Western Digital Corporation (NASDAQ:WDC) Q3: Beats On Revenue, Next Quarter Growth Looks Optimistic

Adam Hejl 2022/04/28 4:19 pm EDT

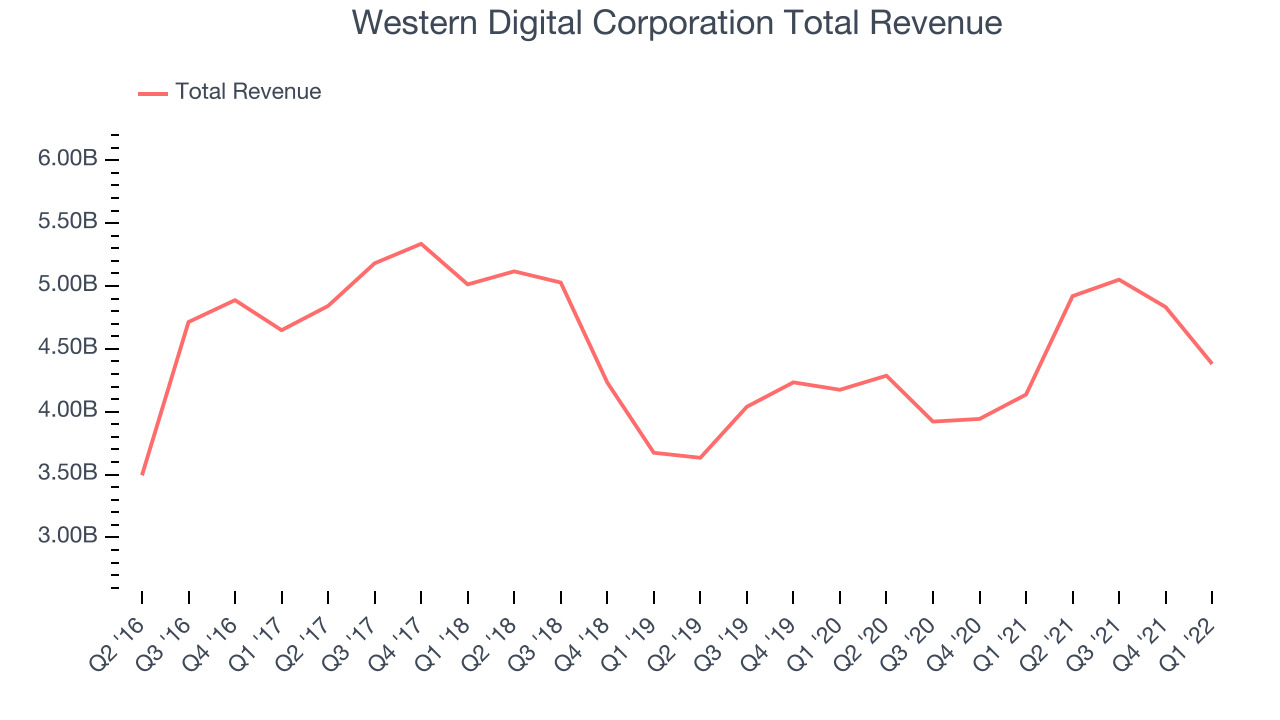

Leading data storage manufacturer Western Digital (NASDAQ: WDC) reported Q3 FY2022 results that beat analyst expectations, with revenue up 5.89% year on year to $4.38 billion. Guidance for next quarter's revenue was $4.6 billion at the midpoint, which is 1.14% above the analyst consensus. Western Digital Corporation made a GAAP profit of $25 million, down on its profit of $197 million, in the same quarter last year.

Is now the time to buy Western Digital Corporation? Access our full analysis of the earnings results here, it's free.

Western Digital Corporation (WDC) Q3 FY2022 Highlights:

- Revenue: $4.38 billion vs analyst estimates of $4.33 billion (1.03% beat)

- EPS (non-GAAP): $1.65 vs analyst estimates of $1.49 (11% beat)

- Revenue guidance for Q4 2022 is $4.6 billion at the midpoint, above analyst estimates of $4.54 billion

