Sales intelligence platform ZoomInfo reported Q4 FY2023 results beating Wall Street analysts' expectations, with revenue up 4.9% year on year to $316.4 million. The company expects next quarter's revenue to be around $308.5 million, in line with analysts' estimates. It made a non-GAAP profit of $0.26 per share, down from its profit of $0.26 per share in the same quarter last year.

ZoomInfo (ZI) Q4 FY2023 Highlights:

- Revenue: $316.4 million vs analyst estimates of $310.5 million (1.9% beat)

- EPS (non-GAAP): $0.26 vs analyst estimates of $0.25 (5.6% beat)

- Revenue Guidance for Q1 2024 is $308.5 million at the midpoint, roughly in line with what analysts were expecting

- Management's revenue guidance for the upcoming financial year 2024 is $1.27 billion at the midpoint, in line with analyst expectations and implying 2.5% growth (vs 13.5% in FY2023)

- Free Cash Flow of $119.9 million, up 26.5% from the previous quarter

- Gross Margin (GAAP): 88.9%, up from 87.8% in the same quarter last year

- Market Capitalization: $6.00 billion

Founded in 2007 as DiscoveryOrg and renamed after a merger in 2019, ZoomInfo (NASDAQ:ZI) is a software as a service product that provides sales departments with access to a database of prospective clients.

The company essentially runs a large database of professionals similar to LinkedIn, and it also maintains a repository of companies with information about their revenue, industry or number of employees. It then puts this data together to help sales teams find and identify potential customers, alerts them if new ones appear and provides them with contact details of prospective buyers. ZoomInfo scrapes the information and data from public websites, sources it from email communications of people who let the company scan their mailboxes or buys it from other companies.

Sales Software

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

ZoomInfo’s main competitor is LinkedIn which is owned by Microsoft (NASDAQ:MSFT), but there are plenty of smaller competitors in this space whether public, like TechTarget (NASDAQ:TTGT), or private, like Clearbit or FullContact.

