Video conferencing platform Zoom (NASDAQ:ZM) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 3.2% year on year to $1.14 billion. The company expects next quarter's revenue to be around $1.15 billion, in line with analysts' estimates. It made a non-GAAP profit of $1.35 per share, improving from its profit of $1.16 per share in the same quarter last year.

Zoom (ZM) Q1 CY2024 Highlights:

- Revenue: $1.14 billion vs analyst estimates of $1.13 billion (1.2% beat)

- EPS (non-GAAP): $1.35 vs analyst estimates of $1.19 (13.5% beat)

- Revenue Guidance for Q2 CY2024 is $1.15 billion at the midpoint, roughly in line with what analysts were expecting

- The company reconfirmed its revenue guidance for the full year of $4.62 billion at the midpoint

- Gross Margin (GAAP): 76.1%, in line with the same quarter last year

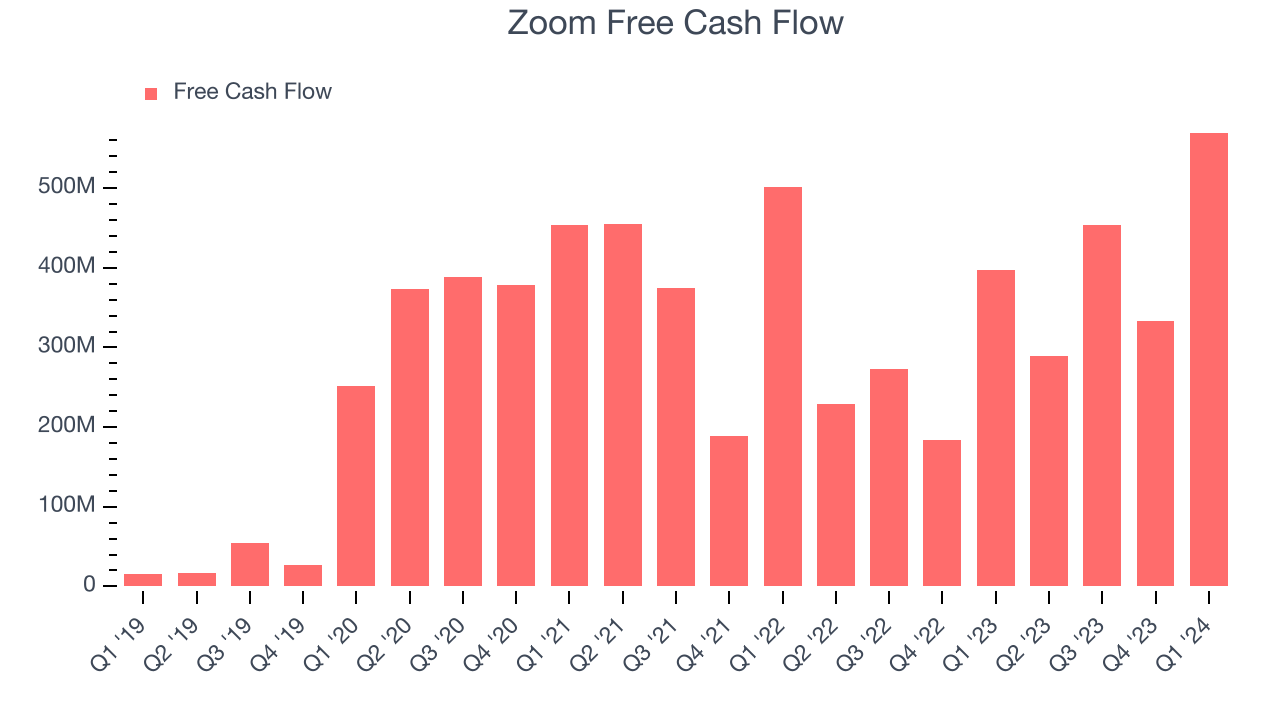

- Free Cash Flow of $569.7 million, up 71.2% from the previous quarter

- Net Revenue Retention Rate: 99%, in line with the previous quarter

- Customers: 3,883 customers paying more than $100,000 annually

- Market Capitalization: $19.92 billion

Started by Eric Yuan who once ran engineering for Cisco’s video conferencing business, Zoom (NASDAQ:ZM) offers an easy to use, cloud-based platform for video conferencing, audio conferencing and screen sharing.

