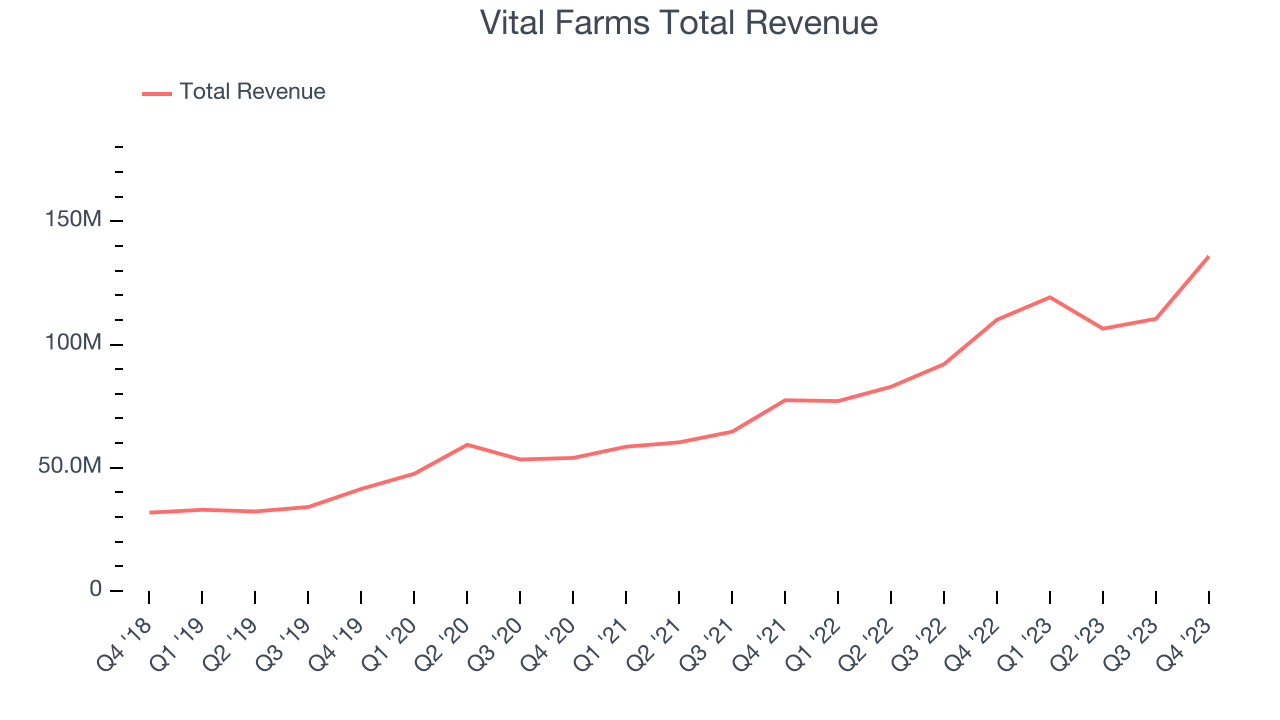

Egg and butter company Vital Farms (NASDAQ:NATR) beat analysts' expectations in Q4 FY2023, with revenue up 23.4% year on year to $135.8 million. The company expects the full year's revenue to be around $552 million, in line with analysts' estimates. It made a GAAP profit of $0.17 per share, improving from its profit of $0.05 per share in the same quarter last year.

Vital Farms (VITL) Q4 FY2023 Highlights:

- Revenue: $135.8 million vs analyst estimates of $131 million (3.7% beat)

- EPS: $0.17 vs analyst estimates of $0.07 ($0.10 beat)

- Management's revenue guidance for the upcoming financial year 2024 is $552 million at the midpoint, in line with analyst expectations and implying 17% growth (vs 31.6% in FY2023)

- Free Cash Flow of $21.33 million, up from $3.28 million in the previous quarter