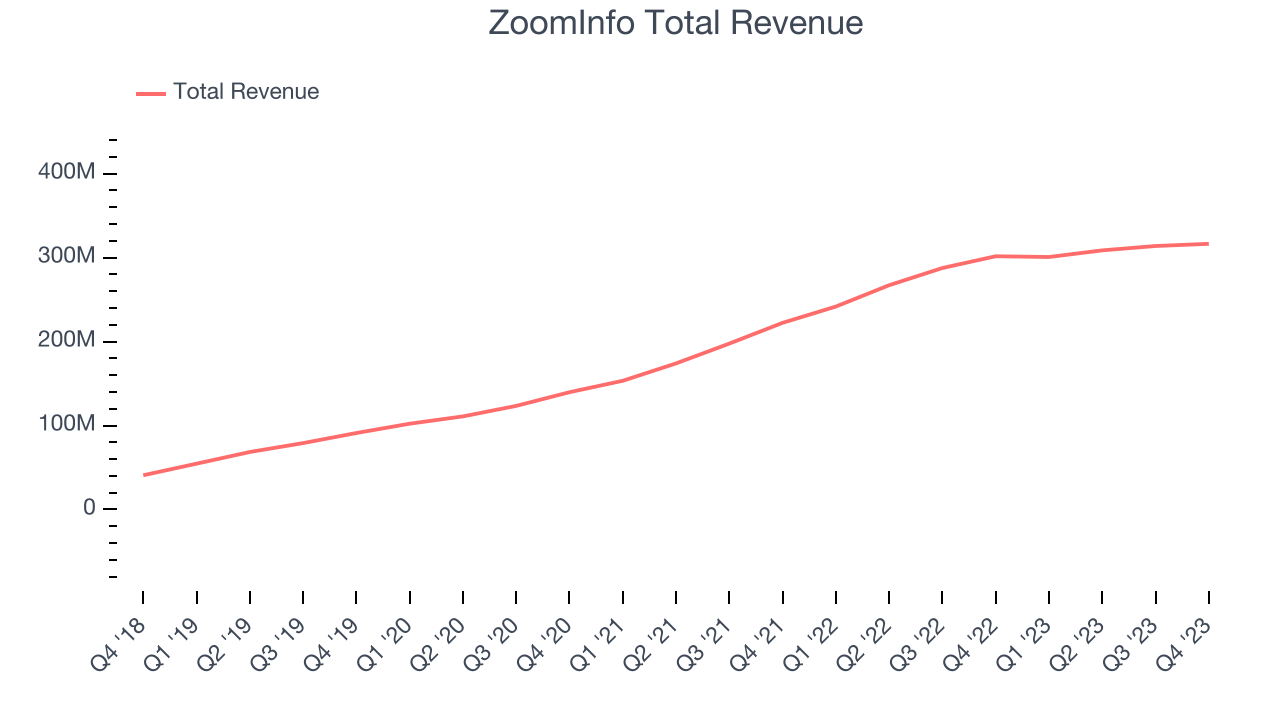

Sales Growth

As you can see below, ZoomInfo's revenue growth has been strong over the last two years, growing from $222.3 million in Q4 FY2021 to $316.4 million this quarter.

ZoomInfo's quarterly revenue was only up 4.9% year on year, which might disappoint some shareholders. Additionally, its growth did slow down compared to last quarter as the company's revenue increased by just $2.6 million in Q4 compared to $5.1 million in Q3 2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that ZoomInfo is expecting revenue to grow 2.6% year on year to $308.5 million, slowing down from the 24.4% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $1.27 billion at the midpoint, growing 2.5% year on year compared to the 12.9% increase in FY2023.

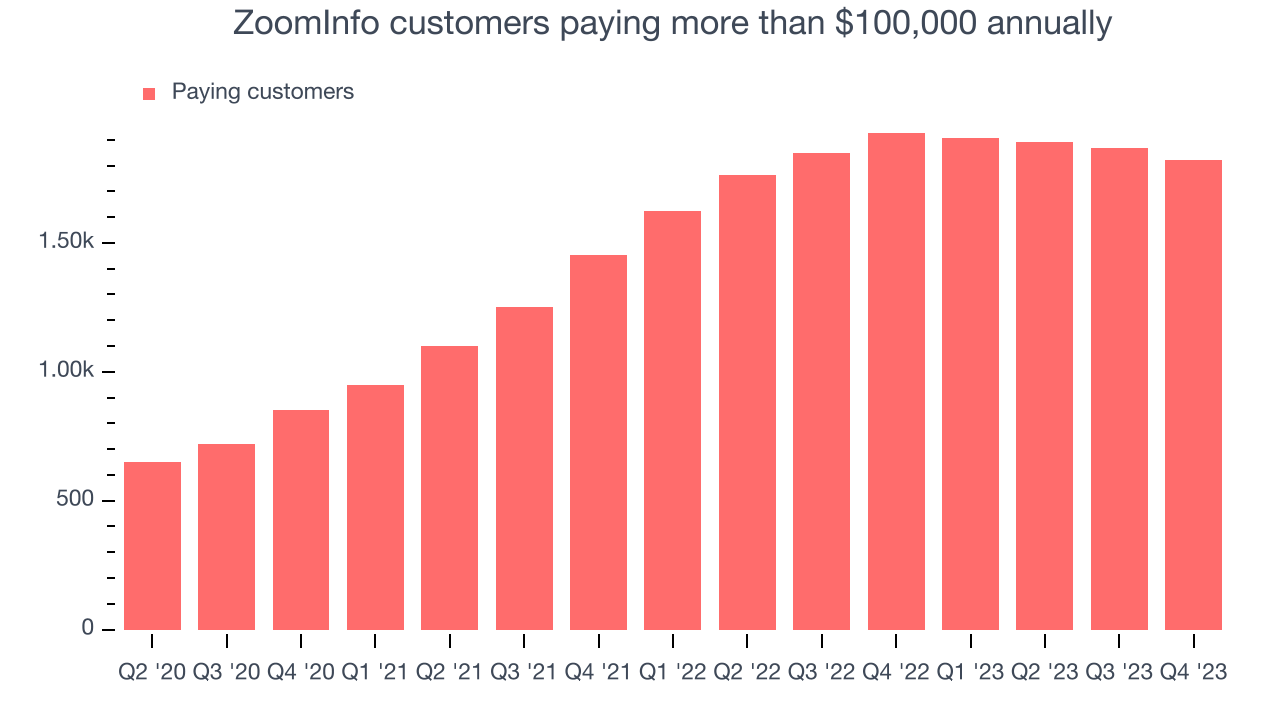

Large Customers Growth

This quarter, ZoomInfo reported 1,820 enterprise customers paying more than $100,000 annually, a decrease of 49 from the previous quarter. We've no doubt shareholders would like to see the company regain its sales momentum.

