Clothing and accessories retailer Urban Outfitters (NASDAQ:URBN) fell short of analysts' expectations in Q4 FY2024, with revenue up 7.3% year on year to $1.49 billion. It made a non-GAAP profit of $0.69 per share, improving from its profit of $0.34 per share in the same quarter last year.

Urban Outfitters (URBN) Q4 FY2024 Highlights:

- Revenue: $1.49 billion vs analyst estimates of $1.50 billion (1% miss)

- EPS (non-GAAP): $0.69 vs analyst expectations of $0.74 (7.3% miss)

- Gross Margin (GAAP): 29.9%, up from 27.3% in the same quarter last year

- Same-Store Sales were up 4.9% year on year (miss vs. expectations of up 5.4% year on year)

- Market Capitalization: $4.26 billion

Founded as a purveyor of vintage items, Urban Outfitters (NASDAQ:URBN) now largely sells new apparel and accessories to teens and young adults seeking on-trend fashion.

In addition to being trendy, the aesthetic tends to also be edgy and creative. Skaters and art students can be thought of as embodying the Urban Outfitters style. In addition to clothing and accessories such as beanies, socks, and bags, the company also sells unique items such as home decor and vinyl records to augment its aesthetic.

A typical Urban Outfitters store is roughly 10,000 square feet and located in both urban and suburban shopping centers as well as close to places with a high density of young consumers such as college campuses. The stores don’t usually follow typical retail layouts and are designed to be more edgy and nonconformist. There can be some initial difficulty navigating a store but the upside is more exploration and wandering.

In addition to the core Urban Outfitters brand, the company also operates Anthropologie and Free People. Anthropologie sells women’s clothing, accessories, and home decor featuring a bohemian aesthetic. Free People is a similar brand to Anthropologie but strictly focuses on apparel and accessories. All Urban Outfitters brands have an ecommerce presence that gives customers multiple ways to shop, return, and exchange merchandise.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Retailers offering casual yet trendy apparel for men, women, and children include H&M (OM:HMB), Inditex (BME:ITX) which owns Zara, Abercrombie & Fitch (NYSE:ANF), and American Eagle Outfitters (NYSE:AEO).Sales Growth

