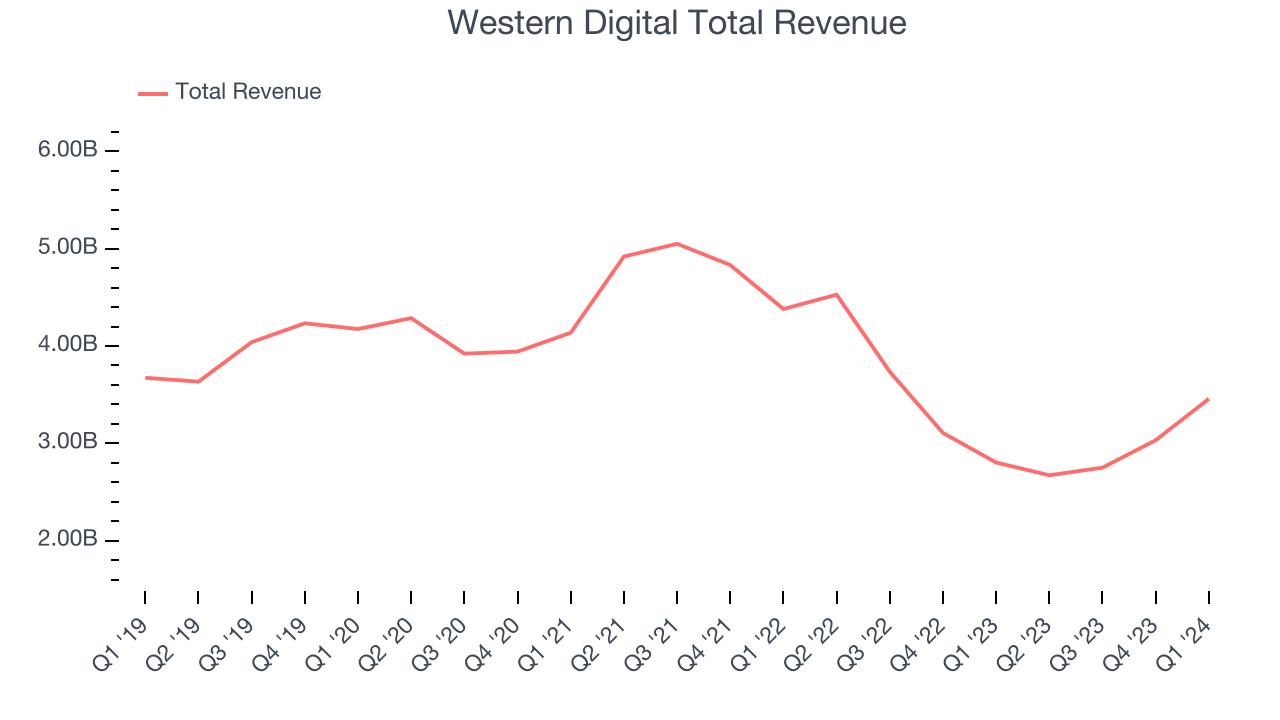

Leading data storage manufacturer Western Digital (NASDAQ: WDC) reported Q1 CY2024 results topping analysts' expectations, with revenue up 23.3% year on year to $3.46 billion. The company expects next quarter's revenue to be around $3.7 billion, in line with analysts' estimates. It made a non-GAAP profit of $0.63 per share, improving from its loss of $1.34 per share in the same quarter last year.