- Free cash flow of $148 million, down 63.6% from previous quarter

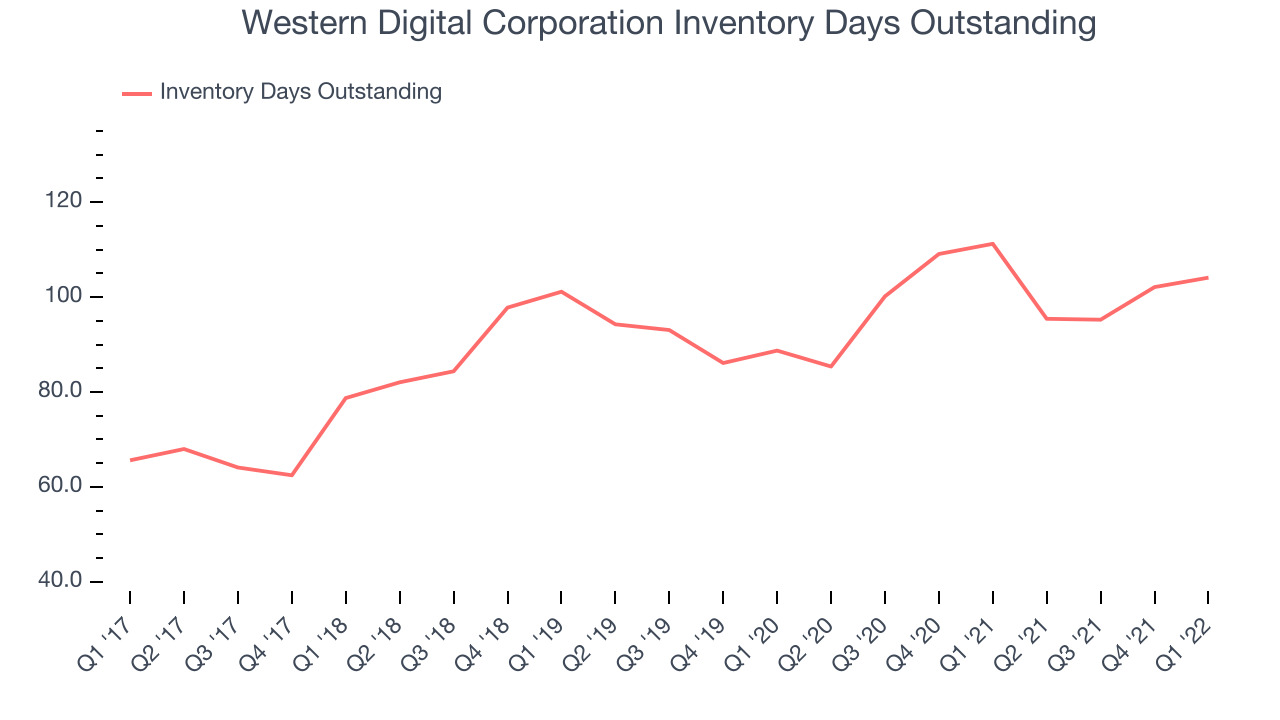

- Inventory Days Outstanding: 104, up from 102 previous quarter

- Gross Margin (GAAP): 26.9%, in line with same quarter last year

"The entire Western Digital team worked together to deliver excellent financial performance while navigating a dynamic geopolitical and macroeconomic environment, as well as ongoing supply challenges. This has all been made possible by the operational and portfolio improvements we have made over the last couple of years, which enable us to unlock the earnings power of the Western Digital model,” said David Goeckeler, Western Digital CEO.

Founded in 1970 by a Motorola employee, Western Digital (NASDAQ: WDC) is a leading producer of hard disk drives, SSDs and flash memory.

The rapid growth in data generation and the need to support increases in processing power for everything from consumer devices to data center servers are driving the demand for memory chips. From the content delivery networks and edge computing to the cloud, data storage is a key component underpinning the global technology architecture. On top of that, secular growth drivers like machine learning and the boom in media-rich digital content are further accelerating the need for storage. Like all semiconductor segments, memory makers are highly cyclical, driven by supply and demand imbalances and exposure to consumer product cycles.

Sales Growth

Western Digital Corporation's revenue growth over the last three years has been unimpressive, averaging 3.69% annually. But as you can see below, last year has been stronger for the company, growing from quarterly revenue of $4.13 billion to $4.38 billion. Semiconductors are a cyclical industry and long-term investors should be prepared for periods of high growth, followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

While Western Digital Corporation beat analysts' revenue estimates, this was a very slow quarter with just 5.89% revenue growth. This marks 4 straight quarters of revenue growth, implying we are mid-cycle for Western Digital Corporation, as a typical upcycle tends to last 8-10 quarters.

Western Digital Corporation's revenue growth is expected to go negative next quarter, with the company guiding to decline of 6.5% YoY next quarter, but analyst consensus sees growth of 5.65% over the next twelve months.

There are others doing even better than Western Digital Corporation. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 150% since the IPO last December. You can find it on our platform for free.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) are an important metric for chipmakers, as it reflects the capital intensity of the business and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise the company may have to downsize production.

This quarter, Western Digital Corporation’s inventory days came in at 104, 14 days above the five year average, suggesting that that inventory has grown to higher levels than what we used to see in the past.

Key Takeaways from Western Digital Corporation's Q3 Results

With a market capitalization of $15.6 billion, more than $2.5 billion in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

We were impressed by how strongly Western Digital Corporation outperformed analysts’ earnings expectations this quarter. And we were also glad to see the improvement in operating margin. On the other hand, it was less good to see that the revenue growth was quite weak and the inventory levels increased a little. Overall, this quarter's results still seemed pretty positive and shareholders can feel optimistic. The company is up 3.64% on the results and currently trades at $54.55 per share.

Should you invest in Western Digital Corporation right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.