Urban Outfitters is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

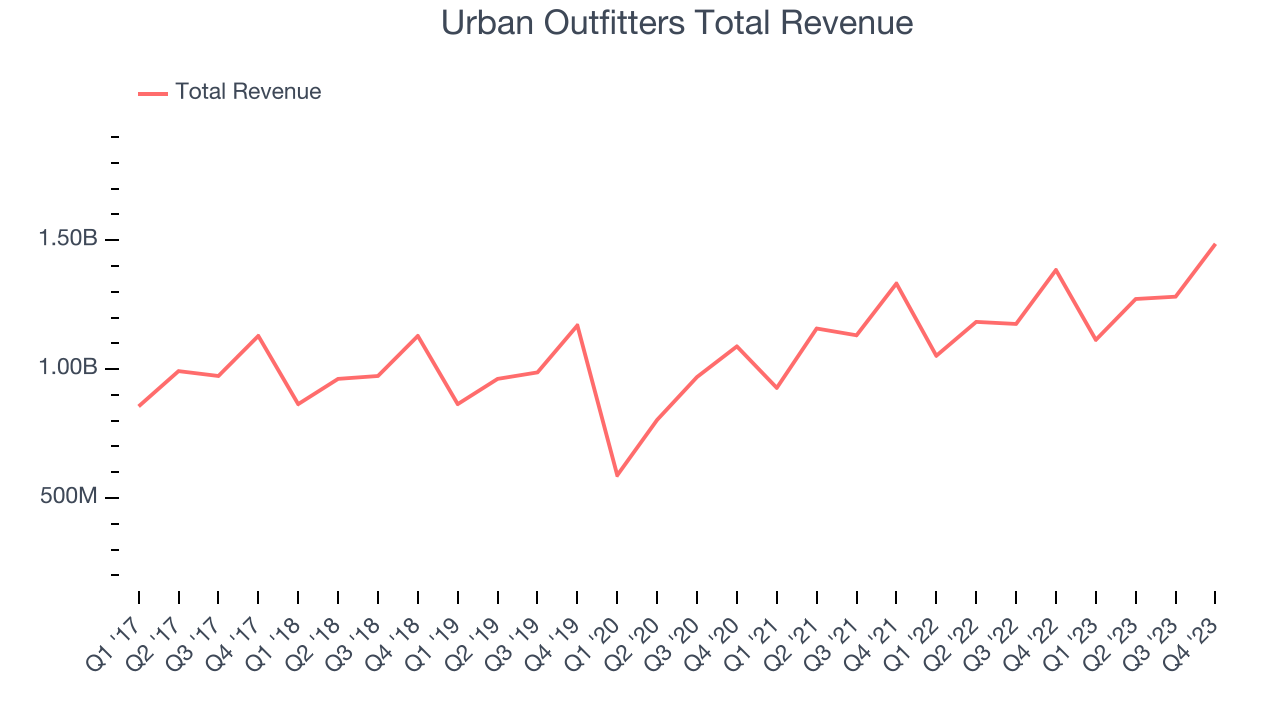

As you can see below, the company's annualized revenue growth rate of 6.6% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak , but to its credit, it opened new stores and grew sales at existing, established stores.

This quarter, Urban Outfitters's revenue grew 7.3% year on year to $1.49 billion, missing Wall Street's expectations. Looking ahead, Wall Street expects sales to grow 5.3% over the next 12 months, a deceleration from this quarter.

Same-Store Sales

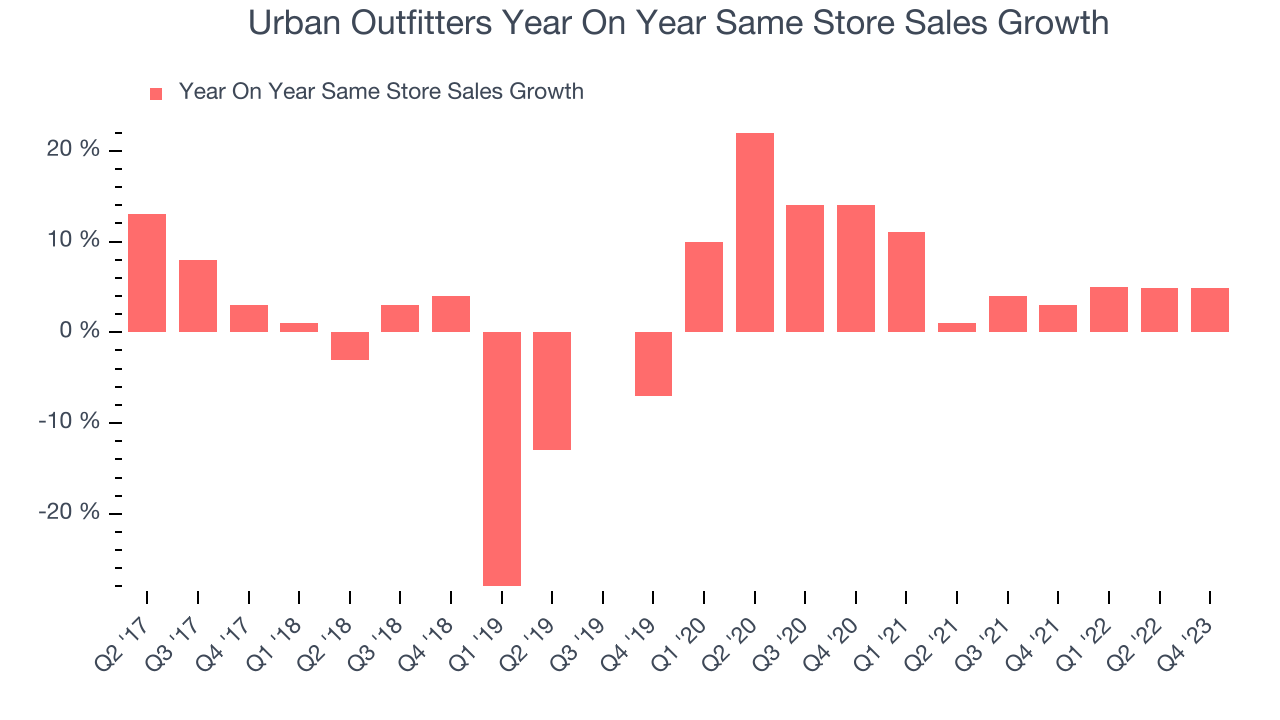

Same-store sales growth is a key performance indicator used to measure organic growth and demand for retailers.