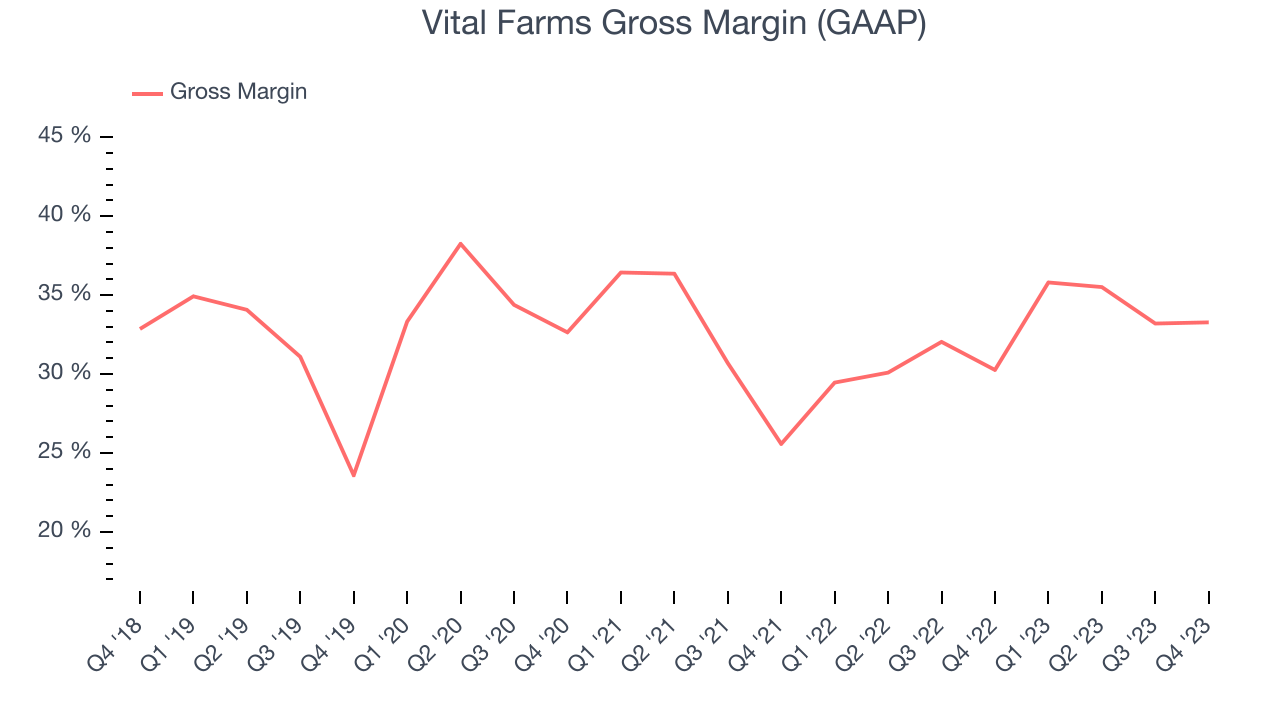

- Gross Margin (GAAP): 33.3%, up from 30.3% in the same quarter last year

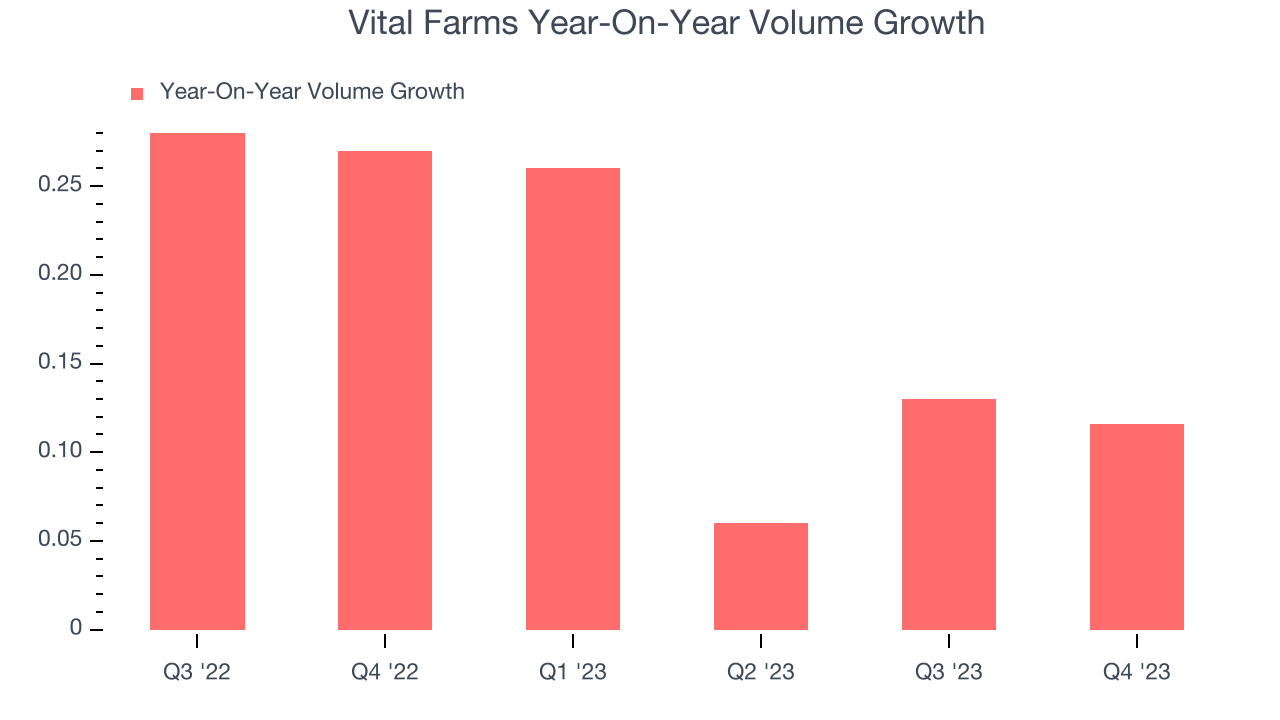

- Sales Volumes were up 11.6% year on year

- Market Capitalization: $790.4 million

With an emphasis on ethically produced products, Vital Farms (NASDAQ:NATR) specializes in pasture-raised eggs and butter.

The company was founded in 2007 by Matt O'Hare, who had a vision of transforming and championing ethical food practices. Vital Farms started with just 20 hens, and over the years, the company grew organically rather than through the acquisitions that are common for farm-based or agricultural businesses.

Today, Vital Farms is renowned for its pasture-raised eggs. Unlike conventional "free-range" or "cage-free" labels, pasture-raised labels mean that chickens genuinely spend significant time outdoors. Vital Farms also offers butter, egg bites, and ghee.

Vital Farms' core customer is the conscious consumer. This customer cares about where their food comes from, how it's produced, and the impact it has on the environment and animal welfare. These individuals often pay a premium for products they trust and believe in.

Vital Farms enjoys widespread distribution with its products stocked in national grocery chains and local health-conscious food stores.

Packaged Food

Packaged food stocks are considered resilient investments because people always need to eat. These companies therefore can enjoy consistent demand as long as they stay on top of changing consumer preferences. But consumer preferences can be a double-edged sword, as companies that aren't at the front of trends such as health and wellness and natural ingredients can fall behind. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Vital Farms has few scaled competitors as it operates in a commodity industry. Its main competitor is Cal-Maine Foods (NASDAQ:CALM), and private competitors include Rose Acre Farms and Hillandale Farms.Sales Growth

Vital Farms is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 30.1% over the last three years was incredible for a consumer staples business.

This quarter, Vital Farms reported remarkable year-on-year revenue growth of 23.4%, and its $135.8 million in revenue topped Wall Street estimates by 3.7%. Looking ahead, Wall Street expects sales to grow 16% over the next 12 months, a deceleration from this quarter.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Vital Farms's average quarterly volume growth of 18.6% over the last two years has beaten the competition by a long shot. This is great because companies with significant volume growth are needles in a haystack in the stable consumer staples sector.

In Vital Farms's Q4 2023, sales volumes jumped 11.6% year on year. By the company's standards, this result was a meaningful deceleration from the 27% year-on-year increase it posted 12 months ago. We'll be watching Vital Farms closely to see if it can reaccelerate demand for its products.

Gross Margin & Pricing Power

All else equal, we prefer higher gross margins. They usually indicate that a company sells more differentiated products and commands stronger pricing power.

This quarter, Vital Farms's gross profit margin was 33.3%, up 3 percentage points year on year. That means for every $1 in revenue, $0.67 went towards paying for raw materials, production of goods, and distribution expenses.