Western Digital (WDC) Q1 CY2024 Highlights:

- Revenue: $3.46 billion vs analyst estimates of $3.35 billion (3.2% beat)

- EPS (non-GAAP): $0.63 vs analyst estimates of $0.15 (312% beat)

- Revenue Guidance for Q2 CY2024 is $3.7 billion at the midpoint, roughly in line with what analysts were expecting

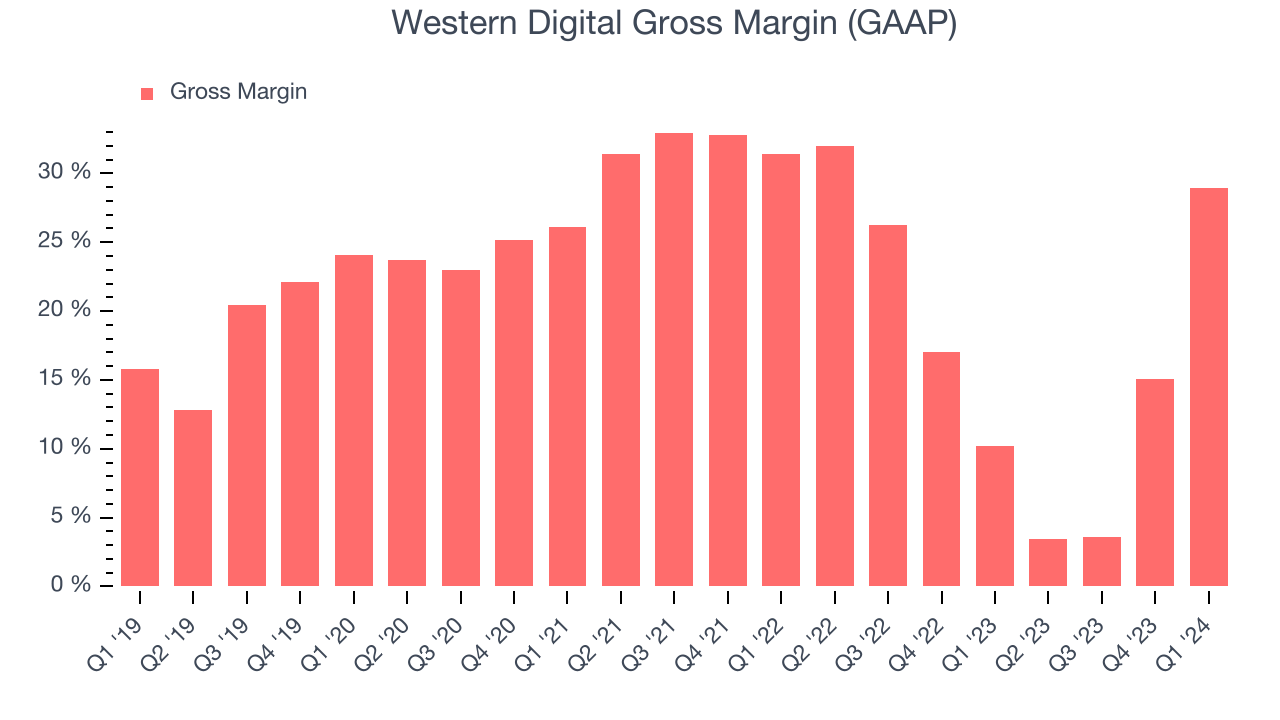

- Gross Margin (GAAP): 29%, up from 10.2% in the same quarter last year

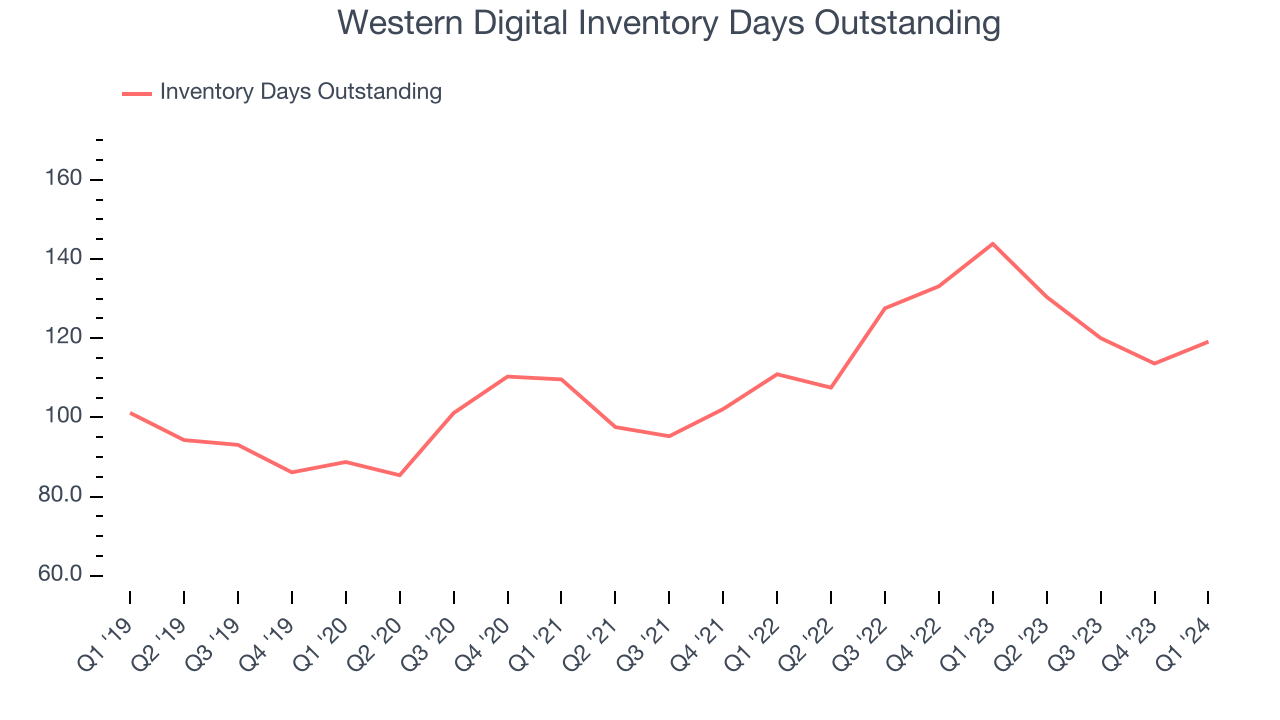

- Inventory Days Outstanding: 119, up from 114 in the previous quarter

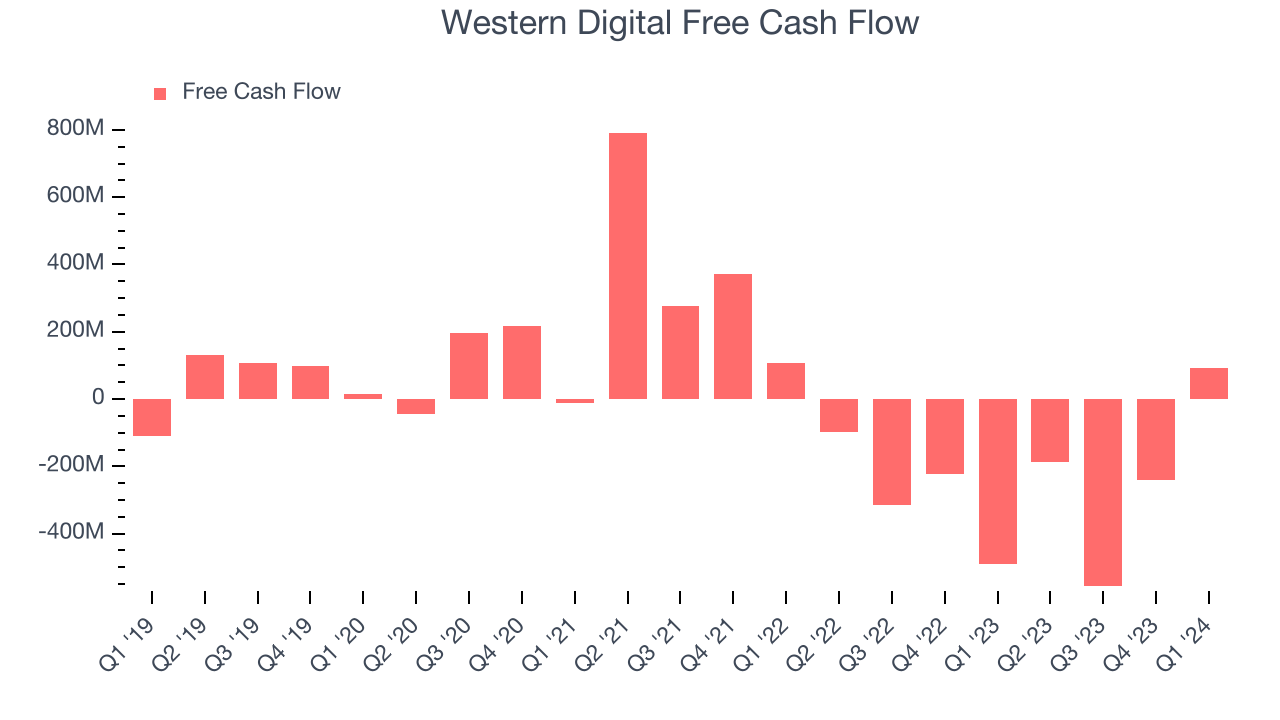

- Free Cash Flow of $91 million is up from -$242 million in the previous quarter

- Market Capitalization: $22.71 billion

Founded in 1970 by a Motorola employee, Western Digital (NASDAQ: WDC) is a leading producer of hard disk drives, SSDs and flash memory.

Originally a producer of calculator chips, Western Digital refocused on hard disk drives in 1978, and created the original ATA hard disk drive standard used in PCs. HDDs were one of the most competitive, low margin, tech markets for decades until a wave of consolidation shrank the market to two main players; Western Digital and Seagate, following Western Digital’s acquisition of Hitachi Global Storage in 2015. That same year the company acquired SanDisk, one of the largest producers of flash memory.