Urban Outfitters's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 4.9% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Urban Outfitters is reaching more customers and growing sales.

In the latest quarter, Urban Outfitters's same-store sales rose 4.9% year on year. This growth was an acceleration from the 3% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Gross Margin & Pricing Power

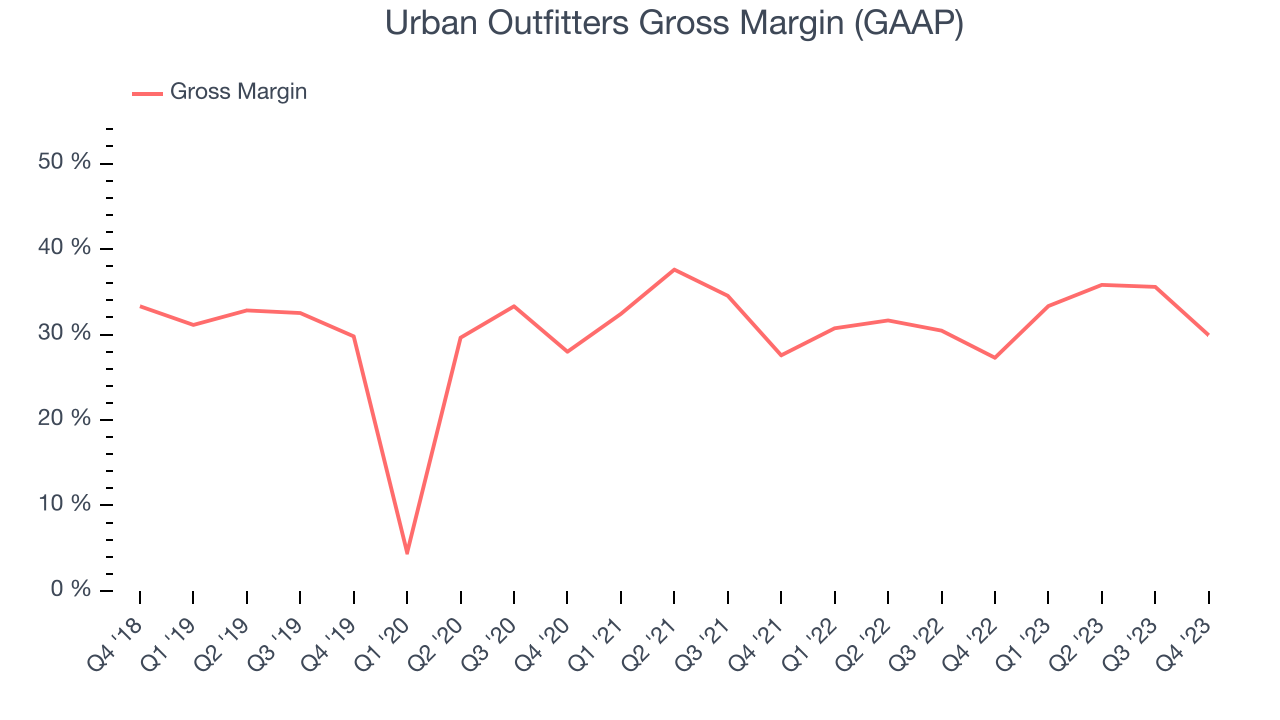

Urban Outfitters has weak unit economics for a retailer, making it difficult to reinvest in the business. As you can see below, it's averaged a 31.8% gross margin over the last eight quarters. This means the company makes $0.32 for every $1 in revenue before accounting for its operating expenses.

Urban Outfitters produced a 29.9% gross profit margin in Q4, marking a 2.6 percentage point increase from 27.3% in the same quarter last year. This margin expansion is a good sign in the near term. If this trend continues, it could signal a less competitive environment where the company has better pricing power, less pressure to discount products, and more stable input costs (such as distribution expenses to move goods).