Vital Farms's unit economics are higher than the typical consumer staples company, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see above, it's averaged a decent 32.7% gross margin over the last eight quarters. Its margin has also been trending up over the last 12 months, averaging 13.3% year-on-year increases each quarter. If this trend continues, it could suggest a less competitive environment where the company has better pricing power and more favorable input costs (such as raw materials).

Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

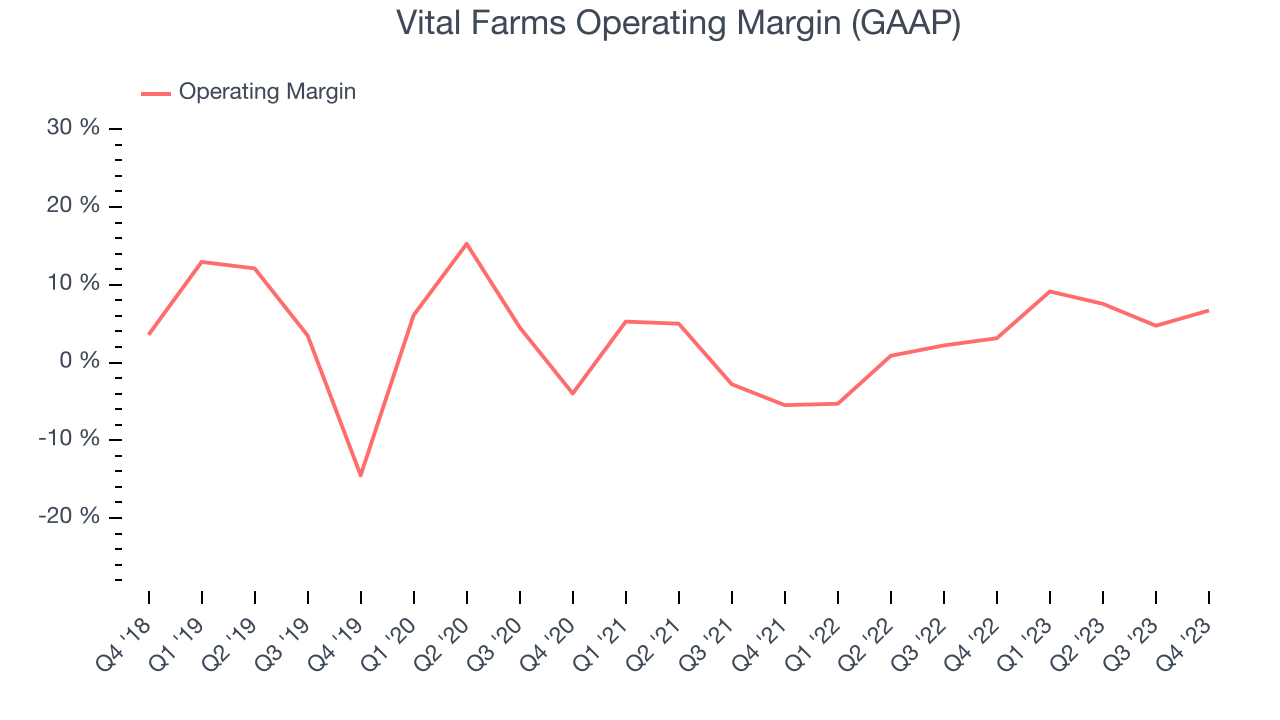

This quarter, Vital Farms generated an operating profit margin of 6.7%, up 3.6 percentage points year on year. This increase was encouraging, and we can infer Vital Farms was more efficient with its expenses because its operating margin expanded more than its gross margin.

Zooming out, Vital Farms was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 4.2%. However, Vital Farms's margin has improved by 6.5 percentage points on average over the last year, an encouraging sign for shareholders. The tide could be turning.

