Online real estate marketplace Zillow (NASDAQ:ZG) reported Q1 CY2024 results topping analysts' expectations, with revenue up 12.8% year on year to $529 million. It made a GAAP loss of $0.10 per share, down from its loss of $0.09 per share in the same quarter last year.

Is now the time to buy Zillow? Find out by accessing our full research report, it's free.

Zillow (ZG) Q1 CY2024 Highlights:

- Revenue: $529 million vs analyst estimates of $507.7 million (4.2% beat)

- EPS: -$0.10 vs analyst expectations of -$0.08 (23.4% miss)

- Gross Margin (GAAP): 76.7%, down from 80.4% in the same quarter last year

- Free Cash Flow of $41 million, down 21.2% from the previous quarter

- Market Capitalization: $10.02 billion

Founded by Expedia co-founders Lloyd Frink and Rich Barton, Zillow (NASDAQ:ZG) is the leading U.S. online real estate marketplace.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

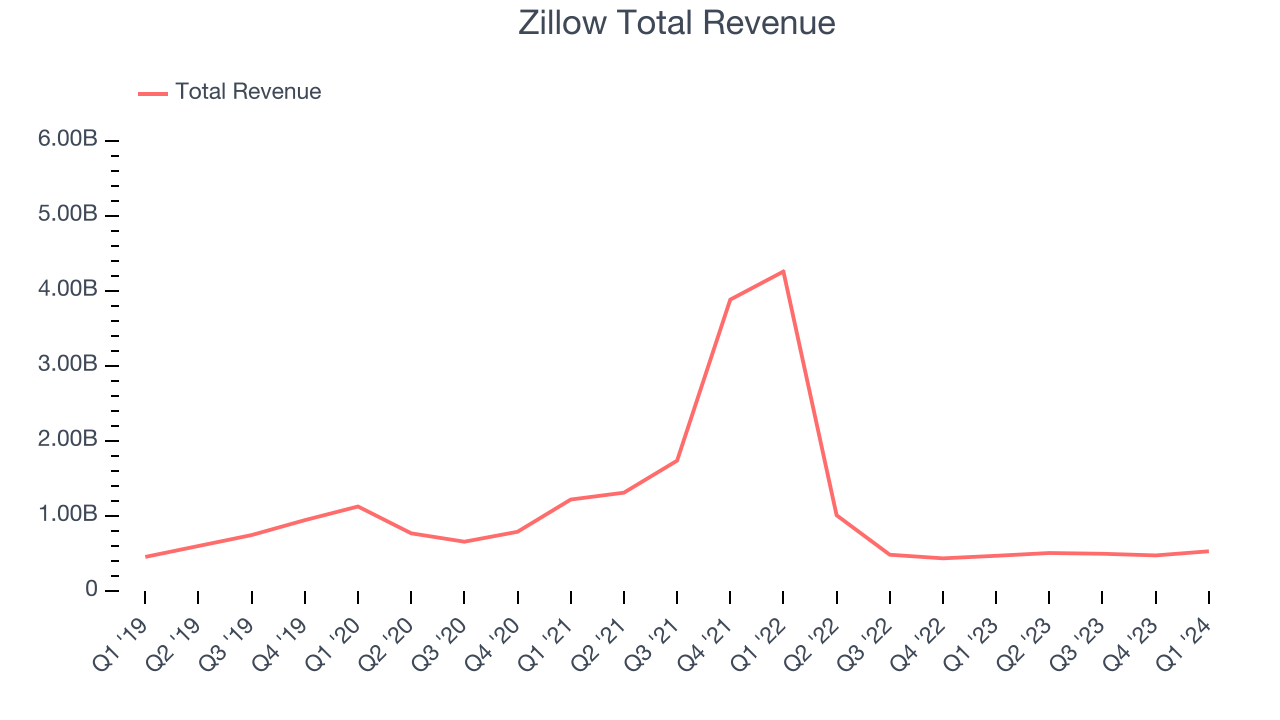

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Zillow's annualized revenue growth rate of 6.1% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Zillow's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 57.7% over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Zillow's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 57.7% over the last two years.

