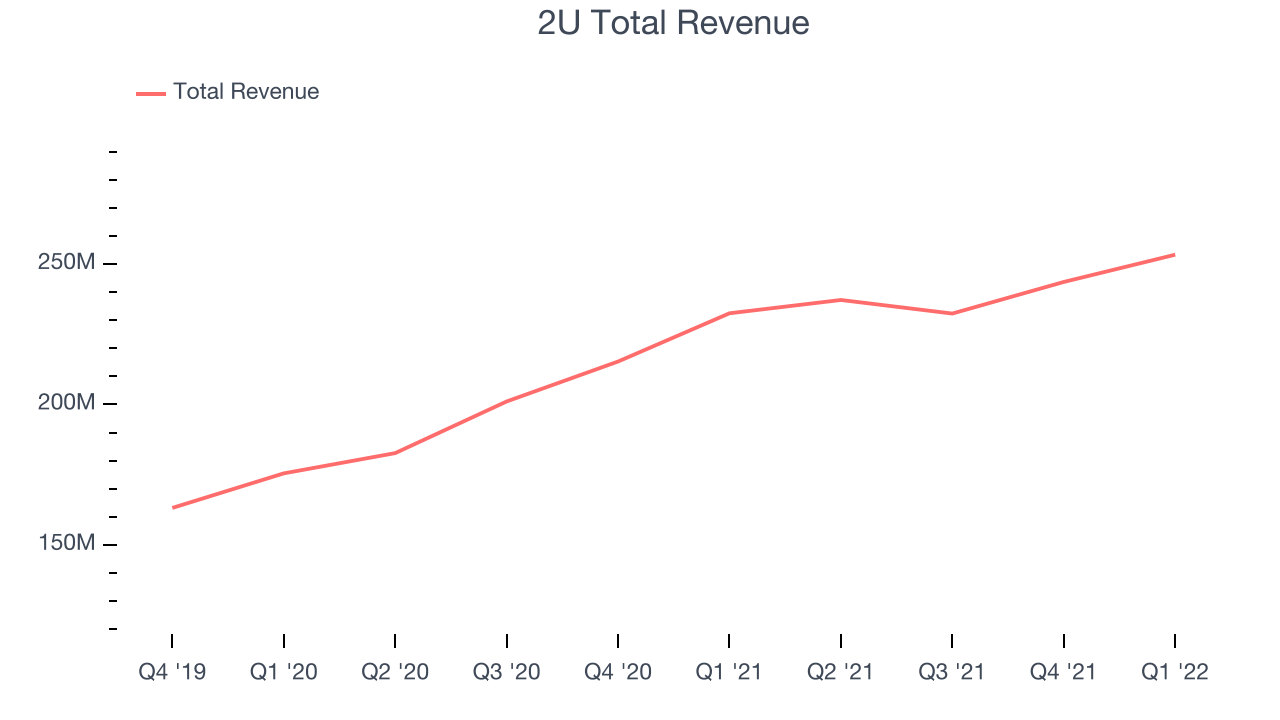

Last quarter 2U reported revenues of $253.3 million, up 8.97% year on year, in line with analyst expectations. It was a weaker quarter for the company, with a slow revenue growth and a decline in gross margin.

Is 2U buy or sell heading into the earnings? Read our full analysis here, it's free.

This quarter analysts are expecting 2U's revenue to grow 7.18% year on year to $254.2 million, slowing down from the 29.8% year-over-year increase in revenue the company had recorded in the same quarter last year. Adjusted loss is expected to come in at -$0.17 per share.

Majority of analysts covering the company have reconfirmed their estimates over the last thirty days, suggesting they are expecting the business to stay the course heading into the earnings. The company has a history of exceeding Wall St's expectations, beating revenue estimates every single time over the past two years on average by 2.76%.

With 2U being the first among its peers to report earnings this season, we don't have anywhere else to look at to get a hint at how this quarter will unravel for vertical software stocks. The whole tech sector has been facing a sell-off since late last year and while some of the sales and marketing software stocks have fared somewhat better, they have not been spared, with share price declining 10.6% over the last month. 2U is down 14.6% during the same time, and is heading into the earnings with analyst price target of $17.3, compared to share price of $8.83.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.