Zooming out, Vital Farms was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 4.2%. However, Vital Farms's margin has improved by 6.5 percentage points on average over the last year, an encouraging sign for shareholders. The tide could be turning.EPS

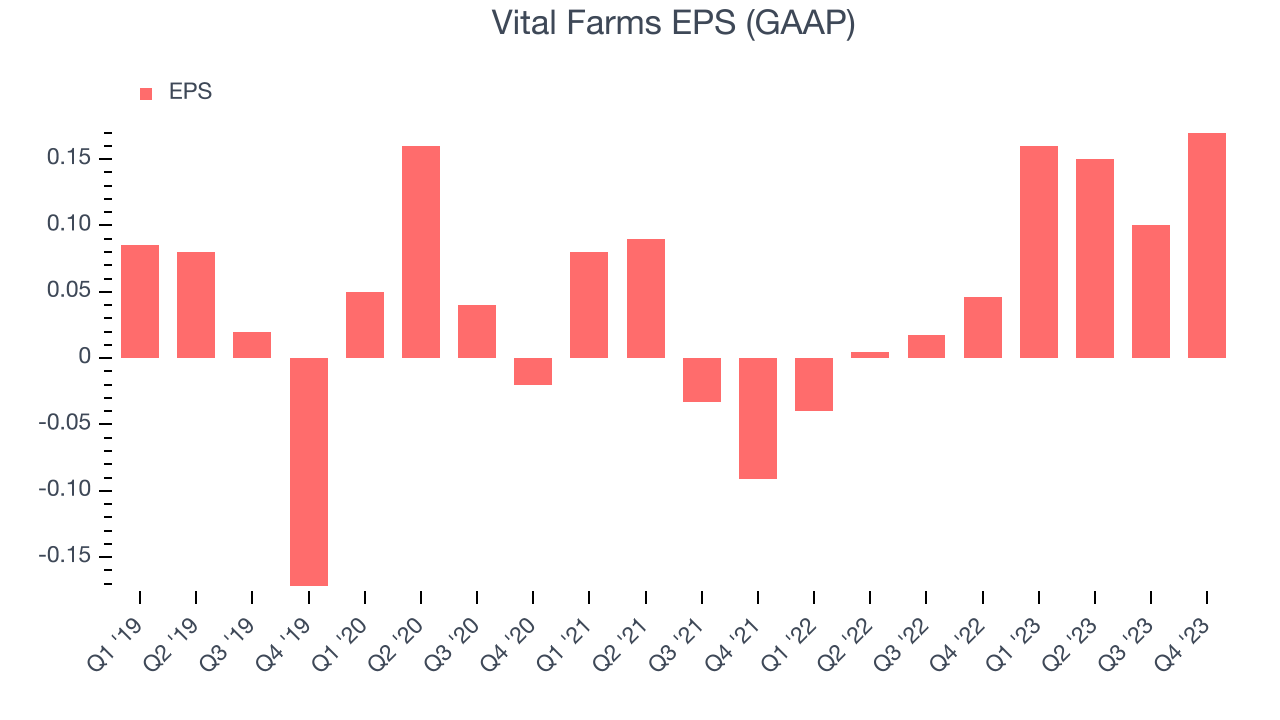

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q4, Vital Farms reported EPS at $0.17, up from $0.05 in the same quarter a year ago. This print easily cleared Wall Street's estimates, and shareholders should be content with the results.

Between FY2020 and FY2023, Vital Farms's EPS grew 152%, translating into an astounding 36.1% compounded annual growth rate. Thanks to the magic of compound interest, this means that Vital Farms will more than quadruple its EPS in five years if it can maintain this rate of growth.

Over the next 12 months, however, Wall Street is projecting Vital Farms's EPS to stay flat.

