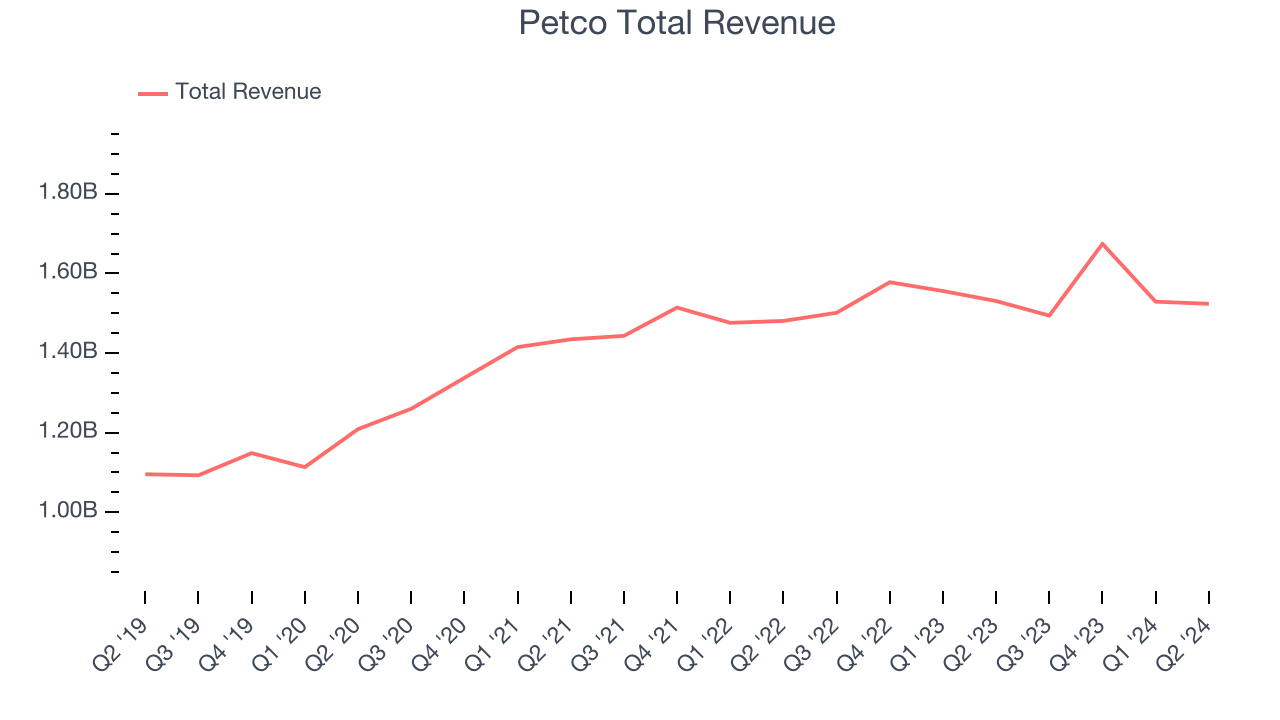

Pet-focused retailer Petco (NASDAQ:WOOF) reported results in line with analysts’ expectations in Q2 CY2024, with revenue flat year on year at $1.52 billion. On the other hand, the company expects next quarter’s revenue to be around $1.5 billion, slightly below analysts’ estimates. It made a non-GAAP loss of $0.02 per share, down from its profit of $0.06 per share in the same quarter last year.

Is now the time to buy Petco? Find out by accessing our full research report, it’s free.

Petco (WOOF) Q2 CY2024 Highlights:

- Revenue: $1.52 billion vs analyst estimates of $1.52 billion (small miss)

- EPS (non-GAAP): -$0.02 vs analyst estimates of -$0.03

- Revenue Guidance for Q3 CY2024 is $1.5 billion at the midpoint, below analyst estimates of $1.51 billion

- EPS (non-GAAP) guidance for Q3 CY2024 is -$0.04 at the midpoint, below analyst estimates of -$0.03

- EBITDA guidance for Q3 CY2024 is $78 million at the midpoint, below analyst estimates of $80.3 million