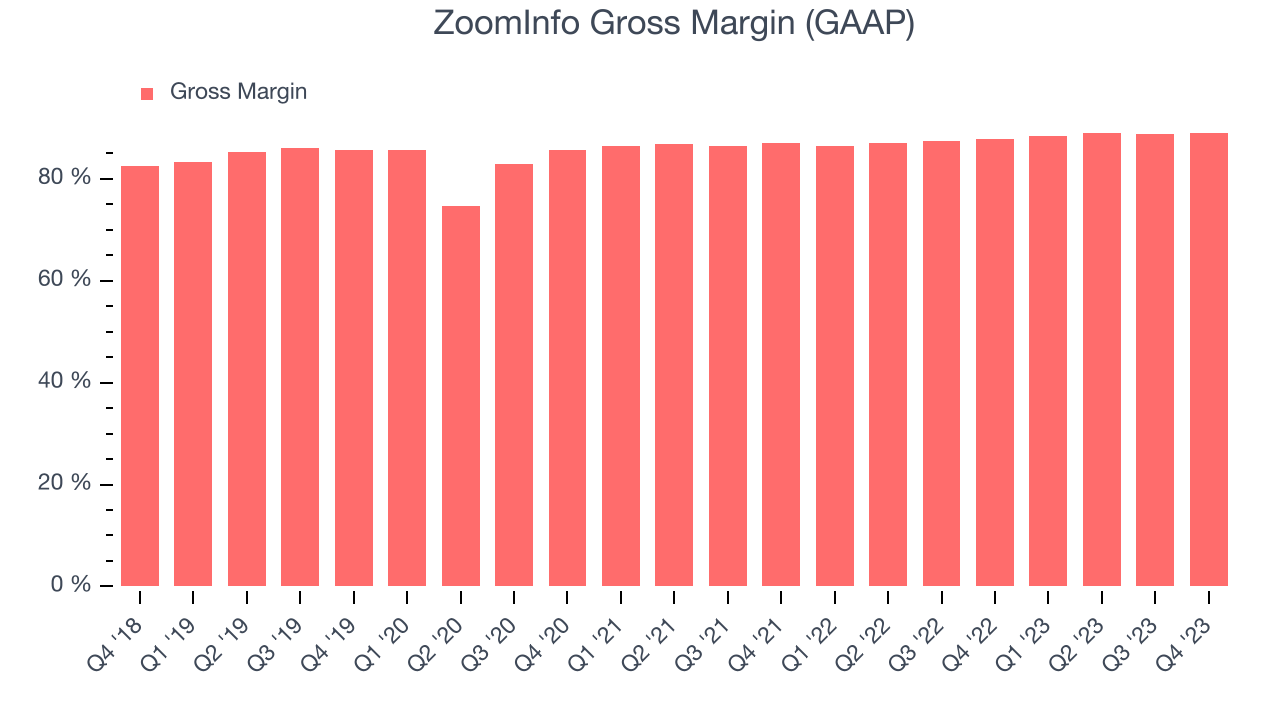

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. ZoomInfo's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 88.9% in Q4.

That means that for every $1 in revenue the company had $0.89 left to spend on developing new products, sales and marketing, and general administrative overhead. ZoomInfo's excellent gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity. It's also comforting to see its gross margin remain stable, indicating that ZoomInfo is controlling its costs and not under pressure from its competitors to lower prices.

