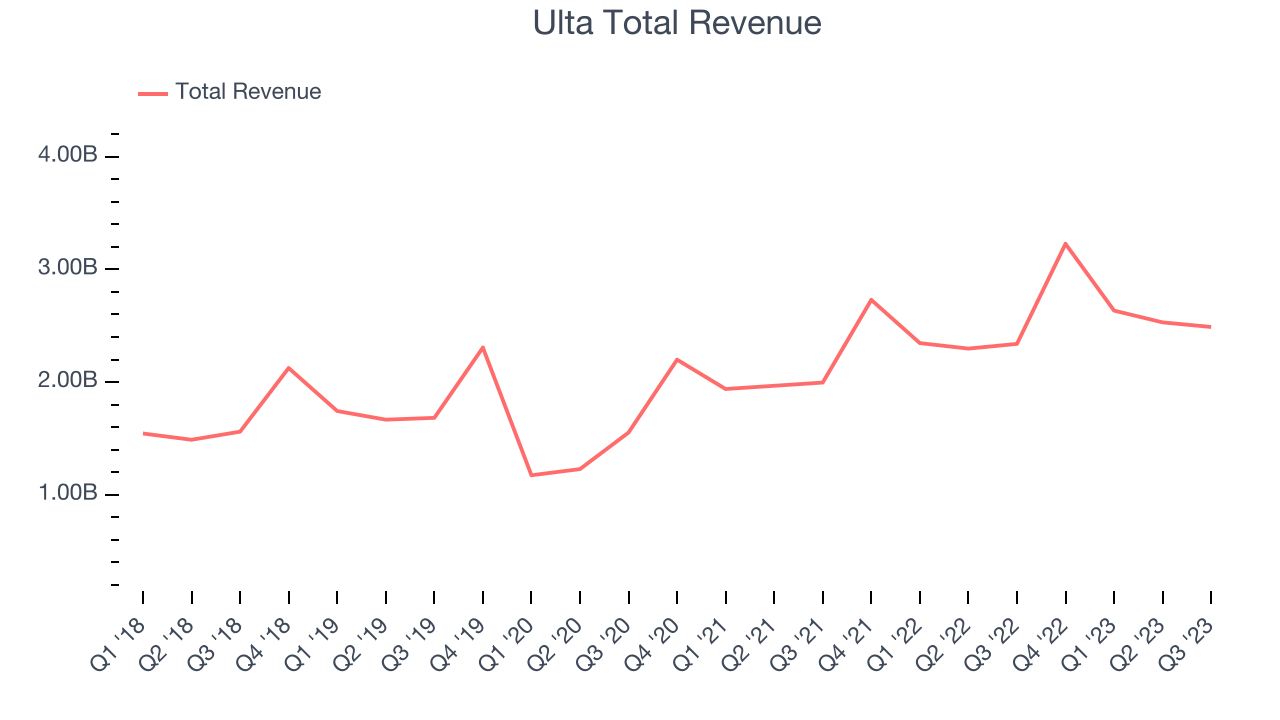

Beauty, cosmetics, and personal care retailer Ulta Beauty (NASDAQ:ULTA) reported results in line with analysts' expectations in Q3 FY2023, with revenue up 6.4% year on year to $2.49 billion. On the other hand, the company's full-year revenue guidance of $11.13 billion at the midpoint came in slightly below analysts' estimates. It made a GAAP profit of $5.07 per share, down from its profit of $5.34 per share in the same quarter last year.

Is now the time to buy Ulta? Find out by accessing our full research report, it's free.

Ulta (ULTA) Q3 FY2023 Highlights:

- Revenue: $2.49 billion vs analyst estimates of $2.47 billion (small beat)