This quarter, Zillow reported robust year-on-year revenue growth of 12.8%, and its $529 million of revenue exceeded Wall Street's estimates by 4.2%. Looking ahead, Wall Street expects sales to grow 12.1% over the next 12 months, a deceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

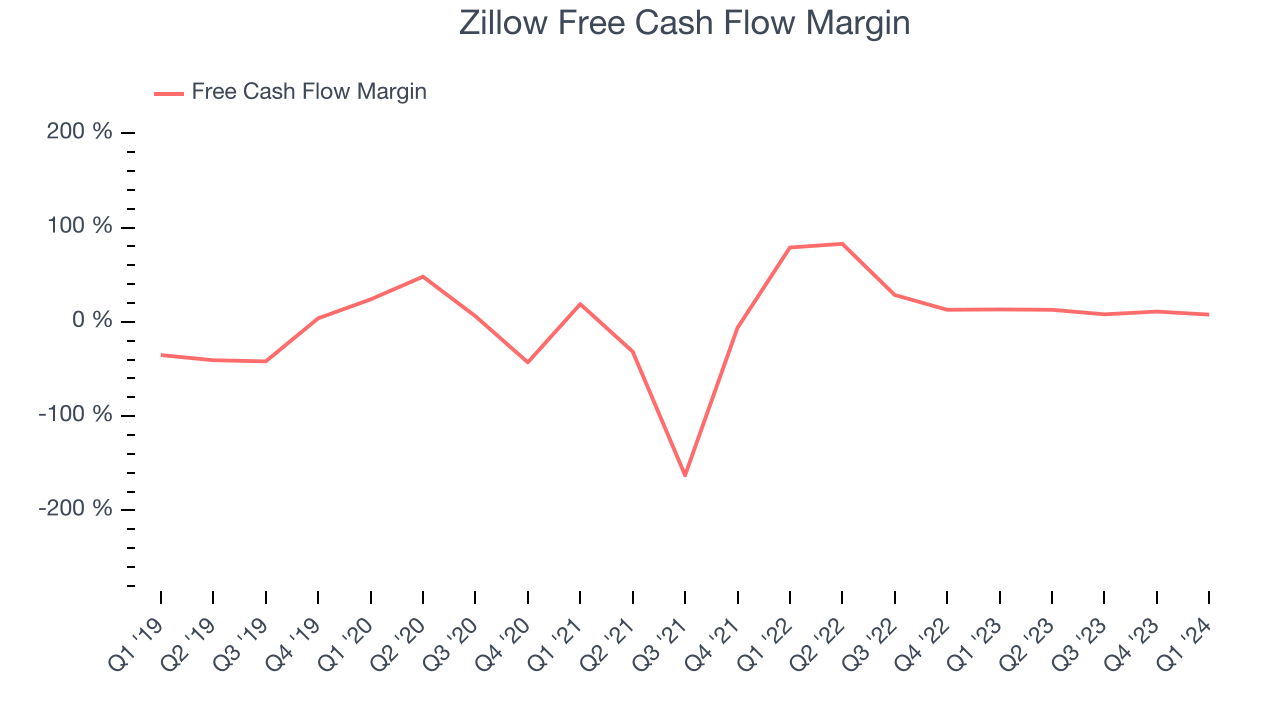

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Zillow has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining a robust cash balance. The company's free cash flow margin has been among the best in the consumer discretionary sector, averaging 29.3%.

Zillow's free cash flow came in at $41 million in Q1, equivalent to a 7.8% margin and down 33.9% year on year.

Key Takeaways from Zillow's Q1 Results

We enjoyed seeing Zillow exceed analysts' revenue and EBITDA expectations this quarter. On the other hand, its EPS missed and its number of website/mobile app visits fell short of Wall Street's projections. The company did not provide any guidance. Overall, the results could have been better. The company is down 9.1% on the results and currently trades at $37.65 per share.

Zillow may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.