AI lending platform Upstart (NASDAQ:UPST) reported Q4 FY2023 results beating Wall Street analysts' expectations, with revenue down 4.5% year on year to $140.3 million. On the other hand, next quarter's revenue guidance of $125 million was less impressive, coming in 17.4% below analysts' estimates. It made a non-GAAP loss of $0.11 per share, improving from its loss of $0.25 per share in the same quarter last year.

Is now the time to buy Upstart? Find out by accessing our full research report, it's free.

Upstart (UPST) Q4 FY2023 Highlights:

- Revenue: $140.3 million vs analyst estimates of $135.3 million (3.7% beat)

- EPS (non-GAAP): -$0.11 vs analyst estimates of -$0.14

- Revenue Guidance for Q1 2024 is $125 million at the midpoint, below analyst estimates of $151.3 million

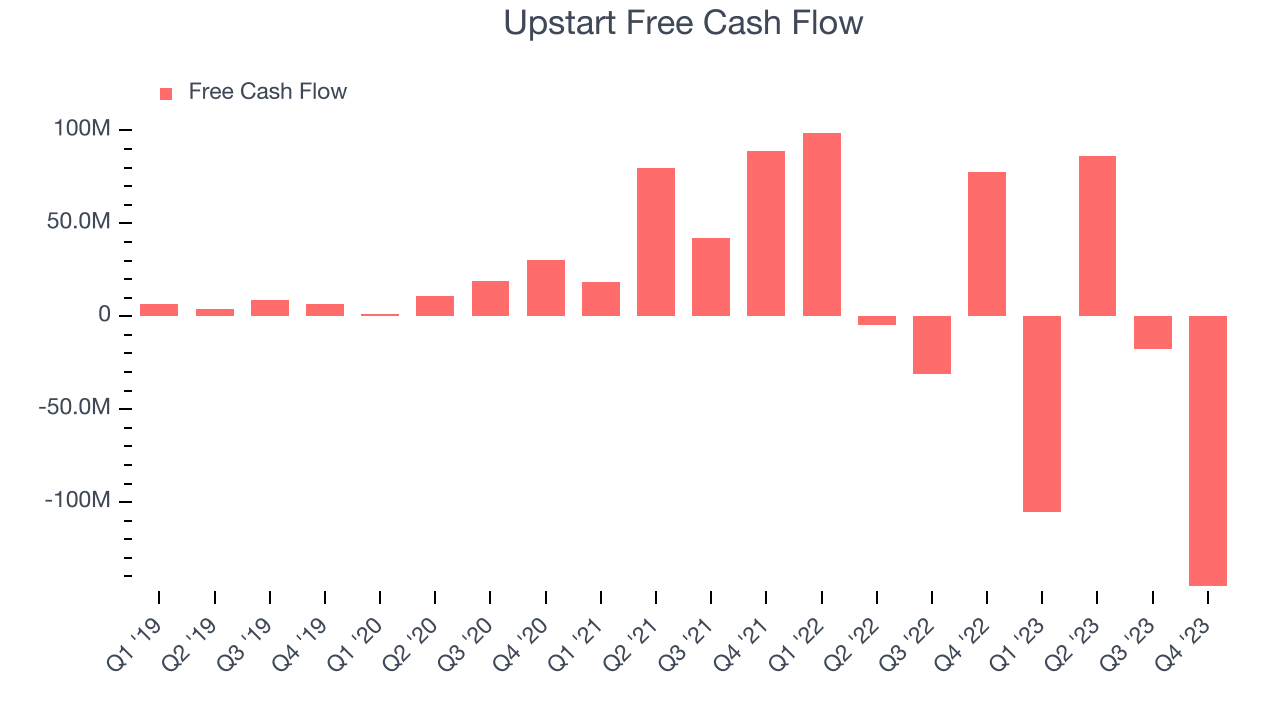

- Free Cash Flow was -$145.4 million compared to -$17.63 million in the previous quarter

- Gross Margin (GAAP): 59.3%, down from 70.4% in the same quarter last year

- Market Capitalization: $3.02 billion

Founded by the former head of Google's enterprise business Dave Girouard, Upstart (NASDAQ:UPST) is an AI-powered lending platform that helps banks better evaluate the risk of lending money to a person and provide loans to more customers.