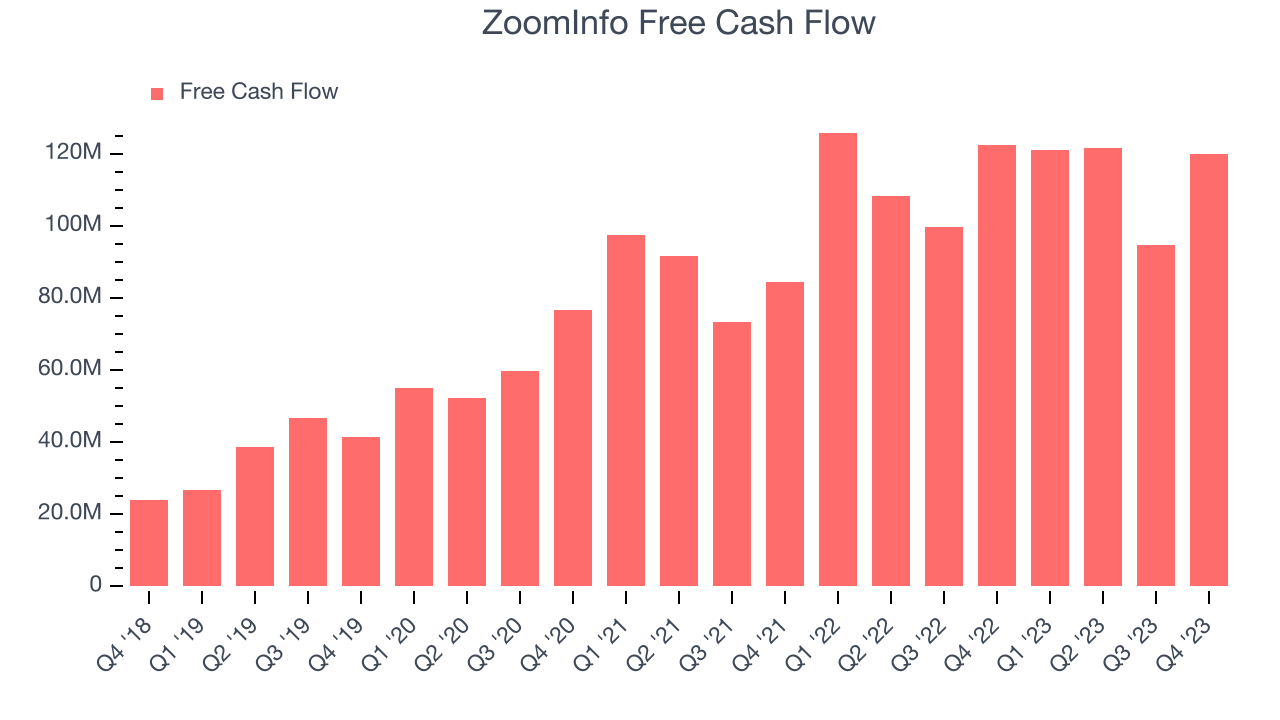

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. ZoomInfo's free cash flow came in at $119.9 million in Q4, roughly the same as last year.

ZoomInfo has generated $457.3 million in free cash flow over the last 12 months, an eye-popping 36.9% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Key Takeaways from ZoomInfo's Q3 Results

With a market capitalization of $6.16 billion, ZoomInfo is among smaller companies, but its $567.9 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

It was encouraging to see ZoomInfo narrowly top analysts' revenue and adjusted operating profit expectations this quarter. That really stood out as a positive in these results. On the other hand, its new large contract wins slowed and both its revenue and adjusted operating profit guidance for next quarter came in slightly below Wall Street's estimates. However, full year guidance for those two line items was slightly above. Overall, the results could have been better, but there were no major surprises good or bad, so the company is on track. The stock is up 1.48% after reporting and currently trades at $15.75 per share.

Key Takeaways from ZoomInfo's Q4 Results

It was encouraging to see ZoomInfo narrowly top analysts' revenue expectations this quarter. Non-GAAP operating profit also beat expectations. Those stood out as a positives in these results. While revenue guidance for next year suggests a slowdown in growth, guidance was roughly in line with expectations. Given some of the choppy quarters the company has had in the last year and fears about secular tailwinds to the business from AI, these results were likely better than feared. The stock is up 10.2% after reporting and currently trades at $17.68 per share.

Is Now The Time?

ZoomInfo may have had a bad quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Although ZoomInfo isn't a bad business, it probably wouldn't be one of our picks. Although its , Wall Street expects growth to deteriorate from here. And while its bountiful generation of free cash flow empowers it to invest in growth initiatives, the downside is its existing customers have been reducing their spend, which is a bit of a concern. On top of that, its customer acquisition is less efficient than many comparable companies.

The market is certainly expecting long-term growth from ZoomInfo given its price-to-sales ratio based on the next 12 months is 5.0x. In the end, beauty is in the eye of the beholder. While ZoomInfo wouldn't be our first pick, if you like the business, the shares are trading at a pretty interesting price point right now.

Wall Street analysts covering the company had a one-year price target of $19.81 per share right before these results (compared to the current share price of $17.68).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.