Operating Margin

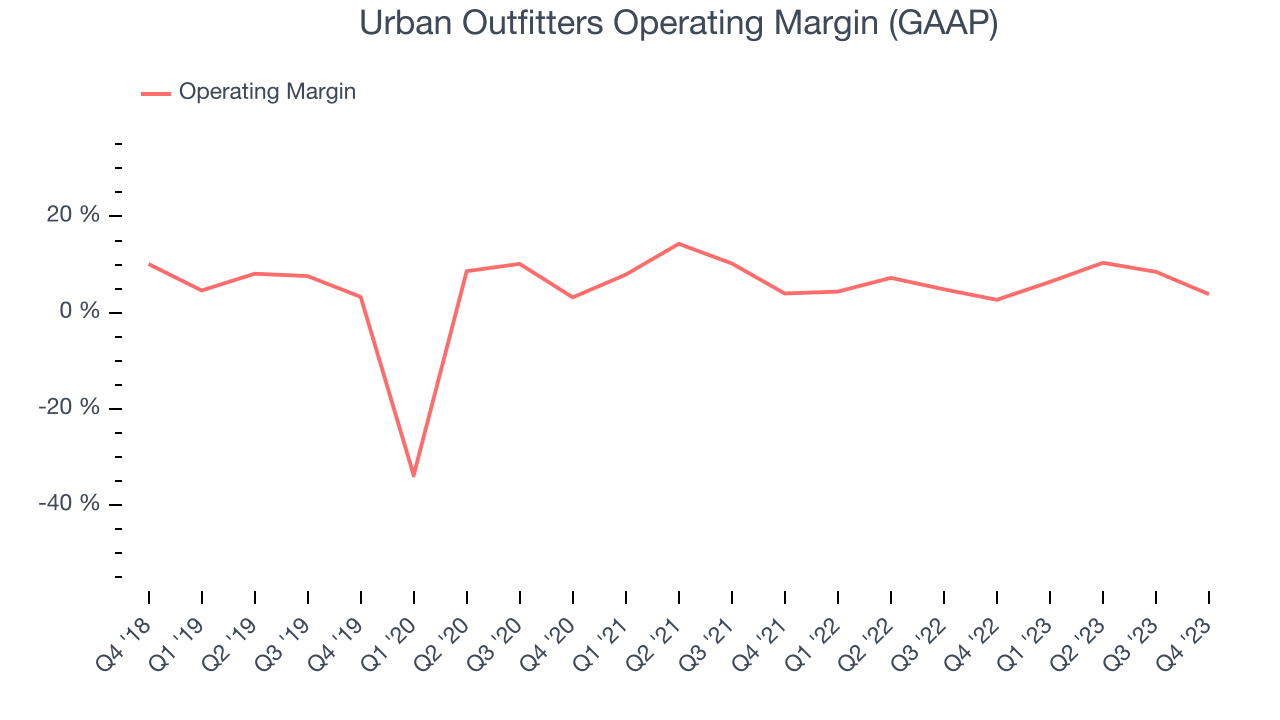

Operating margin is a key profitability metric for retailers because it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

In Q4, Urban Outfitters generated an operating profit margin of 3.9%, up 1.2 percentage points year on year. This increase was encouraging and driven by stronger pricing power, as indicated by the company's larger rise in gross margin.

Zooming out, Urban Outfitters was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer retail business, producing an average operating margin of 6%. However, Urban Outfitters's margin has improved, on average, by 2.4 percentage points year on year, an encouraging sign for shareholders. The tide could be turning.

Zooming out, Urban Outfitters was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer retail business, producing an average operating margin of 6%. However, Urban Outfitters's margin has improved, on average, by 2.4 percentage points year on year, an encouraging sign for shareholders. The tide could be turning.EPS