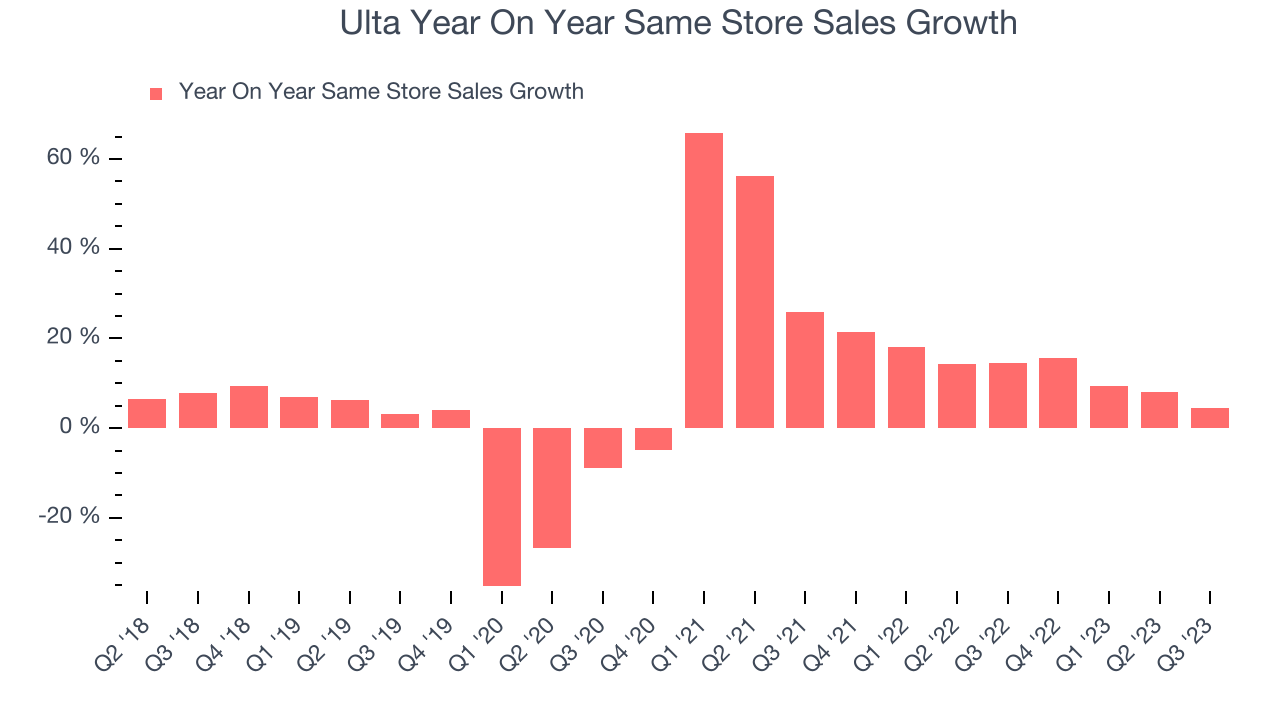

- Same-Store Sales were up 4.5% year on year (beat vs. expectations of up 3.1% year on year)

- EPS: $5.07 vs analyst estimates of $4.97 (1.9% beat)

- The company slightly raised its revenue guidance for the full year , $11.13 billion at the midpoint (also raised same-store sales and EPS guidance)

- Free Cash Flow was -$177.1 million compared to -$50.7 million in the same quarter last year

- Gross Margin (GAAP): 39.9%, down from 41.2% in the same quarter last year (slight beat)

