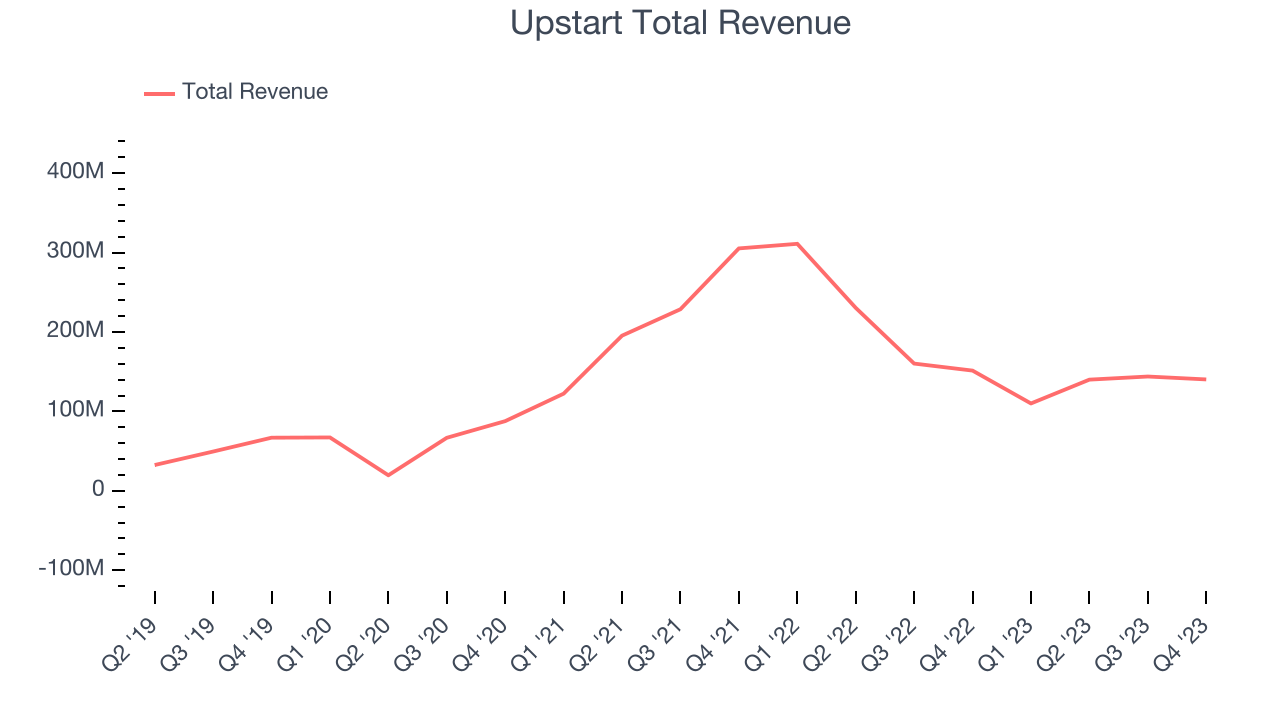

AI lending platform Upstart (NASDAQ:UPST) announced better-than-expected results in Q4 FY2023, with revenue down 4.5% year on year to $140.3 million. On the other hand, next quarter's revenue guidance of $125 million was less impressive, coming in 17.4% below analysts' estimates. It made a non-GAAP loss of $0.11 per share, improving from its loss of $0.25 per share in the same quarter last year.

Upstart (UPST) Q4 FY2023 Highlights:

- Revenue: $140.3 million vs analyst estimates of $135.3 million (3.7% beat)

- EPS (non-GAAP): -$0.11 vs analyst estimates of -$0.14

- Revenue Guidance for Q1 2024 is $125 million at the midpoint, below analyst estimates of $151.3 million