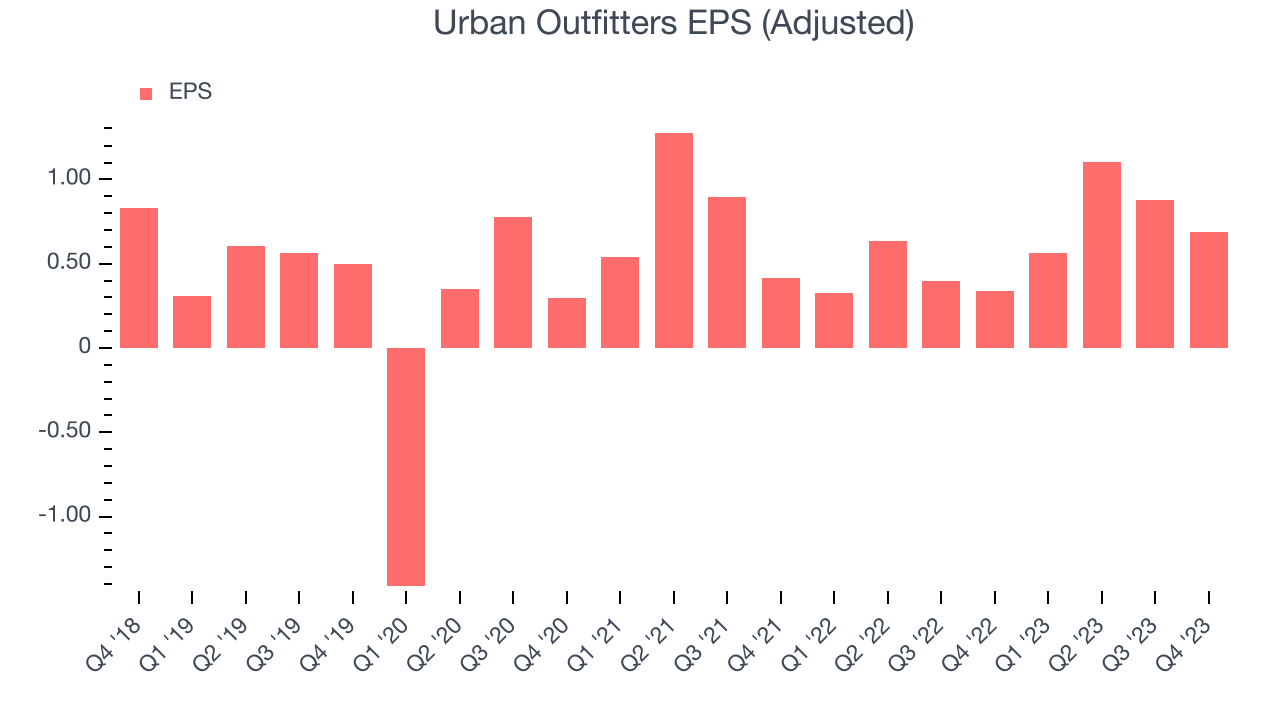

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q4, Urban Outfitters reported EPS at $0.69, up from $0.34 in the same quarter a year ago. This print unfortunately missed Wall Street's estimates, but we care more about long-term EPS growth rather than short-term movements.

Between FY2020 and FY2024, Urban Outfitters's adjusted diluted EPS grew 63.9%, translating into a decent 13.1% compounded annual growth rate. This growth is materially higher than its revenue growth over the same period and was driven by excellent expense management (leading to higher profitability) and share repurchases (leading to higher PER share earnings).

Wall Street expects the company to continue growing earnings over the next 12 months, with analysts projecting an average 8.7% year-on-year increase in EPS.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Urban Outfitters's five-year average ROIC was 8.4%, somewhat low compared to the best retail companies that consistently pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last two years, Urban Outfitters's ROIC averaged 7.5 percentage point increases each year. This is a good sign and we hope the company can continue to improving.

Key Takeaways from Urban Outfitters's Q4 Results

We struggled to find many strong positives in these results. Its same store sales, revenue, and gross margin missed analysts' expectations, leading to a bottom-line EPS miss vs. Wall Street's estimates. No guidance was given. Overall, this was a mixed quarter for Urban Outfitters. The company is down 6.3% on the results and currently trades at $44.2 per share.

Is Now The Time?

Urban Outfitters may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Urban Outfitters, we'll be cheering from the sidelines. Its revenue growth has been a little slower over the last four years. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its relatively low ROIC suggests it has struggled to grow profits historically. On top of that, its poor same-store sales performance has been a headwind.

Urban Outfitters's price-to-earnings ratio based on the next 12 months is 13.4x. While we've no doubt one can find things to like about Urban Outfitters, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $41.94 per share right before these results (compared to the current share price of $44.20), implying they didn't see much short-term potential in Urban Outfitters.

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.