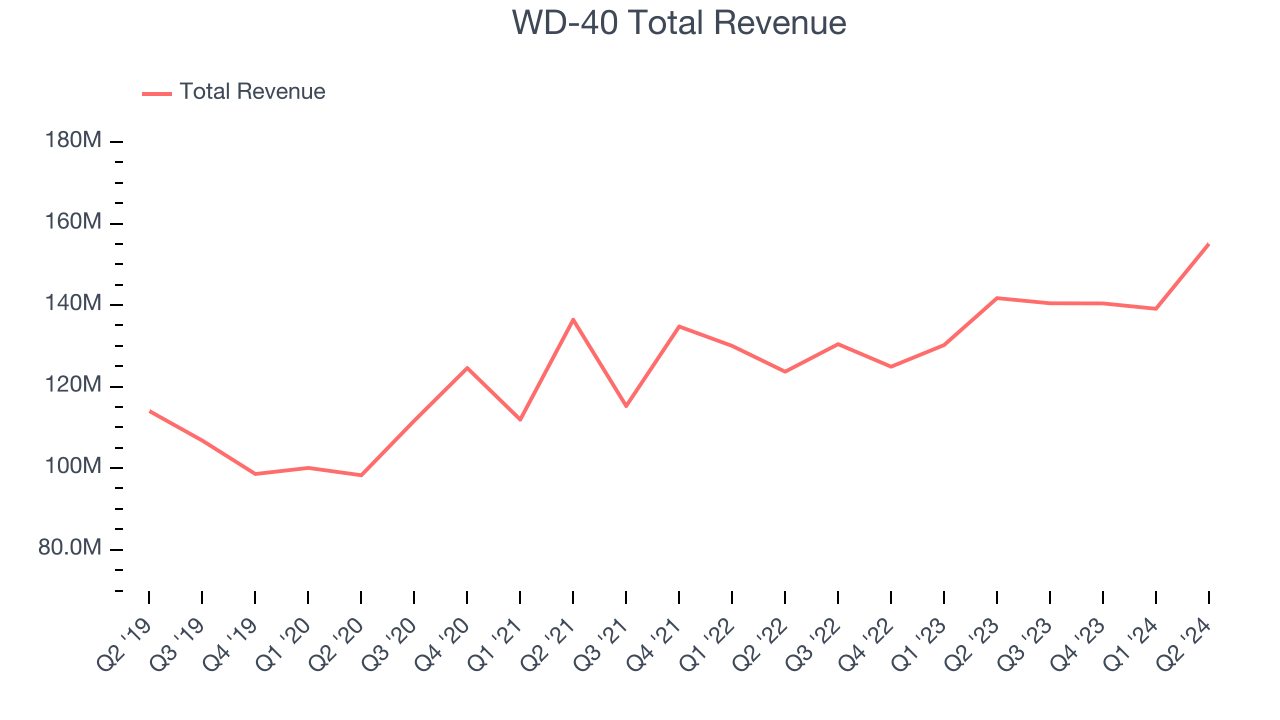

Household products company WD-40 (NASDAQGS:WDFC) reported Q2 CY2024 results exceeding Wall Street analysts' expectations, with revenue up 9.4% year on year to $155 million. The company's full-year revenue guidance of $585 million at the midpoint also came in 1.2% above analysts' estimates. It made a GAAP profit of $1.46 per share, improving from its profit of $1.38 per share in the same quarter last year.

Is now the time to buy WD-40? Find out by accessing our full research report, it's free.

WD-40 (WDFC) Q2 CY2024 Highlights:

- Revenue: $155 million vs analyst estimates of $145.8 million (6.3% beat)

- EPS: $1.46 vs analyst estimates of $1.27 (15% beat)

- The company reconfirmed its revenue guidance for the full year of $585 million at the midpoint