- Gross Margin (GAAP): 38.1%, in line with the same quarter last year

- EBITDA Margin: 5.5%, down from 7.4% in the same quarter last year

- Free Cash Flow Margin: 2.8%, similar to the same quarter last year

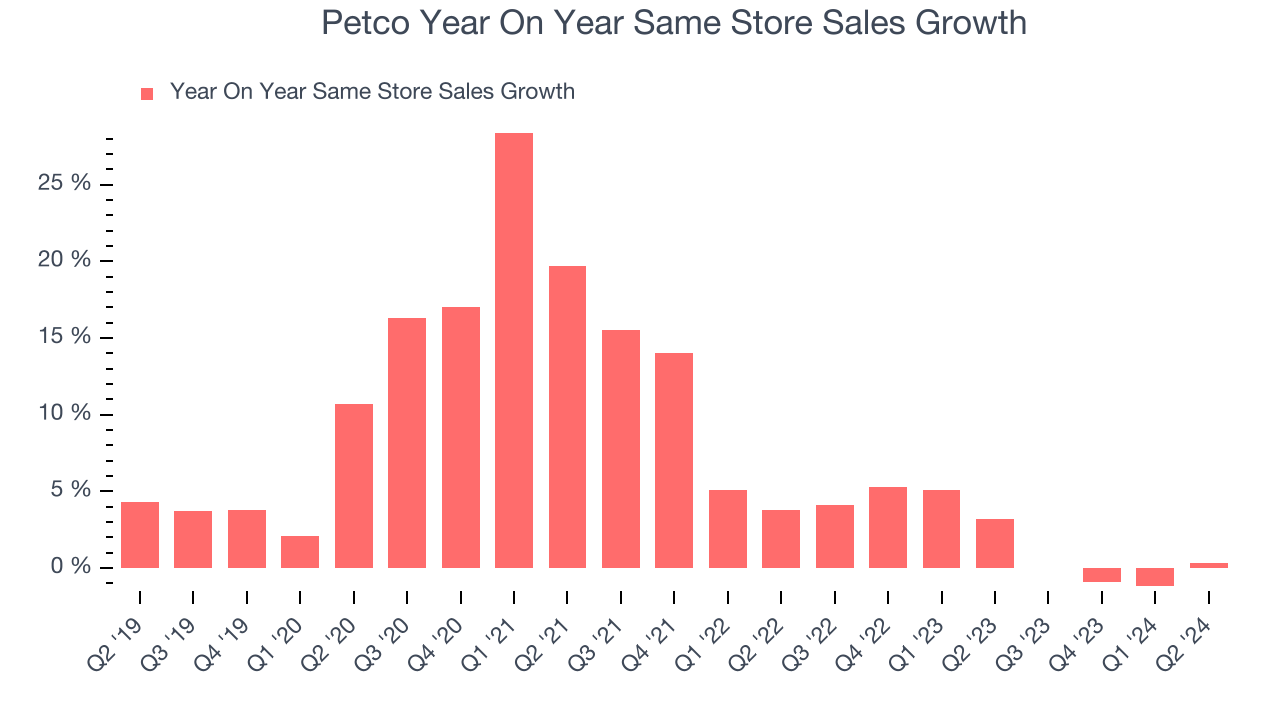

- Same-Store Sales were flat year on year (3.2% in the same quarter last year)

- Market Capitalization: $778 million

Historically known for its window displays of pets for sale or adoption, Petco (NASDAQ:WOOF) is a specialty retailer of pet food and supplies as well as a provider of services such as wellness checks and grooming.

Specialty Retail

Some retailers try to sell everything under the sun, while others—appropriately called Specialty Retailers—focus on selling a narrow category and aiming to be exceptional at it. Whether it’s eyeglasses, sporting goods, or beauty and cosmetics, these stores win with depth of product in their category as well as in-store expertise and guidance for shoppers who need it. E-commerce competition exists and waning retail foot traffic impacts these retailers, but the magnitude of the headwinds depends on what they sell and what extra value they provide in their stores.

Sales Growth

Petco is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company’s annualized revenue growth rate of 6.8% over the last five years was sluggish as its store count dropped, signaling that growth was driven by more sales at existing, established stores.

This quarter, Petco missed Wall Street’s estimates and reported a rather uninspiring 0.5% year-on-year revenue decline, generating $1.52 billion in revenue. The company is guiding for revenue to rise 0.4% year on year to $1.5 billion next quarter, improving from the 0.5% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for retailers.

Petco’s demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company’s same-store sales have grown by 2% year on year. Given its declining store count over the same period, this performance stems from higher e-commerce sales or increased foot traffic at existing stores, which is sometimes a side effect of reducing the total number of stores.

In the latest quarter, Petco’s year on year same-store sales were flat. By the company’s standards, this growth was a meaningful deceleration from the 3.2% year-on-year increase it posted 12 months ago. We’ll be watching Petco closely to see if it can reaccelerate growth.

Key Takeaways from Petco’s Q2 Results

We enjoyed seeing Petco exceed analysts’ EPS expectations this quarter. We were also happy its gross margin narrowly outperformed Wall Street’s estimates. On the other hand, its revenue and earnings guidance for next quarter came in slightly below Wall Street’s estimates. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The areas below expectations seem to be driving the stock move, and the stock traded down 1.9% to $3.02 immediately after reporting.

So should you invest in Petco right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.