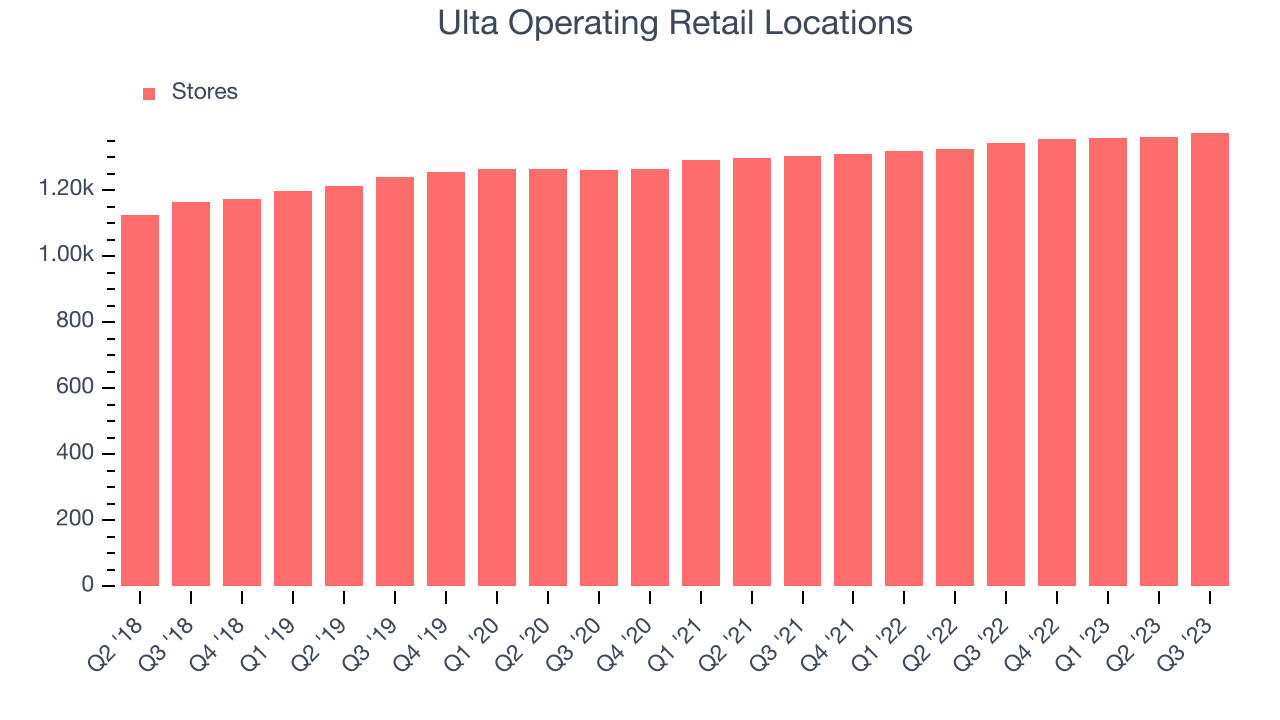

- Store Locations: 1,374 at quarter end, increasing by 31 over the last 12 months

“The third quarter represented another strong performance by the Ulta Beauty team, as sales, gross profit, and diluted EPS all exceeded our internal expectations. Our traffic trends remained healthy, our brand awareness increased, and we expanded our loyalty program to a record 42.2 million members,” said Dave Kimbell, chief executive officer.

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ:ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Beauty and Cosmetics Retailer

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Sales Growth

Ulta is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 10.8% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it opened new stores and grew sales at existing, established stores.

This quarter, Ulta grew its revenue by 6.4% year on year, in line with Wall Street's estimates. in line with Wall Street's expectations. Looking ahead, analysts expect sales to grow 6.5% over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Number of Stores

A retailer's store count is a crucial factor influencing how much it can sell, and store growth is a critical driver of how quickly its sales can grow.

When a retailer like Ulta is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, Ulta's store count increased by 31 locations, or 2.3%, to 1,374 total retail locations in the most recently reported quarter.

Taking a step back, the company has generally opened new stores over the last eight quarters, averaging 2.9% annual growth in its physical footprint. This is decent store growth and in line with other retailers. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Ulta's demand has outpaced the broader consumer retail sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 13.2% year on year. This performance suggests that its steady rollout of new stores could be beneficial for shareholders. When a company has strong demand, more locations should help it reach more customers seeking its products.

In the latest quarter, Ulta's same-store sales rose 4.5% year on year. By the company's standards, this growth was a meaningful deceleration from the 14.6% year-on-year increase it posted 12 months ago. We'll be watching Ulta closely to see if it can reaccelerate growth.

Key Takeaways from Ulta's Q3 Results

With a market capitalization of $20.68 billion, a $121.8 million cash balance, and positive free cash flow over the last 12 months, we're confident that Ulta has the resources needed to pursue a high-growth business strategy.

Same-store sales posted a convincing beat, although revenue only narrowly topped expectations this quarter. Profitability was sound, leading to a nice EPS beat in the quarter. The company raised its full year outlook for important metrics such as same-store sales, revenue, and EPS. Finally, management commentary in the release was optimistic, citing healthy traffic trends and a good setup for the important holiday shopping season. Zooming out, we think this was a solid quarter, showing that the company is staying on target. The stock is up 9.4% after reporting and currently trades at $466.03 per share.

So should you invest in Ulta right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.