- Gross Margin (GAAP): 53.1%, up from 50.6% in the same quarter last year

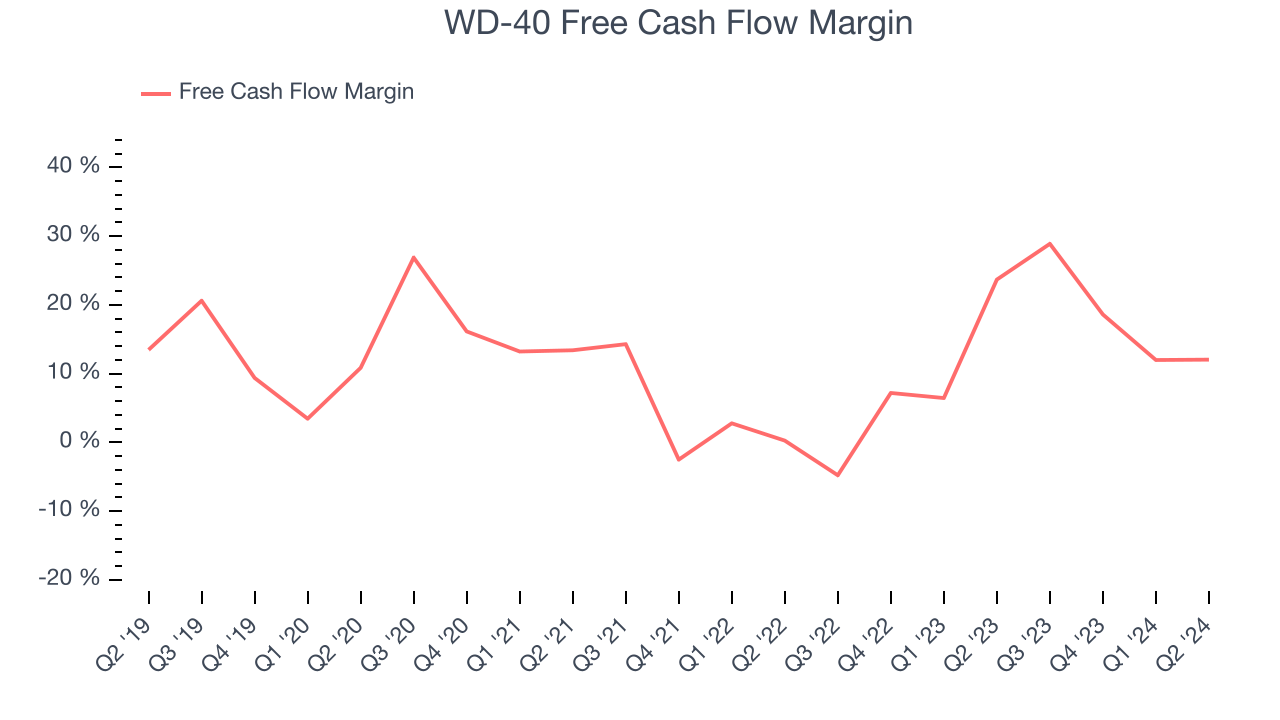

- Free Cash Flow of $18.67 million, up 12% from the previous quarter

- Market Capitalization: $2.99 billion

Short for “Water Displacement perfected on the 40th try”, WD-40 (NASDAQGS:WDFC) is a renowned American consumer goods company known for its iconic and versatile spray, WD-40 Multi-Use Product.

Household Products

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

Sales Growth

WD-40 is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale.

As you can see below, the company's annualized revenue growth rate of 5.9% over the last three years was mediocre for a consumer staples business.

This quarter, WD-40 reported solid year-on-year revenue growth of 9.4%, and its $155 million in revenue outperformed Wall Street's estimates by 6.3%. Looking ahead, Wall Street expects sales to grow 4.5% over the next 12 months, a deceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

WD-40 has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining a cash cushion. The company's free cash flow margin has been among the best in the consumer staples sector, averaging 13.3% over the last two years.

Taking a step back, we can see that WD-40's margin expanded by 9.3 percentage points during that time. This is encouraging because it gives the company more ways to win.

WD-40's free cash flow clocked in at $18.67 million in Q2, equivalent to a 12% margin. The company's margin regressed as it was 11.6 percentage points lower than in the same quarter last year, but we wouldn't read too much into it because working capital needs can be seasonal and cause short-term swings.

Key Takeaways from WD-40's Q2 Results

We were impressed by how significantly WD-40 blew past analysts' revenue and EPS expectations this quarter. We were also glad its full-year revenue guidance came in higher than Wall Street's estimates. On the other hand, its full-year earnings forecast was underwhelming, but the other beats more than made up for it. Overall, we think this was a really good quarter that should please shareholders. The stock traded up 9.8% to $241.41 immediately after reporting.

WD-40 may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.