The company became a household name during the Covid pandemic and today it's used not only for business meetings but also by teachers to conduct classes, by developers to write code together, and by lawyers in court.

Zoom didn’t invent video conferencing, it just made it a lot less painful. The platform works reasonably well even on a spotty internet connection, is easy to use, cheap and works across mobile and desktop. The company is notoriously customer obsessed and Yuan, the CEO, has been known to personally write to disgruntled users for feedback.

Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

And that is important because there is a lot of competition in the video conferencing space from products like Google Meet, Microsoft (NASDAQ:MSFT) Teams, Cisco (NASDAQ:CSCO) Webex or upcoming startups like Around.co.

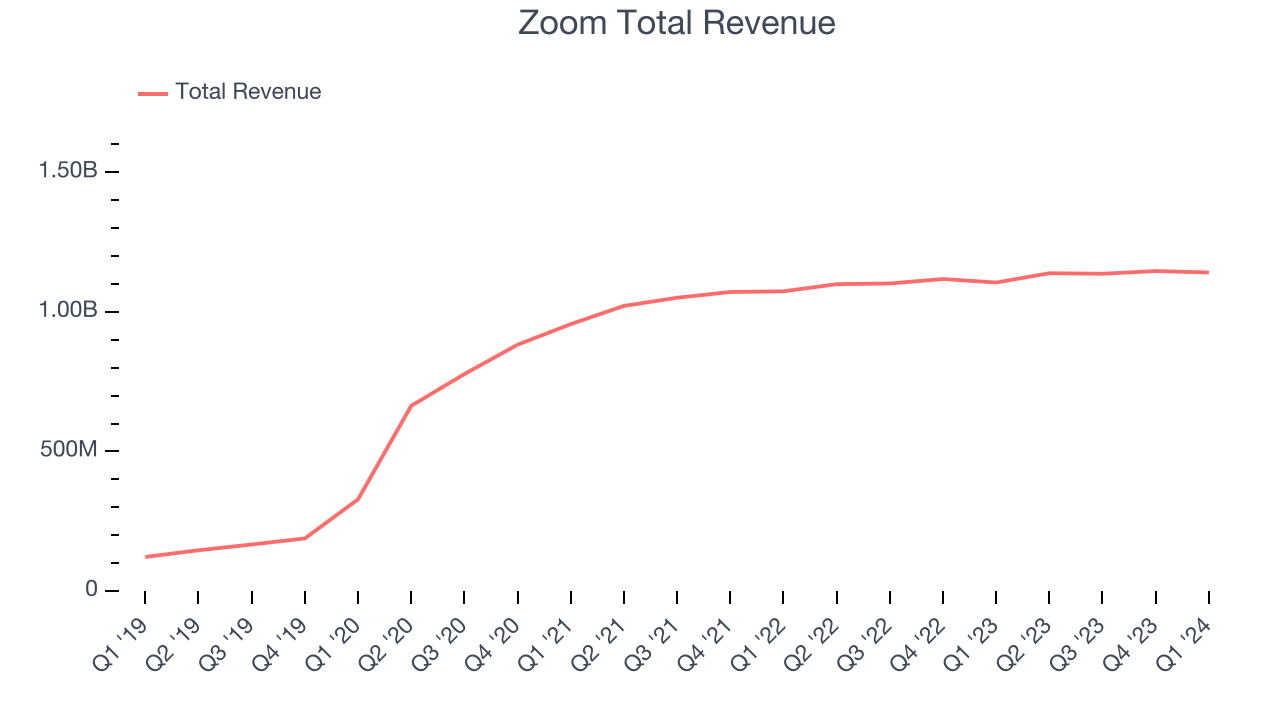

Sales Growth

As you can see below, Zoom's revenue growth has been unremarkable over the last three years, growing from $956.2 million in Q1 2022 to $1.14 billion this quarter.