The SanDisk acquisition brought Western Digital into a partnership with Toshiba (now named Kioxia) in Flash Ventures, the largest producer of flash memory semiconductors in the world, and diversified Western Digital’s revenues equally across HDD and flash memory, each of which today account for roughly half of its revenues.

Western Digital’s peers and competitors include Seagate (NASDAQ:STX), SK Hynix (KOSI:000660), and Samsung (KOSI:005930).Memory Semiconductors

The global memory chip market has become concentrated due to the highly commoditized nature of these semiconductors. Despite the market consolidation, DRAM and NAND are subject to wide pricing swings as supply and demand ebbs and flows. This plays itself out in the business models of memory producers, where the large, fixed cost bases required to produce memory chips in volume can become very profitable during times of rising prices due to high demand and tight supply but also can result in periods of low profitability when more supply is brought online or demand drops.

Sales Growth

Western Digital's revenue has been declining over the last three years, dropping by 6.7% on average per year. As you can see below, this was a weaker quarter for the company, with revenue growing from $2.80 billion in the same quarter last year to $3.46 billion. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Western Digital had a good quarter as its revenue grew 23.3% year on year, topping analysts' estimates by 3.2%. Western Digital's growth inflected from negative to positive this quarter, indicating that the recent cycle downturn is likely in the rearview mirror.

Western Digital returned to positive revenue growth this quarter and its management team expects the trend to continue. The company is guiding to 38.5% year-on-year growth next quarter, and analysts seem to agree, forecasting 38.9% growth over the next 12 months.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Western Digital's DIO came in at 119, which is 11 days above its five-year average, suggesting that the company's inventory has grown to higher levels than we've seen in the past.

Pricing Power

In the semiconductor industry, a company's gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor. Western Digital's gross profit margin, which shows how much money the company gets to keep after paying key materials, input, and manufacturing costs, came in at 29% in Q1, up 18.8 percentage points year on year.

Western Digital's gross margins have been stable over the last 12 months, averaging 13.8%. Although its margins remain below the peer group average, the trend points to a likely stable pricing environment.