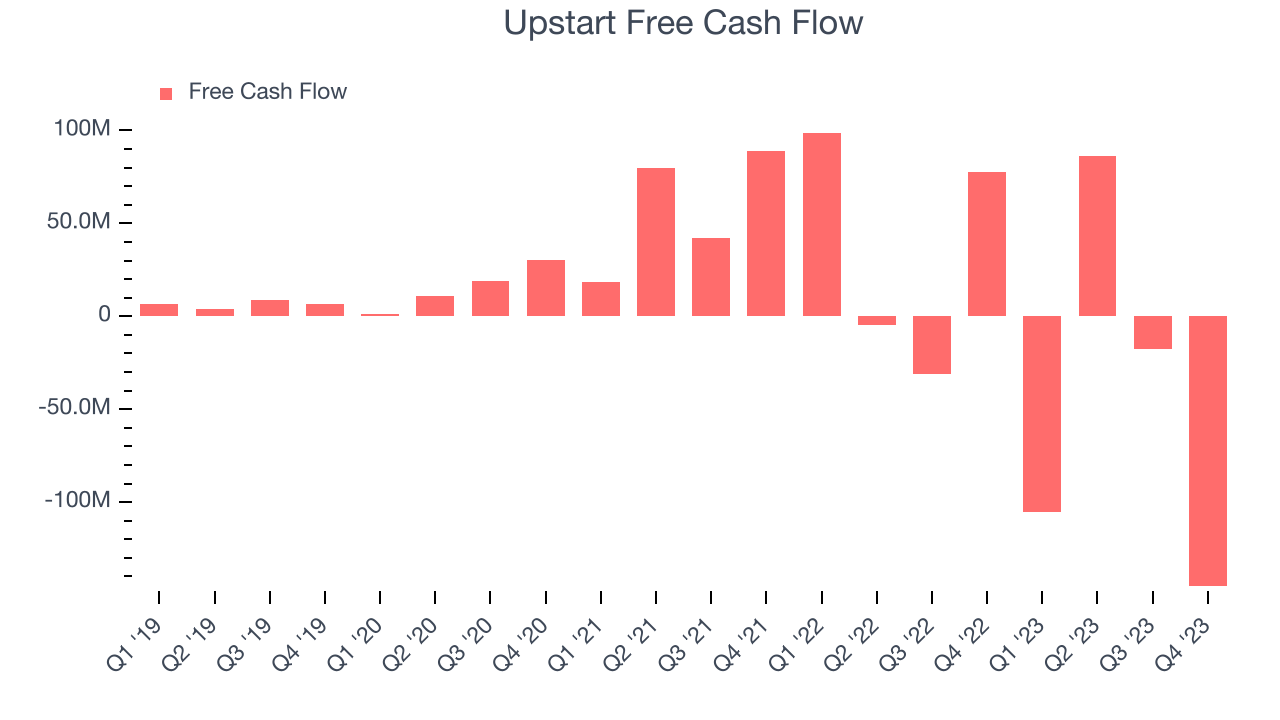

- Free Cash Flow was -$145.4 million compared to -$17.63 million in the previous quarter