Zoom's quarterly revenue was only up 3.2% year on year, which might disappoint some shareholders. On top of that, the company's revenue actually decreased by $5.22 million in Q1 compared to the $9.73 million increase in Q4 CY2023. Sales also dropped by a similar amount a year ago and management is guiding for revenue to rebound in the coming quarter, which might hint at an emerging seasonal pattern.

Next quarter's guidance suggests that Zoom is expecting revenue to grow 0.8% year on year to $1.15 billion, slowing down from the 3.6% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 1.9% over the next 12 months before the earnings results announcement.

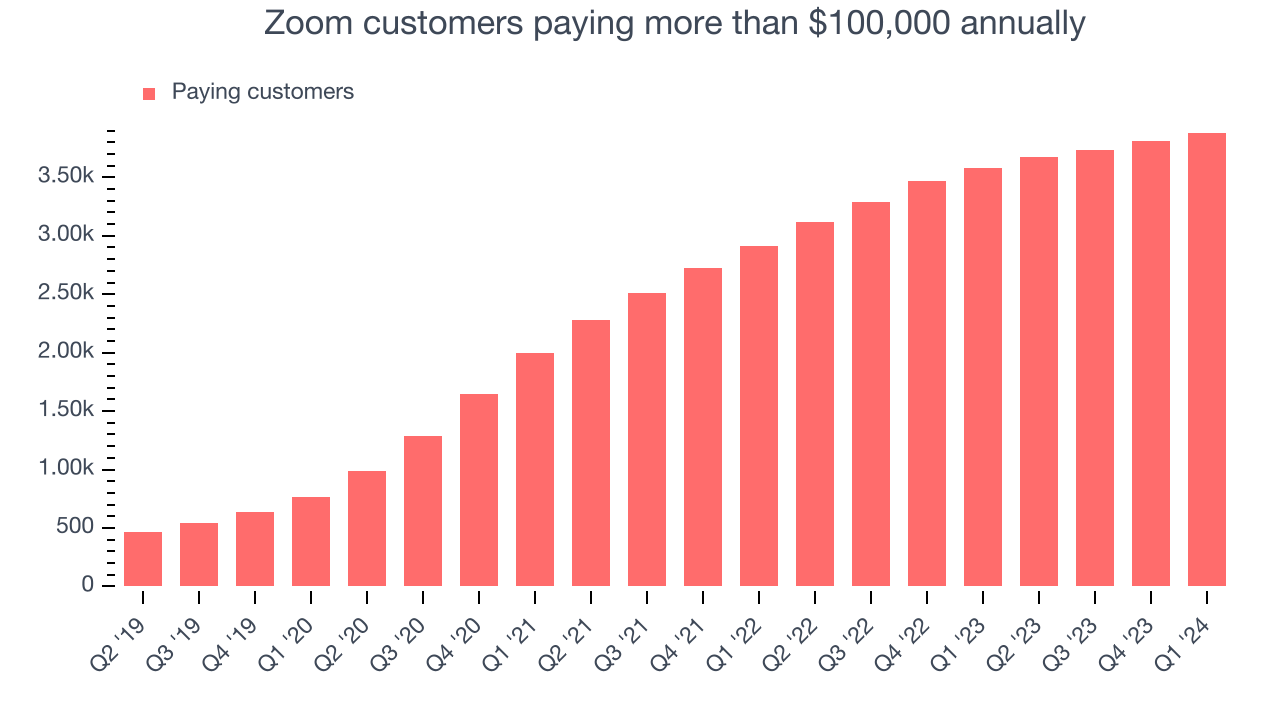

Large Customers Growth

This quarter, Zoom reported 3,883 enterprise customers paying more than $100,000 annually, an increase of 73 from the previous quarter. That's in line with the number of contracts wins in the last quarter but quite a bit below what we've typically observed over the last year, suggesting that the sales slowdown we observed in the last quarter could continue.