Profitability

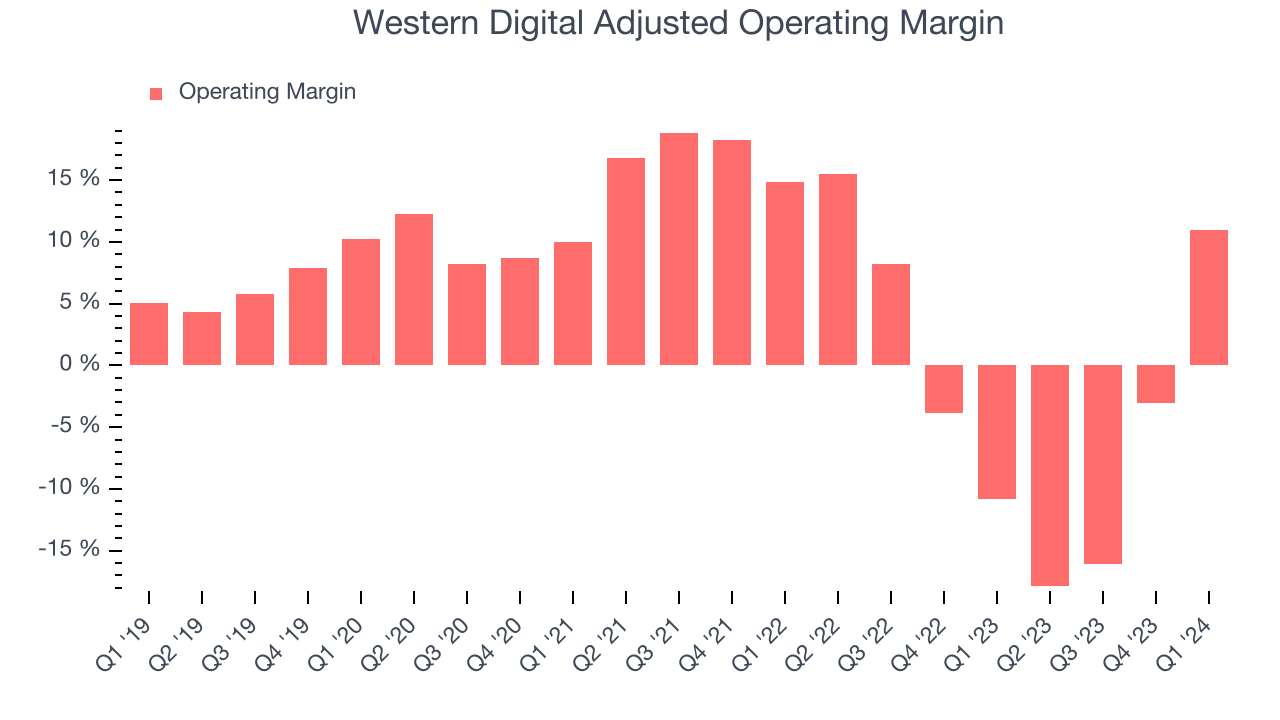

Western Digital reported an operating margin of 11% in Q1, up 21.8 percentage points year on year. Operating margins are one of the best measures of profitability because they tell us how much money a company takes home after manufacturing its products, marketing and selling them, and, importantly, keeping them relevant through research and development.

Western Digital's operating margins have been trending down over the last year, averaging negative 5.3%. This is a bad sign for Western Digital, whose margins are already among the lowest for semiconductors. The company will have to improve its relatively inefficient operating model.

Earnings, Cash & Competitive Moat

Analysts covering Western Digital expect earnings per share to grow 213% over the next 12 months, although estimates will likely change after earnings.

Although earnings are important, we believe cash is king because you can't use accounting profits to pay the bills. Western Digital's free cash flow came in at $91 million in Q1, up 119% year on year.

As you can see above, Western Digital failed to produce positive free cash flow over the last 12 months and shareholders will likely want to see an improvement in the coming quarters.