Cash Is King

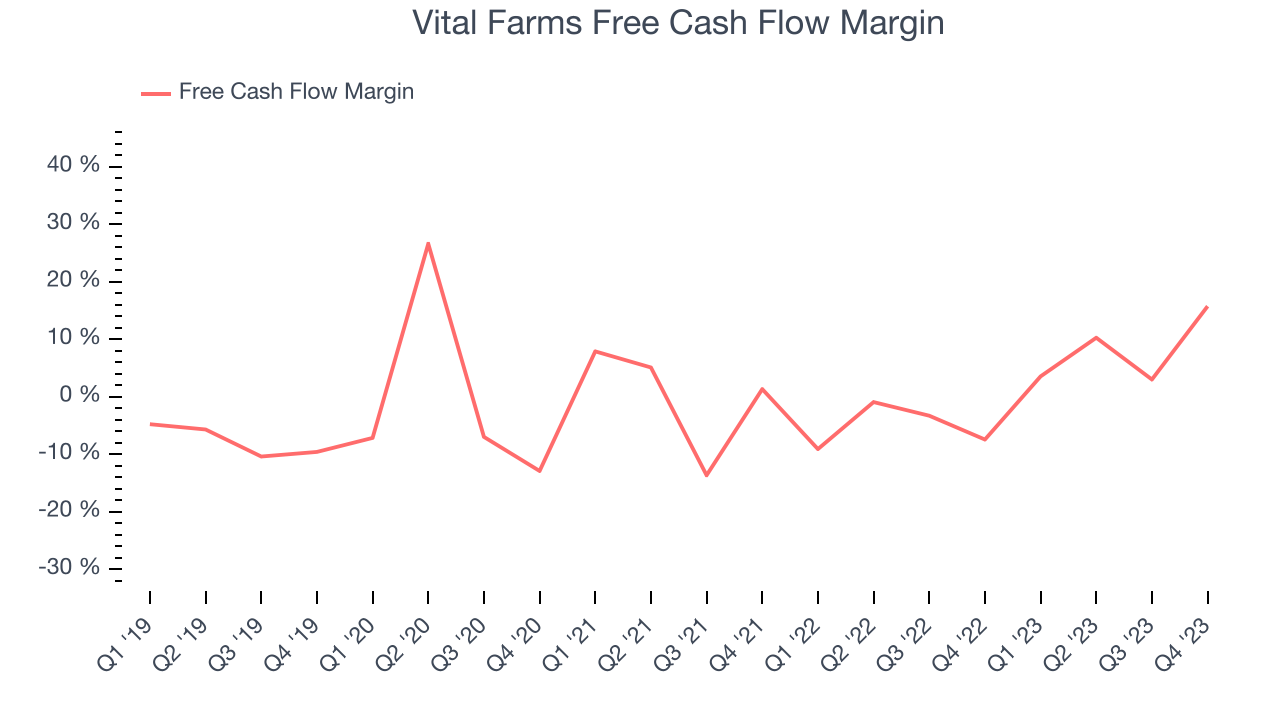

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Vital Farms's free cash flow came in at $21.33 million in Q4, representing a 15.7% margin. This result was great for the business as it flipped from cash flow negative in the same quarter last year to positive this quarter.

Over the last eight quarters, Vital Farms has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 2.5%, subpar for a consumer staples business. However, its margin has averaged year-on-year increases of 13.7 percentage points over the last 12 months. Shareholders should be excited as this will certainly help Vital Farms reach the next level of profitability.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Vital Farms's five-year average ROIC was 14%, higher than most consumer staples companies. Just as you’d like your investment dollars to generate returns, Vital Farms's invested capital has produced solid profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Uneventfully, Vital Farms's ROIC stayed the same over the last two years. A rising ROIC would be ideal, but this is still a noteworthy feat when considering its returns are already high.

Key Takeaways from Vital Farms's Q4 Results

We were impressed by how significantly Vital Farms blew past analysts' operating margin and EPS expectations this quarter. We were also glad its revenue beat, driven by volume growth of 11.6% - this type of unit growth is rare in the consumer staples industry.

Topping off the strong quarter was encouraging guidance, as management's revenue and EBITDA outlooks of $552 million and $57 million cleared Wall Street's projections. The company's long-term goal is to hit $1 billion in net revenue by 2027 with a 35% gross margin and 12-14% adjusted EBITDA margin.

Zooming out, we think this was a great quarter that shareholders will appreciate. The stock is up 9.8% after reporting and currently trades at $20.86 per share.

Is Now The Time?

Vital Farms may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We think Vital Farms is a good business. First off, its revenue growth has been exceptional over the last three years. And while its brand caters to a niche market, its volume growth has been in a league of its own. On top of that, its EPS growth over the last three years has been fantastic.

Vital Farms's price-to-earnings ratio based on the next 12 months is 32.5x. There are definitely things to like about Vital Farms and there's no doubt it's a bit of a market darling, at least for some investors. But when considering the company against the backdrop of the consumer staples landscape, it seems there's a lot of optimism already priced in. We wonder if there are better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $18.43 per share right before these results (compared to the current share price of $20.86).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.