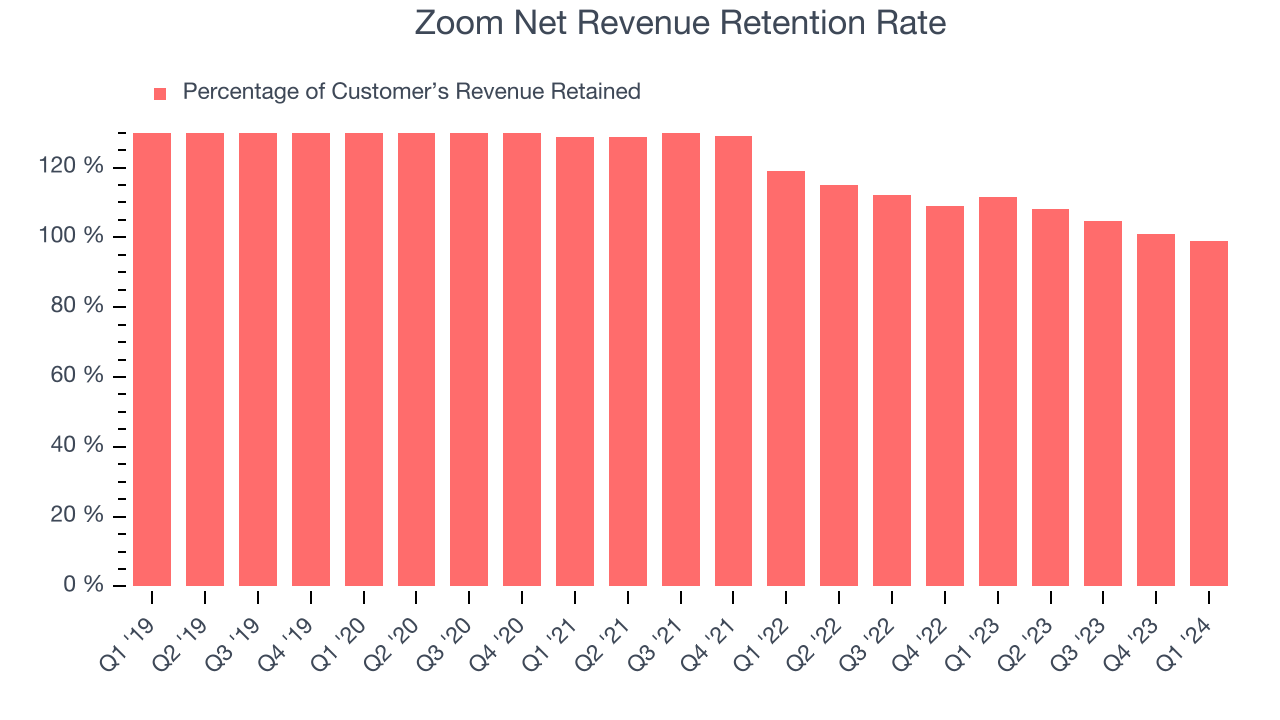

Product Success

One of the best parts about the software-as-a-service business model (and a reason why SaaS companies trade at such high valuation multiples) is that customers typically spend more on a company's products and services over time.

Zoom's net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 99% in Q1. This means Zoom's revenue would've decreased by 1% over the last 12 months if it didn't win any new customers.

Zoom's already weak net retention rate has been dropping the last year, signaling that some customers aren't satisfied with its products, leading to lost contracts and revenue streams.