Lending Software

Businesses have come to use data driven insights to stratify their customers into more granular buckets that enable more personalized (and profitable) offerings. Lending software is a prime example of fintech democratizing access to loans in a still-profitable manner for financial institutions.

Sales Growth

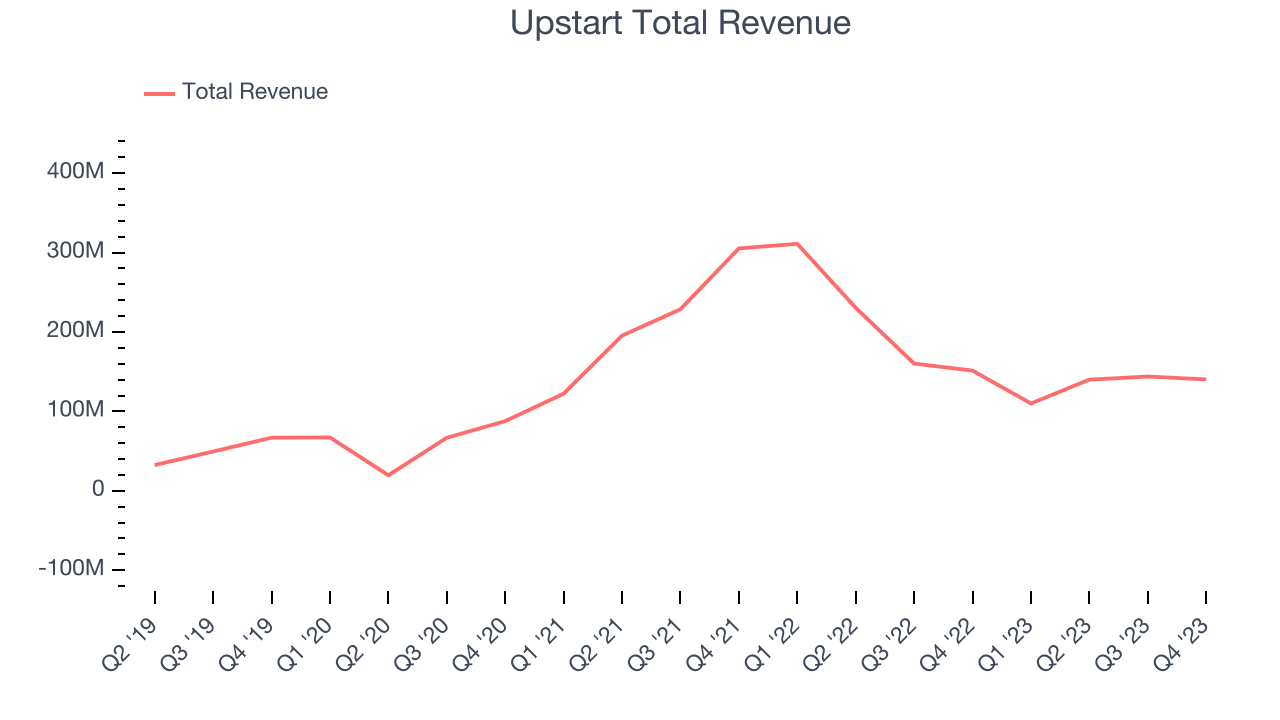

As you can see below, Upstart's revenue has been declining over the last two years, shrinking from $304.8 million in Q4 FY2021 to $140.3 million this quarter.

Upstart's revenue was down again this quarter, falling 4.5% year on year.

Next quarter's guidance suggests that Upstart is expecting revenue to grow 21.4% year on year to $125 million, improving on the 66.8% year-on-year decline it recorded in the same quarter last year.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Upstart burned through $145.4 million of cash in Q4 despite being cash flow positive in the same period last year.

Upstart has burned through $181.8 million of cash over the last 12 months, resulting in a negative 38.8% free cash flow margin. This low FCF margin stems from Upstart's poor unit economics or a constant need to reinvest in its business to stay competitive.

Key Takeaways from Upstart's Q4 Results

It was good to see Upstart beat analysts' revenue expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue guidance for next quarter missed analysts' expectations and cash burn increased. Overall, this was a mediocre quarter for Upstart. The stock is flat after reporting and currently trades at $32.89 per share.

Upstart may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.