Return on Invested Capital (ROIC)

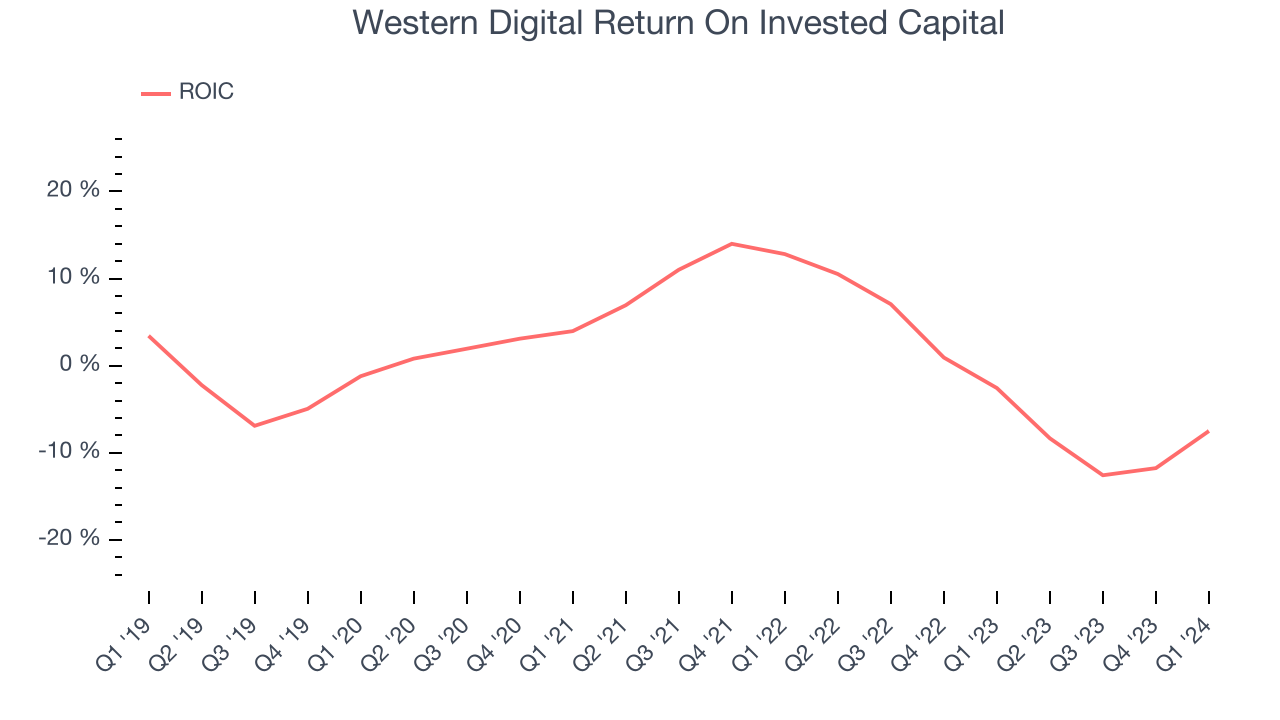

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Western Digital's five-year average ROIC was 1.1%, somewhat low compared to the best semiconductor companies that consistently pump out 35%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Western Digital's ROIC averaged 6.4 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Western Digital's Q1 Results

We were impressed by Western Digital's strong gross margin improvement this quarter. We were also excited its revenue and EPS outperformed Wall Street's estimates, driven by better-than-expected performance in its cloud and client end markets. On the other hand, its inventory levels increased, but that could be a result of stockpiling resources ahead of demand - management noted industry supply and demand dynamics are improving. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. The market was likely expecting more, however, and the stock is down 1.1% after reporting, trading at $68.7 per share.

Is Now The Time?

Western Digital may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for everyone who's making the lives of others easier through technology, but in the case of Western Digital, we'll be cheering from the sidelines. Its revenue has declined over the last three years, and analysts expect growth to deteriorate from here. On top of that, its relatively low ROIC suggests it has struggled to grow profits historically, and its operating margins reveal subpar cost controls compared to other semiconductor businesses.

Western Digital's price-to-earnings ratio based on the next 12 months is 12.3x. While we've no doubt one can find things to like about Western Digital, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $78.82 per share right before these results (compared to the current share price of $68.70).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.