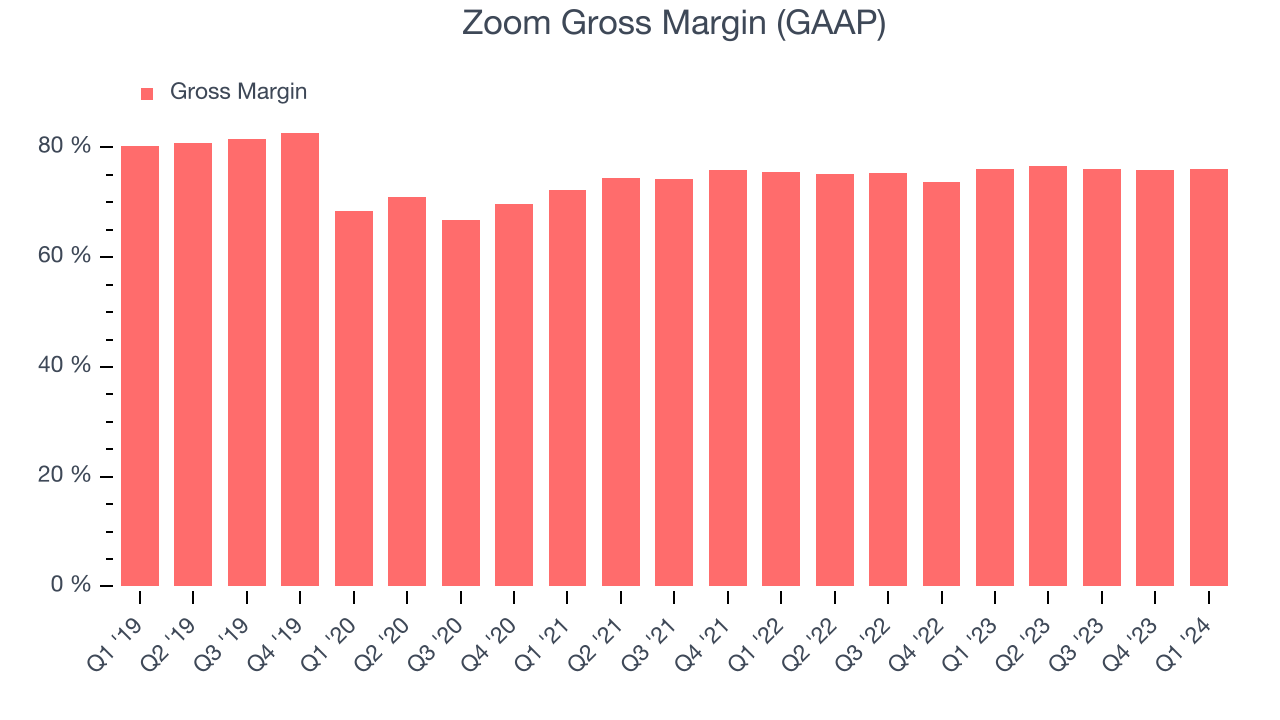

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Zoom's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 76.1% in Q1.

That means that for every $1 in revenue the company had $0.76 left to spend on developing new products, sales and marketing, and general administrative overhead. Zoom's impressive gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity. It's also comforting to see its gross margin remain stable, indicating that Zoom is controlling its costs and not under pressure from its competitors to lower prices.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Zoom's free cash flow came in at $569.7 million in Q1, up 43.6% year on year.

Zoom has generated $1.64 billion in free cash flow over the last 12 months, an eye-popping 36% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Key Takeaways from Zoom's Q1 Results

It was encouraging to see Zoom narrowly top analysts' revenue expectations this quarter. On the other hand, its revenue guidance for next quarter underwhelmed and its net revenue retention decreased. Overall, the results could have been better. The company is down 1.5% on the results and currently trades at $63.19 per share.

Is Now The Time?

When considering an investment in Zoom, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in case of Zoom, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last three years, and analysts expect growth to deteriorate from here. And while its bountiful generation of free cash flow empowers it to invest in growth initiatives, unfortunately, its customer acquisition is less efficient than many comparable companies.

Zoom's price-to-sales ratio based on the next 12 months is 4.3x, suggesting the market has lower expectations for the business relative to the hottest tech stocks. While there are some things to like about Zoom and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $78.63 right before these results (compared to the current share price of $63.19).

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.