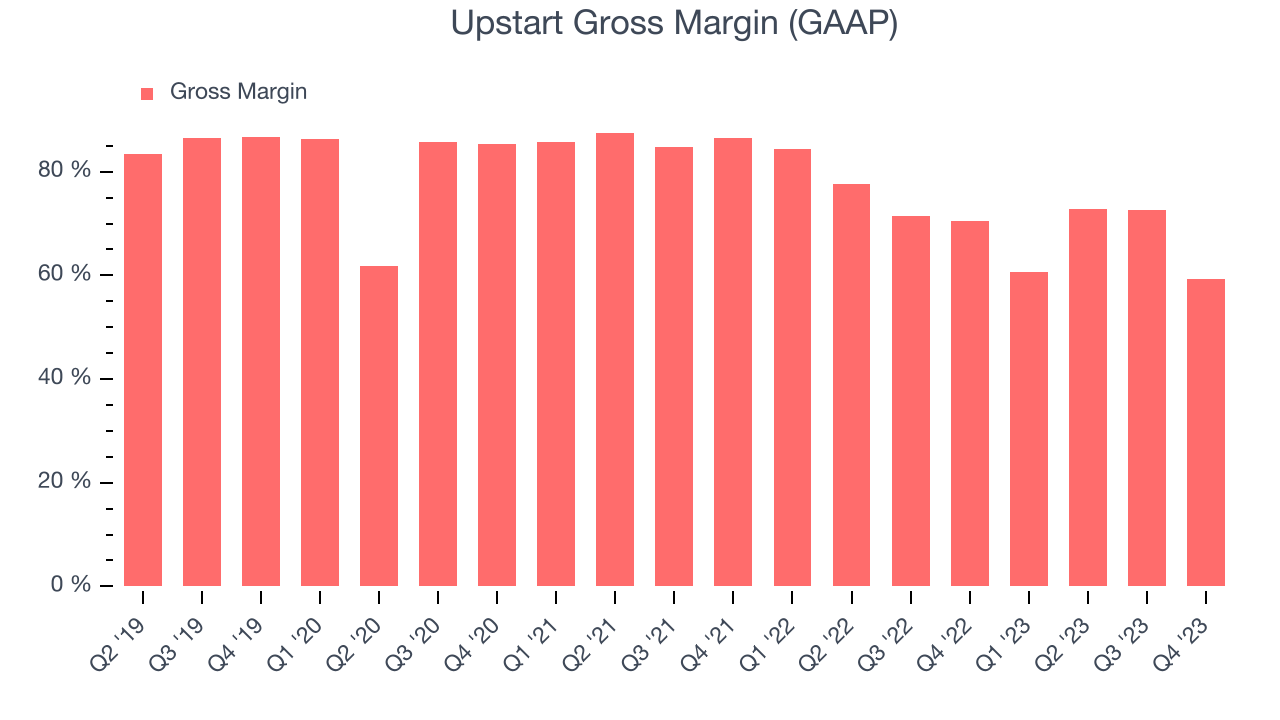

- Gross Margin (GAAP): 59.3%, down from 70.4% in the same quarter last year

- Market Capitalization: $3.02 billion

Founded by the former head of Google's enterprise business Dave Girouard, Upstart (NASDAQ:UPST) is an AI-powered lending platform that helps banks better evaluate the risk of lending money to a person and provide loans to more customers.

After a successful stint at Google where he started what later became Google Cloud, Dave Girouard founded Upstart together with his former colleague Anna Counselman and data scientist Paul Gu.

The ways lenders determine credit approvals in the US have not really changed in over 30 years and still rely mainly on FICO and simplistic rules-based systems. As a result, millions of creditworthy individuals who don’t fit into the precise brackets are either not approved for loans at all, or pay too much to borrow money. Upstart instead uses cloud-computing and machine learning to evaluate more than 1,000 data-points for each loan applicant, allowing them to estimate the risk of default on a loan more precisely, and for more people. For consumers, it means higher approval rates and lower interest rates and for banks it means access to new customers and lower fraud and loss rates. Because the decision is now made by software, it also means all-digital, automated experience from start to end.

Upstart provides their technology to banks and for some customers serves as an intermediary, but itself bears no credit risk and just simply charges the banks a fee for every provided loan. The company has started by evaluating applicants for personal loans, but their target market also includes auto loans, credit cards and mortgages.

Lending Software

Businesses have come to use data driven insights to stratify their customers into more granular buckets that enable more personalized (and profitable) offerings. Lending software is a prime example of fintech democratizing access to loans in a still-profitable manner for financial institutions.

Upstart’s main competitor would be FICO (NYSE:FICO), others somewhat related might include alternative lenders like Lending Tree (NASDAQ:TREE).

Sales Growth

As you can see below, Upstart's revenue has been declining over the last two years, shrinking from $304.8 million in Q4 FY2021 to $140.3 million this quarter.

Upstart's revenue was down again this quarter, falling 4.5% year on year.

Next quarter's guidance suggests that Upstart is expecting revenue to grow 21.4% year on year to $125 million, improving on the 66.8% year-on-year decline it recorded in the same quarter last year.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Upstart's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 59.3% in Q4.

That means that for every $1 in revenue the company had $0.59 left to spend on developing new products, sales and marketing, and general administrative overhead. Upstart's gross margin is poor for a SaaS business and it's dropped significantly since the previous quarter. This is probably the exact opposite of what shareholders would like to see.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Upstart burned through $145.4 million of cash in Q4 despite being cash flow positive in the same period last year.

Upstart has burned through $181.8 million of cash over the last 12 months, resulting in a negative 38.8% free cash flow margin. This low FCF margin stems from Upstart's poor unit economics or a constant need to reinvest in its business to stay competitive.

Key Takeaways from Upstart's Q4 Results

It was good to see Upstart beat analysts' revenue expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue guidance for next quarter missed analysts' expectations and the company burned through significant amount of cash. Overall, this was a mediocre quarter for Upstart. The stock is flat after reporting and currently trades at $32.89 per share.

Is Now The Time?

When considering an investment in Upstart, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in case of Upstart, we'll be cheering from the sidelines. Although its , Wall Street expects growth to deteriorate from here. On top of that, its customer acquisition is less efficient than many comparable companies and its growth is coming at a cost of significant cash burn.

Upstart's price-to-sales ratio based on the next 12 months is 4.3x, suggesting that the market does have lower expectations of the business, relative to the high growth tech stocks. While we have no doubt one can find things to like about the company, we think there might be better opportunities in the market and at the moment don't see many reasons to get involved.

Wall Street analysts covering the company had a one-year price target of $21.47 per share right before these results (compared to the current share price of $32.89), implying they didn't see much short-term potential in the Upstart.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.